Relative total shareholder return (“relative TSR”) has re-emerged as a preeminent management performance measure. The post-Enron decade saw a reduction in stock options in compensation programs, replaced by various types of share unit plans(RSUs, PSUs). Relative TSR was used as a performance modifier in many of these share unit plans. During the Great Recession, much energy was devoted to ensuring executive pay was aligned to an organization’s appetite for risk (focusing on areas such as recoupment policies). More recently, relative TSR has re-emerged in an even more significant way – for both back-testing pay-for-performance (P4P) alignment and as a popular long-term incentive plan (LTIP) measure.

Relative TSR is arguably the most all-encompassing and objective performance measure. Assuming markets are efficient, the share price represents both the current and future expected cash flow and profitability of an underlying organization.

It is important that Boards understand the strengths, weaknesses and operational issues related to relative TSR for their specific companies, and not simply be captivated by its popularity or favourable treatment by the proxy advisors. If TSR is determined to be a good measure of performance, it should be used directly in long-term incentives plans. In situations where incorporating relative TSR does not improve shareholder alignment, this fact should be disclosed and explained. In either case, relative TSR should be monitored by the Board to provide context for decision-making purposes.

What’s Behind the Re-emergence of Relative TSR

- Institutional investors and the proxy advisors have a stronger voice through “say-on-pay”, and are looking for a significant percentage of equity incentives to be performance- conditioned, preferably against a relative benchmark

- Pending Dodd-Frank disclosure rules will require a proxy disclosed assessment of historical pay-for-performance

- The Great Recession and the “1%” debate have put added pressure on Boards to ensure pay is properly justified and aligned with the investor experience

Critical Questions

- How does relative TSR stack up against other measures of shareholder value?

- What importance should relative TSR have in the equity compensation structure, if any?

- What is the best approach in terms of peer groups and measurement methodology?

- Are there any other factors affecting relative TSR that should be considered?

Incorporating relative TSR into a performance framework offers several benefits, but is not without limitations.

Benefits

- Counterbalances the general market movement “wind-fall” problems associated with stock options

- Satisfies motivation and retention objectives in both up and down markets

- May result in a closer measure of management performance (measuring “alpha”), at least theoretically

- Permits multi-year measurement of performance

- Does not require long-term goal-setting

Limitations

- Over finite time periods, strong TSR may not be driven by superior financial performance

- Exogenous factors and increasing investor expectations make it difficult to consistently outperform the benchmark

- Does not drive specific behaviours related to operational or strategic objectives

- Timing can have a significant impact on vesting

- Challenges in finding peer group constituants

Tends to Work In

- Mature businesses

- Businesses significantly impacted by external factors

- Businesses with sufficient number of relevant peers

Tends Not to Work In

- High growth businesses (e.g., start-ups, upstream oil & gas)

- Turnaround situations

- Businesses not in a directly competitive market (e.g., biotechnology)

Pricing Conditions

Relative TSR can be far from unbiased and, in turn, can fall short of capturing management’s true performance. Embedded in share prices are varying levels of expected management performance. To this end, it can be argued that the market is objective, but not always fair. Some comfort can be taken in the fact that if measured and rewarded over a number of cycles, varying expectations become less impactful. Management with high expectations embedded in their share prices should have been appropriately rewarded through historical equity grants, making these high expectations more reasonable.

A useful starting point is to gain an understanding of performance expectations and determine whether they are reasonable, easy or difficult. These could include:

- Analysts’ earnings estimates, relative to budgets, guidance and peer expectations

- Event speculations (e.g., M&A premiums built into share price)

- Market value versus internal valuation (e.g., based on enterprise value multiples)

- Historical relative performance and whether such relationships are sustainable

In the vast majority of situations, we would argue that expectations underlying share prices are reasonable, particularly in the case of mature companies where relative TSR can be most readily applied.

"The market may think that management is doing an outstanding job, but this belief has already been factored into the share price – this effect explains why extraordinary managers may deliver ordinary short-term TSR, and managers of companies with lower performance expectations find it easier to achieve high TSR”

Dobbs and Koller, “Measuring Long- Term Performance”, McKinsey Quarterly

SO RELATIVE TSR IS A GO... NOW WHAT?

PEER GROUP DEVELOPMENT

Boards are well aware of the challenges in finding appropriate peer groups. The objective here is to choose a comparator group that is large enough to be robust, but without sacrificing the relevance of comparators.

In Canada, we have many industries with only a few big players, and perhaps a number of smaller or emerging companies. Many of our clients are forced to expand their peer groups to include greater variation in size, broader industry definitions and / or wider geographies. This, in and of itself, does not mean relative TSR should be abandoned. It is simply one of the factors that should be assessed when determining whether relative TSR more accurately measures management performance compared to the alternatives, be it other performance metrics or types of equity instruments.

CUSTOM PEER GROUP

Utilizing a custom peer group is the most compelling approach when designing a relative TSR metric; most tailored proxy for competitive market

BENCHMARK INDEX

If a sufficient number of peers cannot be found, then a broader industry or market index can provide a relevant market reference point

Back-Testing / Stress-Testing

Once a potential comparator group is created, it is important to test the group against a range of historical and future share price / payout scenarios to confirm that:

- Outcomes align with historical notion of performance

- Any miscorrelations with individual or groups of companies can be identified and accounted for

Testing is intended to provide a level of comfort that the group's constituents are suitable, and outcomes workable

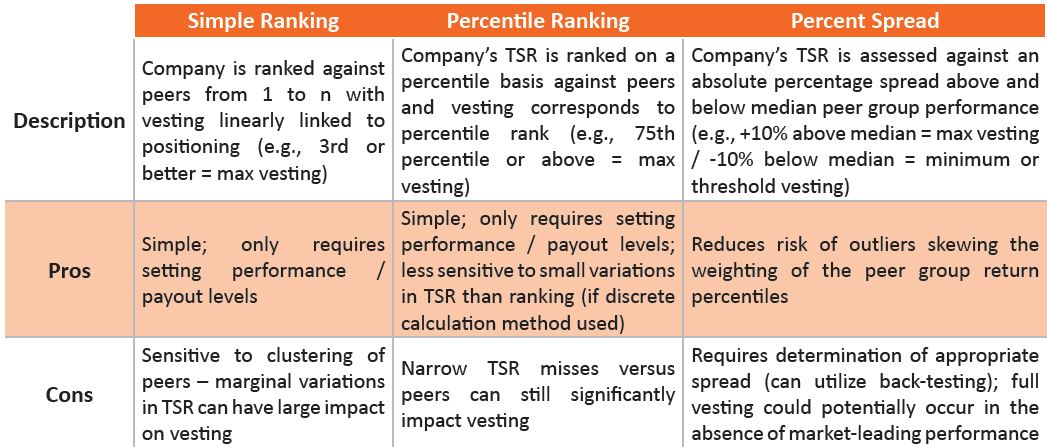

MEASUREMENT METHOD

Once a peer group has been chosen, the Board must then decide how performance against that peer group will be measured. There are three primary methodologies that companies will use.

VARYING SENSITIVITIES – CURRENCY, COMMODITY PRICES, ETC.

Even within a seemingly homogenous peer group, companies may have varying share price sensitivities to business conditions and other exogenous factors. Companies that remain profitable throughout a business or industry cycle are more likely to outperform during downturns and underperform during recoveries. Companies representing higher risk investments have a higher expected investment return and, at least theoretically, should be able to outperform on a TSR basis. Commodity price changes can also influence company performance in different ways. Changes in oil prices can impact two E&P companies to varying degrees depending on their hedging programs.

The currency and stock exchange (e.g., TSX or NYSE) can influence TSR during times of material movements in exchange rates. The influence of currency is an area that tends to be overly simplified by the view that using a common currency or exchange will eliminate most major currency influences. A useful starting point is to consider the natural currency of the organization and compare it to the exchange listed currency. By natural currency, we mean a weighting of the countries (currencies) in which revenues, expenses, assets and financings occur. This will often be a blend of currencies, further influenced by hedging. Currency risk, in this context, is the degree to which the natural currency differs from the stock exchange currency being measured.

The table at right provides a useful example of the issue at hand. It illustrates the impact on price and TSR for 10% swings in exchange rates. Where TSR is measured (i.e., on what exchange) for multi-country peer groups can significantly influence relative TSR performance.

The table at right provides a useful example of the issue at hand. It illustrates the impact on price and TSR for 10% swings in exchange rates. Where TSR is measured (i.e., on what exchange) for multi-country peer groups can significantly influence relative TSR performance.

When these sensitivities are at play, it is important for the Board to fully understand the impact they will have on performance, and determine how to either minimize, or consistently apply, that impact.

OTHER CONSIDERATIONS

- Payout Curve: The Board will need to determine at what level of relative performance will a minimum / target / maximum payout occur. Will a full payout be achieved upon top quartile performance, or will it require better relative results?

- Treatment of Peer Group Changes: Changes among peer group constituents (e.g., corporate transactions, delistings, etc.) can create material issues when calculating TSR; the Board should define treatment rules at the outset (e.g., determine replacements, treatment of partial periods, etc.)

CONCLUDING THOUGHTS

While relative TSR is clearly an important measure for shareholders, it is important to assess how well it fits as a performance measure for your company. With an understanding of the measure’s strengths and weaknesses, Boards and management are in a better position to incorporate relative TSR in a thoughtful and effective manner.