Note to reader: Recent comments from JP Morgan CEO, Jamie Dimon , criticising shareholders for the perception they vote in lock-step with proxy advisors is timely as it touches upon some of the key points in this briefing.

There has been a major evolution in how institutional shareholders approach executive compensation and board governance matters over the last few years. The growing acceptance of investor stewardship principles have encouraged these investors to take a more proactive approach on these matters.

institutional shareholders approach executive compensation and board governance matters over the last few years. The growing acceptance of investor stewardship principles have encouraged these investors to take a more proactive approach on these matters.

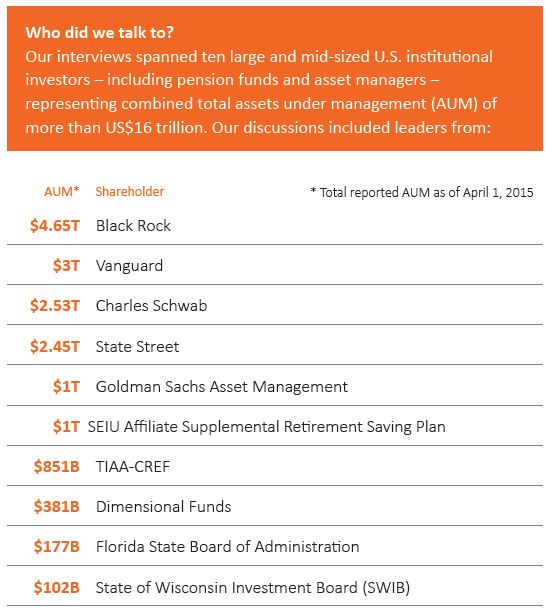

To give our clients a behind-the-scenes look at what this might mean for them, we met with ten large and influential institutional U.S. shareholders to find out what their priorities and focuses will be going forward. Our interviews were with the leaders within the governance function who are responsible for the voting of the proxies, and most often engaging with directors and management on key issues related to governance, performance and executive compensation.

Executive compensation remains an important area of focus for these investors with a particular emphasis on pay‑for‑performance alignment. While interest in compensation is expected to remain high, institutional shareholders believe that say-on-pay and majority voting appropriately empower them to challenge boards and issuers where there is a perceived issue.

It is worth noting that as these major investors have become more sophisticated and organized, their reliance on proxy advisors has waned – they increasingly use their own guidelines and judgement in making voting decisions. The differences between the institutional shareholder and the proxy advisor guidelines, as well as between the shareholders themselves vary widely.

Another area rising to the top of the investor agenda is board accountability, independence and structure. Until recently, institutional investors have largely been reactive in this area - in contrast to executive pay where they have been quite influential and active in shaping certain market practices (e.g., increased use of performance share/units, increasing prevalence of double-trigger change of control provisions).

While these investors have no interest in “micro‑managing” a company, they also recognize governance of the board is within the purview of shareholders. Specific areas of focus will include proxy access, diversity, director independence, the separation between Chairman and CEO roles, and board declassification.

FINE‑TUNING EXECUTIVE COMPENSATION

Executive compensation was a critical area of focus for the 2015 proxy season. There is a general consensus among institutional shareholders that the majority of issuers are doing the right thing with respect to executive pay, evidenced by the strong say-on-pay support that most organizations receive from their shareholders.

Where there are concerns, they have typically centered on pay-for-performance alignment – a relatively small minority of companies have bottom quartile performance and top quartile pay resulting in weak say-on-pay and director election results. It is worth noting that there is still no clear view among the large institutional shareholders on what constitutes performance and the best way to measure it. Many of the institutional shareholders will generally start their assessment of pay-for-performance by reviewing the proxy advisor reports as an initial filter, and then apply their own judgement - some will also have well-defined internal guidelines to assess performance and pay.

Shareholders Listen to a Well‑Reasoned Case

In early 2015, there was a notable example that within the resource space demonstrates investors do apply their judgement in making voting decisions, particularly, where there is a well-reasoned case brought forward by the company.

- In 2014, the Company received 75% support on their SOP vote with ISS supporting and Glass Lewis recommending against

- In 2015, ISS again supported while GL recommended a vote against the company due to a perceived pay-for-performance misalignment (relative TSR was solid but ROA and ROE dragged them down)

- One of the key issues was the GL methodology and use of return (ROA, ROE) metrics which can benefit companies that take major write-offs by making their return metrics look better than those who do not take write-offs – a fact that was not compelling to GL

- The Company undertook an outreach campaign directly to their major shareholders to help them understand the board’s view on payfor-performance alignment, business strategy and key performance drivers

- Investors agreed with the Company’s perspective, as the Company received 90% on their SOP vote

There is also acknowledgement that a small minority of ‘problematic’ issuers (perceived to have a major misalignment of pay and performance – typically very high pay for low performance) consistently attract a disproportionate amount of attention on executive pay matters.

As previously noted, institutional investors believe they are well positioned with say-on-pay and majority voting to take action where they believe boards could do a better job. Voting against say-on-pay is the most prevalent course of action. Only if they believe their concerns are not being addressed or if there is an egregious concern, they may withhold on director elections. As such, with the exception of some fine-tuning of guidelines, we do not expect any major policy initiatives on executive pay from the institutional investors.

THREE TOPICS OF INTEREST WITH RESPECT TO EXECUTIVE COMPENSATION ARE:

Institutional investors want to see stronger alignment between corporate strategy and compensation strategy.

Some institutional investors are starting to compare the corporate strategy that issuers communicate to portfolio managers against the strategy they disclose in the proxy for compensation purposes and are finding that – in some cases – the linkage is tenuous at best. For example, investor presentations often express a commitment to areas such as customer satisfaction but a review of the proxy would find no mention that this was a strategic focus.

Eliminating full vesting of performance-based equity on change of control.

Moving beyond double‑trigger v. single trigger, our interviews suggest that institutional investors are increasingly more inclined to support shareholder proposals that prohibit the full acceleration of unvested performance-based equity in the event of a change of control (even if it is double-triggered). The rationale being that these awards have not completed their performance cycle and thus are not “earned.” At this time, the focus has not extended to time-vested equity incentives.

Shareholders are more inclined to seek to engage on executive compensation during proxy season where they may have potential concerns.

Given limited resources, they have historically tended to push engagement outside of busy proxy season. More recently, investors have recognized that discussions on pay matters may be more ‘constructive’ with a proxy in hand, especially where clarification is required to determine a vote.

BOARD ACCOUNTABILITY, STRUCTURE AND COMPOSITION UNDER THE MICROSCOPE

Three specific issues related to board accountability, structure and composition that were raised in our discussions:

Proxy access: With various stakeholders putting forward a variety of proposals on proxy access, it is clear that this area is rapidly evolving. However, most institutional investors in our panel and beyond are coalescing around the ‘3-for-3’ standard. Some major issuers – such as GE, Bank of America and Prudential – have voluntarily adopted this standard.

What is the ‘3-for-3’ standard? The 3-for-3 standard allows shareholders who hold at least 3 percent of the shares of a company for three years to nominate directors for election.

The Chairman‑CEO role: While the separation between Chairman and CEO roles is not a new topic, it continues to remain top of mind due to some high-profile situations in recent years. Institutional investors generally support the splitting of the role in most circumstances, but acknowledge a combined role may need to be considered on a case by case basis.

Board composition: Institutional investors are increasingly interested in understanding issuer’s views and approaches to director and management diversity and director renewal policies and tenure. There is wide acknowledgement that diversity extends beyond gender, and may include factors such as race, age, breadth of experience etc. At this point, there is limited support for any ‘bright line’ tests, but our discussions show interest in organizations looking at the issue with renewed perspective In response, we have observed a limited number of companies explicitly incorporate diversity indicators into their executive compensation performance metrics.

KEEPING YOUR FINGER ON THE PULSE

Clearly, the focus and influence of institutional investors continue to evolve. Based on our discussions, we expect to see increased scrutiny on board accountability, structure and composition and continued interest in executive compensation actions and policies through 2015 and into 2016.

At the end of the day, the key for issuers – both in the U.S. and those in foreign markets – hoping to attract and retain U.S. institutional investors will be in keeping their finger on the pulse of the major shareholders through the development of a consistent and proactive shareholder communication strategy.

We believe that those boards and issuers that understand shareholder concerns and build stronger relationships with their stakeholders will ultimately enjoy a more predictable proxy season in the future.

CONCLUDING THOUGHTS

As we take stock of the end of the 2015 proxy season and as we look into 2016, we advise clients to:

- Review 2015 director election and say-on-pay voting results and surface any comments or concerns on executive compensation, performance or related governance matters even where the shareholder may have voted in favor.

- Identify major institutional shareholders among the shareholder base. Do some background research and ensure the board and compensation committee understands their policies and priorities and how your compensation programs align.

- Offer to engage with the largest shareholders even if there are no specific issues or concerns identified (open the door). Develop and maintain relationships with these shareholders and open communication channels (easier to build a constructive relationship when there are no major issues).

- Boards should ensure they have a fact-based well-reasoned narrative of how they view and align pay and performance. This becomes even more critical now that pay versus performance disclosure has been proposed by the SEC.