The 2015 proxy season has seen noteworthy developments among Canada’s largest issuers. Overall, CEO pay levels are flat year-over-year, while design modifications for short and long term incentives continue to evolve to better align pay outcomes with performance. Finally, shareholders and proxy advisors continue to exert strong influence on executive pay decisions, with three TSX60 issuers failing their Say-on-Pay votes.

With most of the TSX60 having completed their annual general meetings, Hugessen has summarized its high-level observations of key executive compensation and related governance trends from the 2015 proxy season. This briefing highlights broad findings in the following areas:

- CEO pay levels among the TSX60 constituents

- Noteworthy disclosure of compensation policies and practices

- Governance update, specifically emerging topics in the proxy advisor and institutional shareholder community, as well as results from 2015 Say on Pay votes

- Regulatory update, specifically observations on the new diversity disclosure requirement

TSX60 CEO Pay Levels

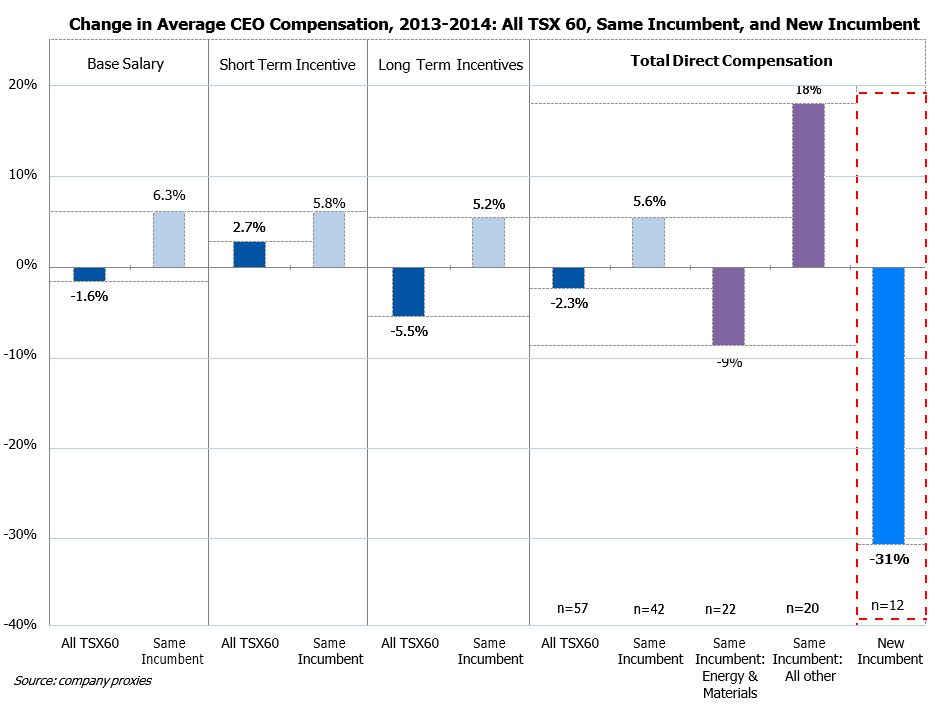

For the current constituents of the TSX 601, median actual Total Direct Compensation (“TDC”) in 2014 was $7.4 million, a decrease of 1.7% from the 2013 median2. Average TDC in 2014 (also $7.4 million) decreased by 2.3% from the 2013 average. Our observations reflect year-over-year changes in the TSX60 constituents including the 12 CEO transitions during 2014.

- 3 new TSX60 issuers: Alimentation Couche-Tard, Inter Pipeline, and Restaurant Brands International replaced Enerplus, Penn West, and Tim Hortons

- 12 CEO Transitions: CEO actual TDC for the 12 new incumbents decreased by an average of 31% compared to their predecessors’ pay. Included in the 12 CEO transitions, were 4 of the 5 big banks. CEO target TDC for the 4 banks decreased by an average of 20% for the new incumbents. Actual TDC was also materially reduced by 32.5%

Among the TSX60, 42 issuers had the same incumbent in the CEO role in 2013 and 2014. Average TDC for the same incumbent CEOs increased by 5.6% year-over-year.

- The 22 energy and materials (predominately mining) companies within this group saw a decrease in average CEO TDC of 9%, compared to an 18% increase in average TDC among all other sectors

Trends in Compensation Policies and Practices

From our review of 2015 information circulars, we note the following ongoing and emerging trends:

STIP performance realignment: Several issuers (n=7) are refining STIP design to ensure stronger alignment with business strategy and key drivers of performance. For example, effective 2015, Agrium reduced the number of key performance indicators within their balanced scorecard to better focus on a smaller number of business critical measures and to provide stronger alignment with Agrium’s strategic priorities. In addition, we are seeing the pendulum swing back somewhat to heavier weighting on corporate performance relative to individual performance when determining STIP payouts. Effective 2015, TransAlta revised their STIP to increase the executives’ corporate performance weighting.

New or modified PSU plan designs – performance measures beyond relative total shareholder return (“TSR”): 47 TSX60 issuers have PSU plans and the majority now include more than one performance metric (n=33). 30 TSX60 issuers include relative TSR as a performance metric, of which 13 are based 100% on relative TSR. From our conversations with institutional shareholders we know they are seeking plans where the chosen metrics and corporate strategy are clearly aligned. This trend also reflects the balancing act between a reliance on relative measures only, and the desire to ensure payouts are in the context of delivering minimum absolute levels of corporate results. In 2014, Inter Pipeline introduced a PSU plan that evenly weights relative TSR and funds from operations per share, while Cameco’s PSU plan is based 30% each on average relative realized uranium price and increased production, and 40% on relative TSR.

“Longer-term” LTIP designs (i.e., extended vesting and/or term beyond three years): The vast majority of RSU and PSU plans (generally defined as “long-term” incentives) vest and are paid out within three years, which many view as “mid-term” instead of “long-term”. We are starting to see the focus shifting to longer-term awards, although at a modest pace. This year, ARC Resources proposed and shareholders approved a restricted share unit plan with a 10 year term, whereby vesting occurs on the 8th, 9th, and 10th anniversary following the date of grant. Effective 2015, Manulife introduced a formal restriction on all stock options awarded so they cannot be exercised prior to the fifth anniversary of grant, with the expectation that they should be held for the full term (10 years).

Performance conditioned stock options issued in place of or in addition to regular time-vested options: In 2014, Magna executives received performance conditioned stock options in place of regular time-vested stock options, whereby vesting is contingent upon relative TSR performance against industry peers. Six issuers among the TSX60 now have performance conditioned stock options. However, among the TSX60, we continue to see a declining prevalence of stock options. On average, the percentage of stock options comprising CEO LTIP mix in 2014 was 30%, declining from an average of 34% in 2013.

Hold requirements beyond vesting are becoming more prevalent among executives and a minority practice has emerged for post-retirement hold requirements for directors: Manulife’s 5- year exercise restriction (as described above) applies post-retirement. Director post-retirement hold requirements is an emerging practice among Canadian issuers. Canadian National Railway and Canadian Pacific Railway are among the first to adopt director post-retirement hold requirements in 2014.

Governance Update

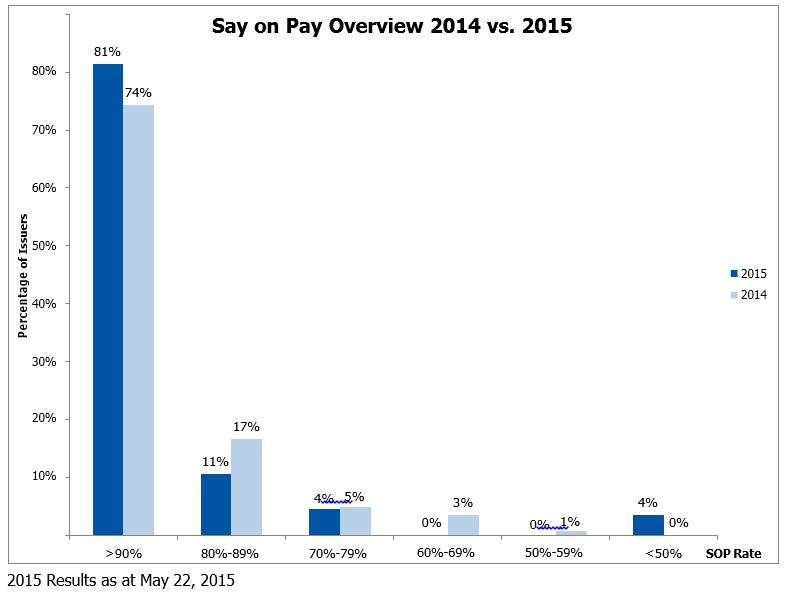

Proxy advisors (principally Institutional Shareholder Services (“ISS”), and Glass Lewis (“GL”)), continue to exert influence on the 2015 Say on Pay (“SoP”) voting results to date.

- 2015 Say on Pay Update: As at May 22, average SoP support is 92%, consistent with last year. In 2015 one new TSX60 constituent (Inter Pipeline) adopted SOP, bringing the total number of adopters among the TSX60 to 44 or 73%. The majority of non-adopters are controlled companies, three of which (Alimentation Couche Tard, CGI Group, and Power Corporation of Canada) received shareholder proposals requesting the adoption of SoP. Predictably, all of the proposals were defeated with an average support level of only 15%

Proxy Advisor Update: In 2015, GL issued four negative recommendations among the TSX60 (five less than last proxy season), while ISS issued three negative recommendations (one more than last proxy season). Among the TSX60, Barrick Gold and Yamana Gold received negative SoP recommendations from both ISS and GL, Agnico Eagle Mines and Goldcorp received a negative recommendation from Glass Lewis, and CIBC received a negative recommendation from ISS.

- GL pay for performance methodology continues to hit gold companies hard. Among the TSX60, 100% of GL negative SoP recommendations were for gold companies

- On average, the five TSX60 issuers who received negative SoP recommendations from one or both proxy advisors received 55% SoP support

Pension funds have also had a prominent voice this proxy season, in particular with three TSX60 issuers:

- Barrick Gold received a fail SoP vote of 27%: CPPIB announced their intent to withhold support from Barrick’s approach to executive compensation. BCIMC and OTPP stated their intent to withhold votes from all director nominees

- CIBC received a fail SoP vote of 41%: CPPIB and OTPP announced their intent to withhold support from CIBC’s approach to executive compensation. In addition, OTPP stated their intent to withhold support from members of CIBC’s compensation committee

- Yamana Gold received a fail SoP vote of 37%: CPPIB announced their intent to withhold support from Yamana’s approach to executive compensation

With increased scrutiny from proxy advisors and their shareholders, we are observing increased efforts by TSX60 issuers to improve disclosure and strengthen board led engagement of shareholders and proxy advisors. Pay for performance and shareholder engagement activities are being more thoughtfully disclosed, demonstrating issuers’ efforts to increase transparency regarding executive pay decisions and related governance. A notable outcome of this proxy season is Goldcorp, who in 2014 received a negative SoP recommendation from GL and a 75% SoP. In 2015, Goldcorp greatly enhanced disclosure of its approach to pay for performance and actively engaged with shareholders, but GL again recommended against on SoP. Through direct shareholder engagement by both the board and management, Goldcorp was able to receive 89% SoP, notwithstanding GL’s recommendation. Overall, this demonstrates that shareholders can be supportive of different approaches to executive compensation when well disclosed and explained.

Regulatory Update

New diversity disclosure requirement – broad spectrum of approaches among TSX60: 2015 was the first year that diversity disclosure requirements were introduced with respect to the representation of women on boards and in executive positions. Overall, there was a broad spectrum of disclosure among the TSX60, with the vast majority adopting a formal diversity policy without set targets. Several issuers have in place or adopted policies which include set targets. BCE Inc. adopted a policy stating that 25% of the Board will be comprised of females by 2017.

Implications for Issuers outside the TSX60 – Similar Trends

The TSX60 tends to lead the way on current and emerging executive compensation and governance related trends, and not surprisingly, we continue to observe companies within the broader TSX Composite following in their footsteps. Most notably, an increasing number issuers beyond the TSX60 are adopting PSU plans to partially or fully replace the usage of stock options. Consistent with the TSX60, some PSU payouts are based 100% on relative TSR, while others are based on multiple metrics of absolute and relative performance. Also, there is a continuing move to enhance pay for performance disclosure, including various approaches to realized and realizable pay illustrations (e.g., Manitoba Telecom Services and Enerplus). In addition, during the 2014 proxy season, ten TSX60 issuers adopted or extended a clawback provision, which has led to many non-TSX60 issuers following suit this proxy season.

We believe pay for performance and good governance remains top of mind among boards, compensation committees and management of a broader group of publicly traded companies. Thoughtful approaches to executive compensation, related governance, and most notably disclosure and shareholder engagement, are becoming increasingly important as shareholders continue to increase their vigilance in their evaluation of the link between pay and performance.

1 For purposes of this analysis, current TSX60 constituents include 57 issuers. As at May 20, 2015, data is not available for BlackBerry, Saputo, and Talisman (which is now private and will not release a proxy circular in 2015).

2 For the purposes of this document, TDC is equal to the sum of base salary, actual short term incentives paid, and expected value (or grant date fair-value) of long term incentives granted, all as disclosed in the summary compensation tables. This differs from how compensation is considered in other published studies, some of which include pension expense. Note that pay data pertains to the companies in the S&P TSX60 Index only.