A company’s Board of Directors is ultimately responsible for overseeing the organization’s strategy; as environmental, social, and governance (“ESG”) factors are becoming an area of increasing strategic focus for many companies, the natural question is how progress on that front is incentivized (i.e., reflected in compensation programs).

Every year, Hugessen Consulting conducts a review of the proxy circulars filed by the constituents of the S&P / TSX60 Index to report on trends in executive compensation and related governance practices among Canada’s largest and most influential companies. This article summarizes our findings related to ESG metrics in these companies’ executive compensation programs in respect of fiscal 2022.

Market Pressures on ESG

To set the stage for this discussion, it is helpful to understand the market forces that have increased the focus on ESG in recent years.

North American regulators have historically taken a somewhat less active approach than those in Europe, but we have begun to see this shift in recent years: OSFI will require financial institutions to publish climate disclosures aligned with the TCFD framework beginning in 20241, and the SEC has proposed climate-related disclosure requirements pending finalization2. In Canada and the US, we continue to observe significant influence exerted from shareholders, proxy advisors, and broader stakeholders.

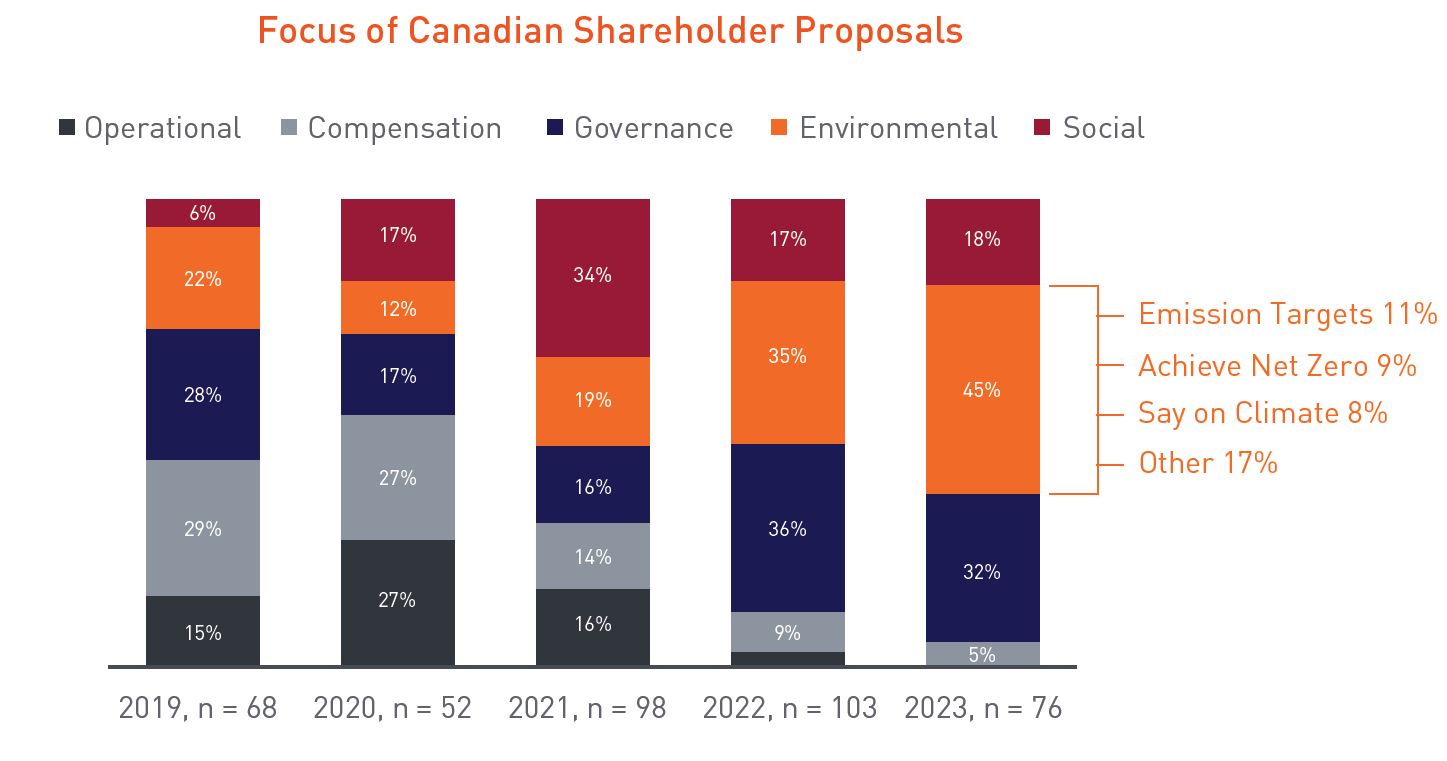

Select investors express their areas of focus through shareholder proposals; this proxy season, over 95% of proposals for TSX-listed companies were related to ESG topics. This year there was an emphasis on environmental proposals, which increased by 10% relative to 2022 and were primarily related to the disclosure of emissions targets, commitment to net zero emissions, and the adoption of an advisory vote on environmental policies (known as “Say on Climate”). All of the major Canadian banks received a proposal to adopt a Say on Climate vote, with support ranging from 16% to 21%.

One shareholder proposal passed this year, which requested that Cenovus’s Board produce a report outlining how the Company’s lobbying and public policy advocacy align with its net zero goal; this proposal was supported by the Company’s Board and management and received 99.47% support3.

Prevalence of ESG Metrics

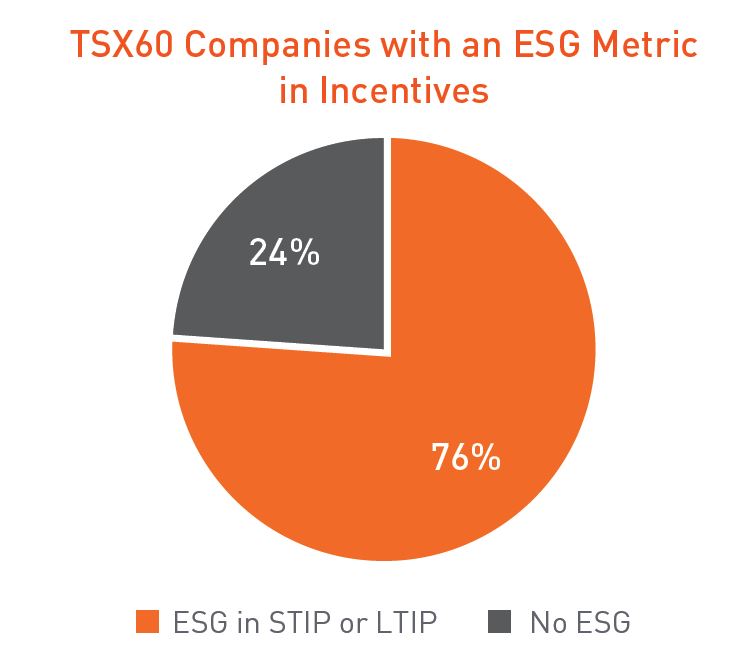

In the 2023 proxy season, we observed a “levelling off” in the number of companies in the TSX60 incorporating ESG metrics in their programs, with 76% this year versus 73% last year4. The weight of ESG metrics in incentive programs has also remained relatively consistent at about 20% on average (for the companies that have defined the weight of ESG metrics within their STIP or LTIP programs), which is similar to the past few years5.

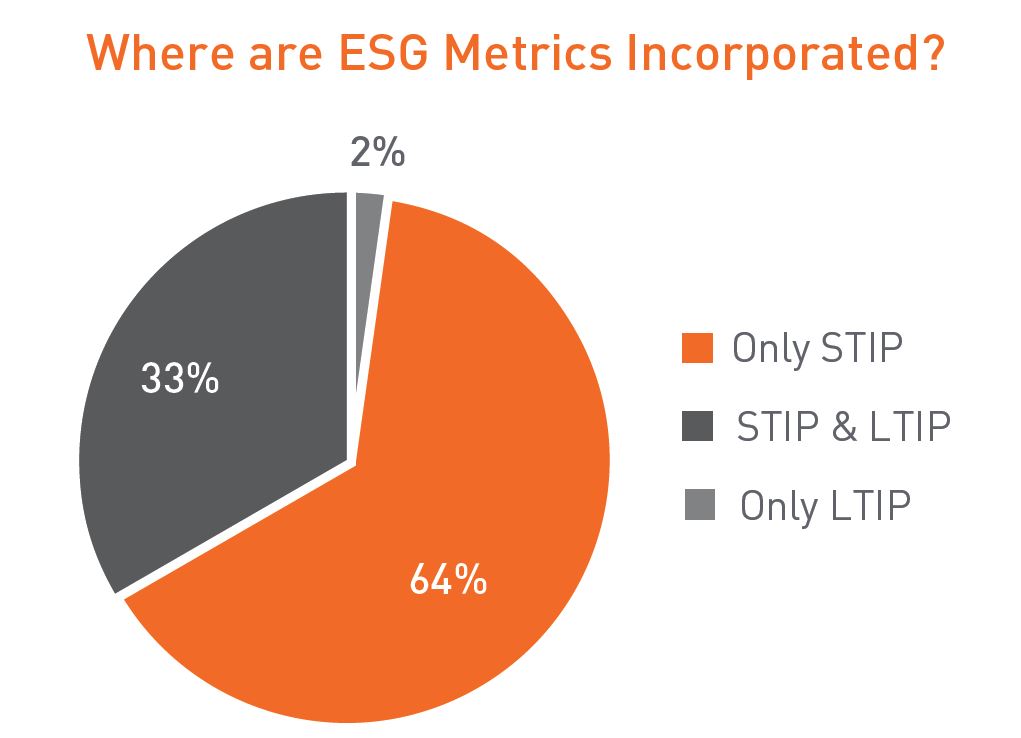

Given the long-term nature of many ESG metrics (e.g., emissions reduction by 2030), they may philosophically be better suited to an LTIP; however, we observe 44 TSX60 companies using ESG metrics in the STIP, versus only 16 companies using them in the LTIP. This represents a 5% and 23% year-over-year increase in prevalence in the STIP and LTIP, respectively (as compared to a 14% and 44% increase the year prior).

Of the 16 companies with an ESG metric in LTIP, 6 companies included an ESG metric as a “back-end” performance measure within their performance share units (“PSUs”), whereas 10 used a “front-end” conditioned LTIP (where a set of metrics informs the grant size).

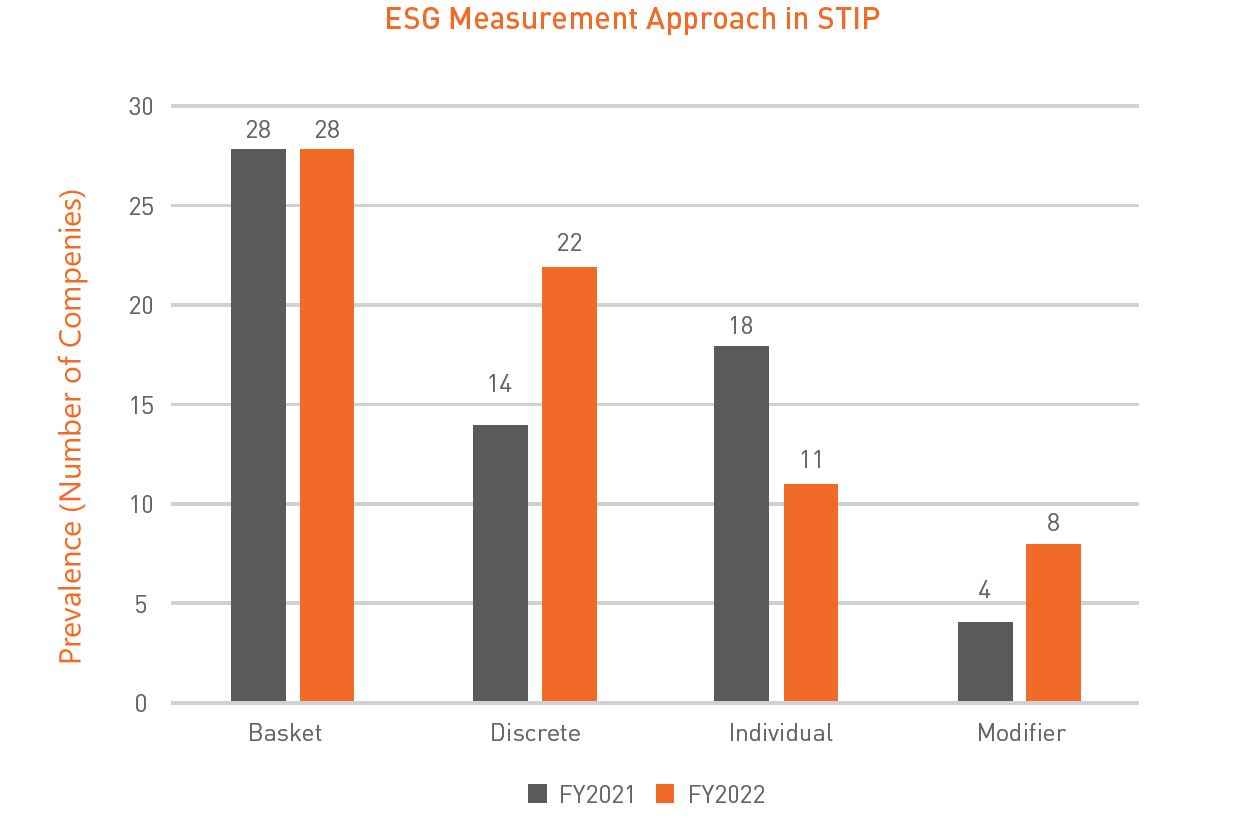

Measurement Approach

While the number of companies including ESG has not significantly changed, we observed a shift in measurement approach used by companies since last year's review.

Specifically, we saw a 57% increase in the number of companies using discrete metrics in the STIP, and a 38% decrease in the number of companies using an individual metric. We believe these trends are reflective of the increased comfort with the use of ESG metrics versus prior years. As companies become more sophisticated in their measurement, forecasting and assessment of ESG based measures, they are able to provide more robust disclosure (i.e., pre-defined metric weights) and are more confident in setting robust targets.

"Discrete" metrics have a specified weighting in a company's scorecard (this is how we most often see financial and operational measures incorporated into a corporate scorecard). A “basket” approach refers to a portion of its scorecard that includes multiple metrics with unspecified weights.

That said, there are still instances where the disclosure of targets and outcomes is clearer for basket metrics than discrete metrics. Canadian Natural Resources, for example, includes two carbon reductions metrics within a broader “Safety and Environmental” basket and does not disclose their individual weights, but clearly outlines each metric’s target setting and evaluation process.

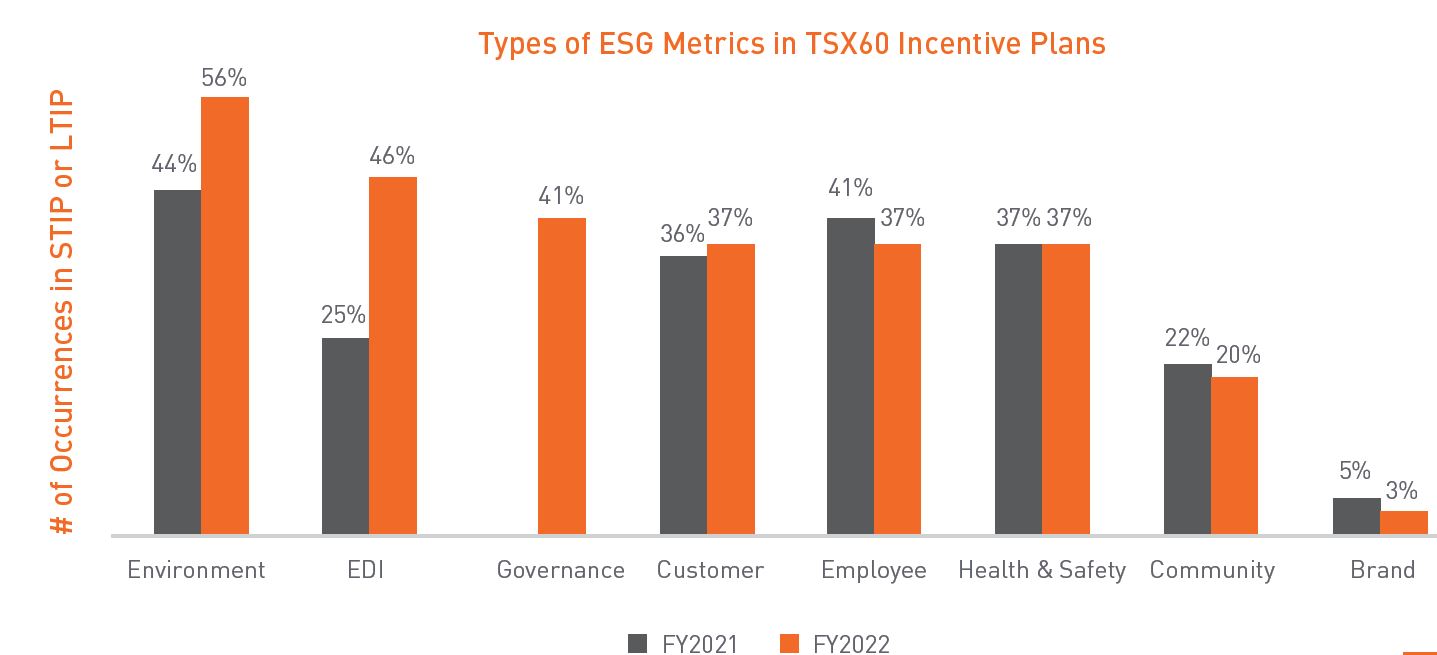

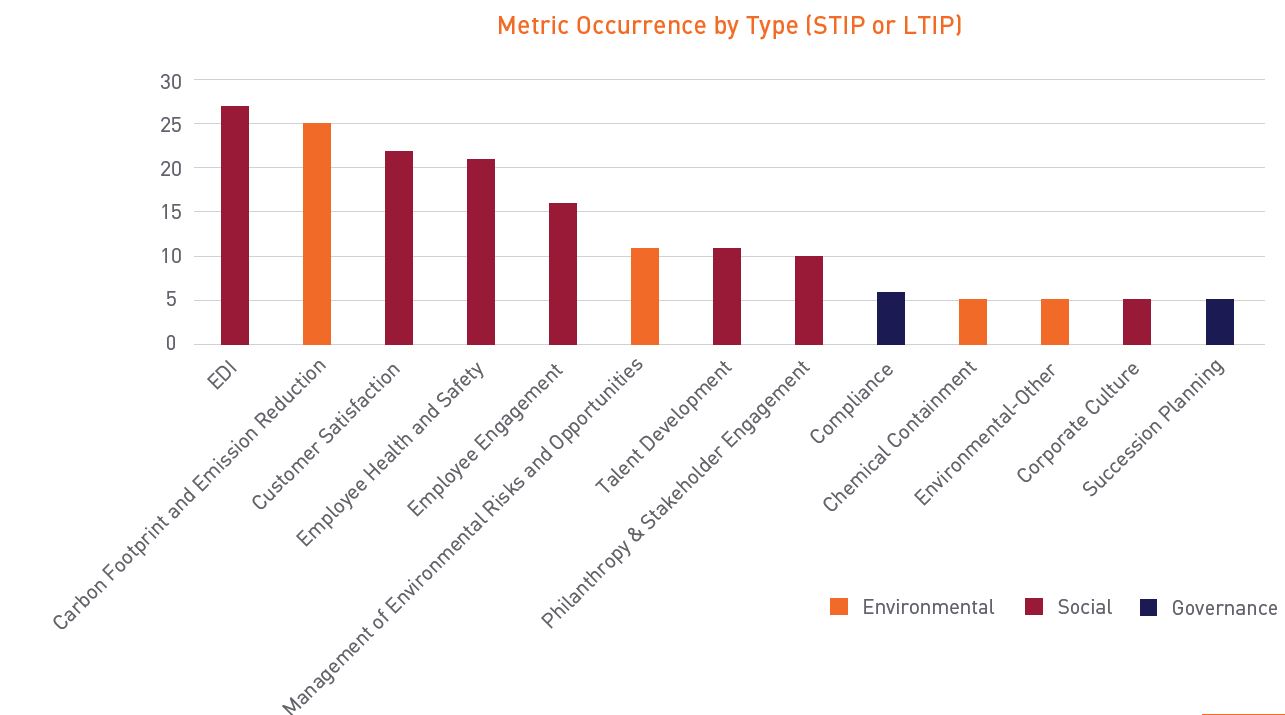

Types of Metrics

We observed significant increases in the use of environmental and equity, diversity, and inclusion (“EDI”) metrics year-over-year; the number of companies using each type of metric in their short- or long-term incentive program increased by 12% and 17%, respectively. In contrast, we observed limited year-over-year change in more “established” ESG metrics related to customers and employees. Note that we did not track the use of governance measures last year, so comparative data is not available for this category.

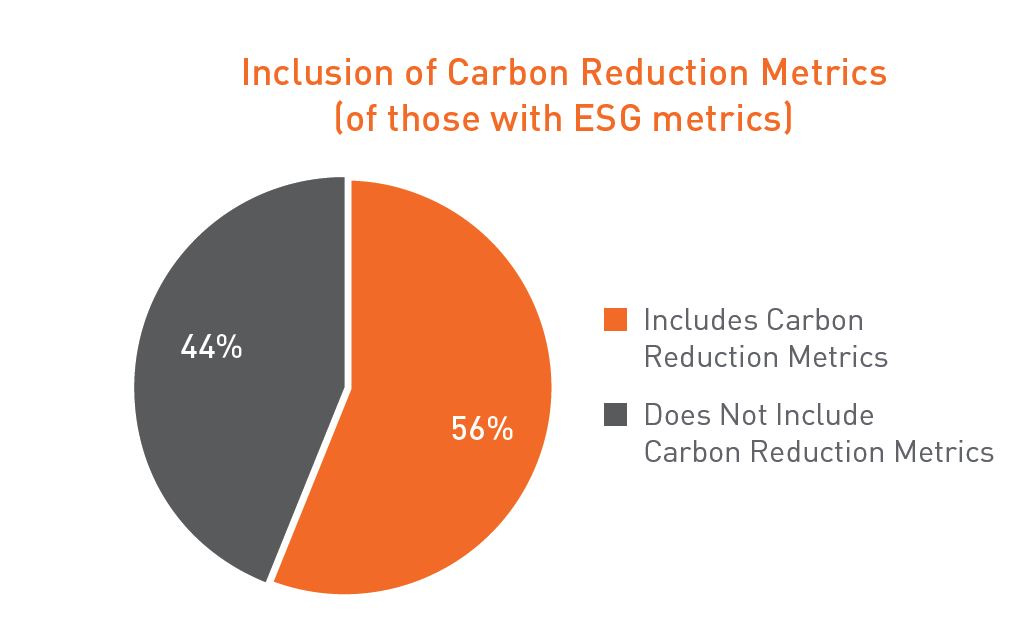

Carbon Reduction Metrics

For the first time this year, more than half of TSX60 companies with an ESG metric in compensation have a measure related to carbon reduction. We note that the adoption of public net-zero targets is often referenced in the disclosure of these metrics.

At this stage, most companies with carbon reduction metrics have not disclosed the specific targets that they are working towards. Some indicate that they are working towards an unspecified target, and others have more “process-oriented” goals such as “establishing a GHG reduction roadmap.” Those at the more

sophisticated end of the spectrum have defined specific interim targets driving to a net-zero goal.

For example, in FY2022 Fortis based 10% of its PSU performance on the reduction of scope 1 emissions. This PSU metric is a 3-year interim target tied to the Company’s longer-term goal of 75% scope 1 emissions reduction by 2035. Looking forward to FY2023, Fortis also prospectively disclosed the use of a modifier on its PSU score, which will be evaluated based on achievement of corporate-wide executive representation targets for gender and ethnicity and may adjust the aggregate PSU score by +/- 5%.

Another example is Teck Resources, which introduced a “sustainability progress index” into its PSUs for the first time in FY2022. One of the five measures within this index is a climate change metric, which is evaluated based on annual carbon reduction relative to a goal of reducing carbon intensity by 33% by 2030.

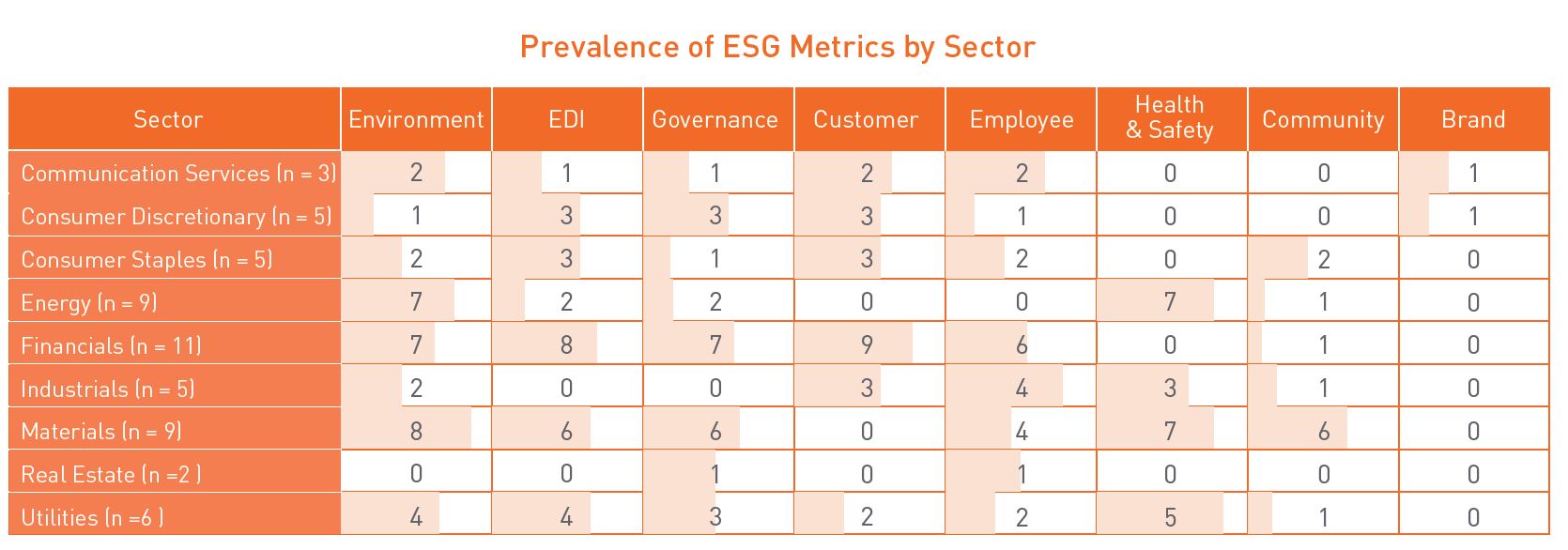

Trends by Industry

The types of ESG metrics that companies incorporate into their programs can often be generalized by industry sector. Traditionally, companies in the energy and materials sectors have tended to emphasize environmental metrics, while companies in the financial services and retail industries (among others) have tended to emphasize social metrics related to their customer base and employees.

This year, we saw more instances of both environmental and EDI metrics across other industries, with a high prevalence of environmental metrics in the financial sector, and notable year-over-year increases in the use of EDI metrics in the materials and utilities sectors (the number of companies with an EDI metric increased from 3 to 6 in the materials sector and 1 to 4 in utilities).

While the metric categories are becoming more widespread, the metrics themselves remain highly tailored. For example, an environmental measure at an extractive company may include “environmental incidents,” whereas at a financial institution a “financed emissions” metric would be more common.

Looking Forward

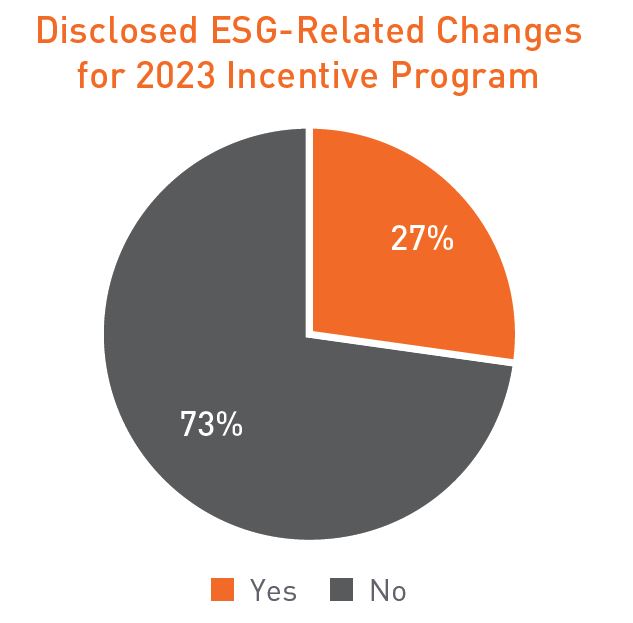

As of the 2023 proxy season, 27% of TSX60 companies have disclosed plans to adjust ESG metrics and/or weighting in their incentive programs. Although the level of detail included in prospective disclosure varies, several notable examples suggest that many of the trends noted this year’s proxy season will continue to gain traction in future years.

For example, Suncor implemented a “climate PSU” with a 5% weight in the company’s LTIP mix in FY2022. This LTIP instrument is completely tied to the company’s environmental objectives, with performance assessed based on progress relative to the company’s climate initiatives, a more “process-oriented goal.” Suncor announced that going forward, climate PSUs will incorporate a formal target for emissions reduction by the end of 2025 as a step towards the company’s 2030 goal (among other changes to the program).

Another example is Sun Life, which plans to add a sustainability modifier that can adjust the PSU score by +/- 10% based on the achievement of 4 goals related to sustainable investment, gender and ethnic diversity representation, and GHG emissions reduction.

We anticipate that additional companies will implement similar changes for FY2023, although they did not prospectively disclose their intentions in their proxies.

Conclusion

As companies' ESG strategies have evolved, their integration into compensation has also become more robust, as demonstrated by this year’s shift in both the type of metrics and quality of disclosure. More companies are disclosing specifics around their ESG metrics including targets, how performance was evaluated, and the weight of metric(s) within their plan, and we expect a continued intensification of these themes next year.

When Boards discuss the integration of ESG into compensation, we advise rooting the conversation in guiding principles: What is the organization’s ability to effectively develop and manage the program, and what are they trying to accomplish?

It can be useful for Canadian companies to understand trends among the TSX60, as they are often first movers on emerging governance and compensation practices. That said, an understanding of market practice is one of several important factors that may be considered by the Board and Management when determining how a company could feasibly implement ESG in compensation today.

1 OSFI Climate Risk Management Guideline (March 2023)

2 SEC Proposes Rules to Enhance and Standardize Climate-Related Disclosures for Investors (March 2022)

3 Investors for Paris Compliance: "99% of Cenovus Shareholders vote in favour of our climate transparency resolution" (April 2023)

4 We note that 56 constituents were consistent year-over-year and 4 new constituents were added to the index in 2023.

5 Methodology is based on weighting as a % of STIP or LTIP (i.e., both corporate and individual components), for only those companies that include ESG metrics in their plans