In Part II of our Say on Pay series, Hugessen explores the impact of proxy advisor recommendations on Say on Pay votes – see Part I (link) for the most common rationale of low Say on Pay outcomes.

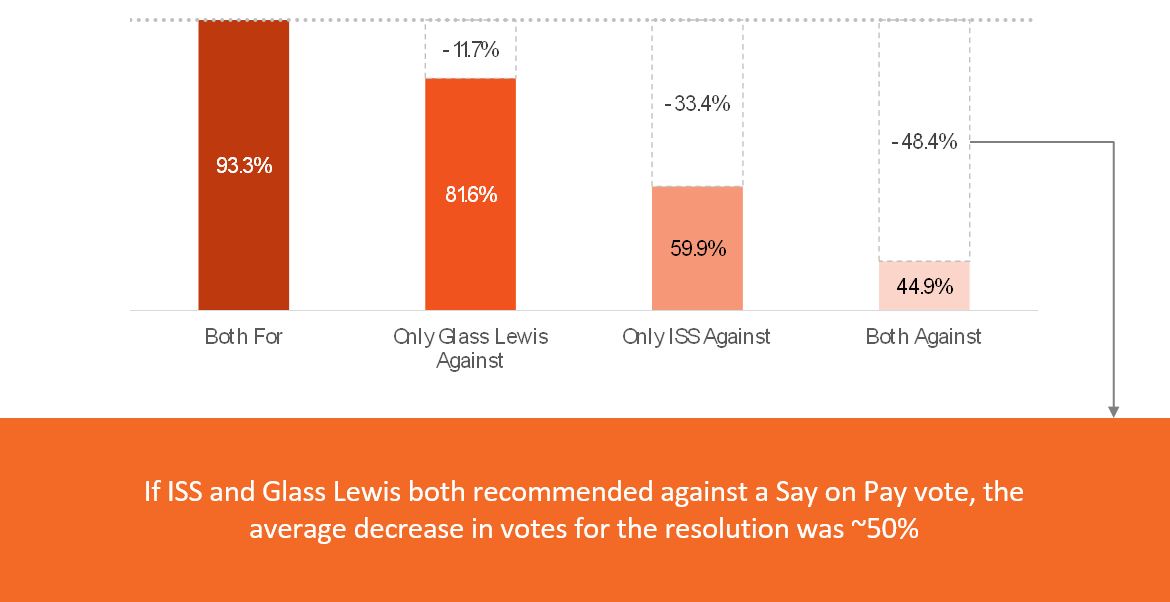

Our analysis found that when ISS and Glass Lewis recommend voting against a company’s Say on Pay, on average, there is a ~50% decrease in votes for the resolution. We also find ISS recommendations have a more significant impact on voting results vs. Glass Lewis (-33% and -12% impact on voting results, respectively).

Background & History

Say on Pay is a non-binding advisory vote which allows shareholders to voice their approval with the Board’s approach to executive compensation. Shareholders have the option to vote “For”, “Against”, or abstain from voting on Say on Pay. Standard practice is to hold an annual Say on Pay vote in order to gather shareholder support relative to any year-over-year changes to pay levels and incentive design. Given the advisory nature of the vote, the results are non-binding, and therefore, the Board is under no obligation to enact any specific corrective measures in the event of a failed vote.

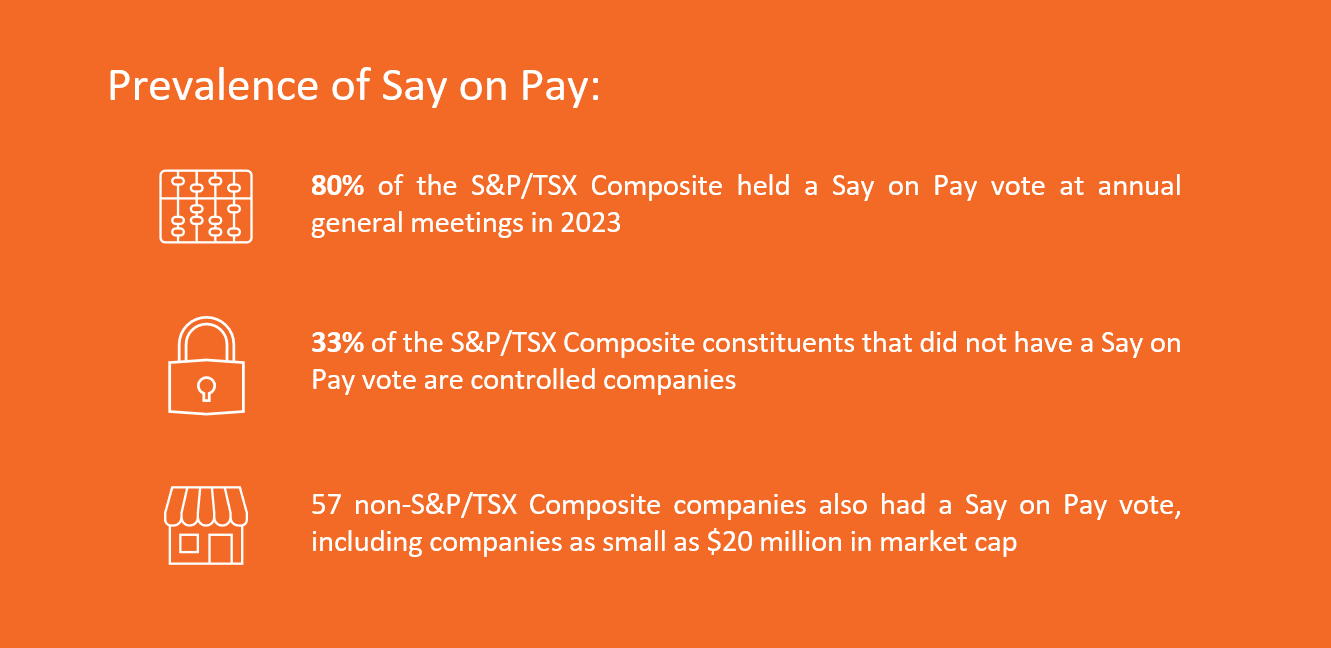

Say on Pay votes have become common among S&P/TSX Composite firms where almost 80% of firms had a Say on Pay resolution for shareholder meetings in 2023. Of the companies that did not have a Say on Pay vote, 33% are controlled companies (i.e., dual share class, significant shareholder). Over the same period, a notable number of firms outside of the S&P/TSX Composite (n=57) also had a Say on Pay vote, suggesting that an increasing number of smaller companies are adopting the vote (firms had market capitalizations as small as $20M, with an average of $500M).

Influence of Proxy Advisors

Annual general meetings are heavily concentrated in the second quarter of each calendar year, which poses a challenge for institutional investors who need to vote on each resolution (e.g., director elections, equity reserve requests, Say on Pay). Proxy advisors support these investors by providing their voting recommendations based on the various facts presented in public disclosures. On compensation, they assess pay programs using propriety models and publicly disclosed voting guidelines to ultimately decide if a For / Against / Withhold vote is warranted for Say on Pay resolutions.

The two largest proxy advisor firms are Institutional Shareholder Services (ISS) and Glass Lewis. While their Canadian market share has not been documented, it is estimated that together they account for more than 90% of the proxy advisor market in the US 1 , with ISS alone representing a significant portion of the market. A notable amount of academic research has been conducted in the US to assess the impact of ISS and Glass Lewis voting recommendations, including Say on Pay results.

The following independent analysis conducted by Hugessen is intended to assess how ISS and Glass Lewis voting recommendations impact Say on Pay results of Canadian firms.

Key Statistics

Hugessen reviewed all annual general meetings of Canadian publicly traded companies (both within and outside of the S&P/TSX Composite) that occurred between 2019 and 2023. We isolated companies that were measured against ISS and Glass Lewis’ Canadian proxy voting guidelines (i.e., excludes issuers that are cross-listed and assessed based on US voting guidelines). This sample includes over 1,000 Say on Pay voting resolutions where we were able to obtain voting data and proxy advisor voting recommendations 2.

In order to control for any upward biases in Say on Pay results, we excluded all controlled companies where the controlling shareholders will always vote with management (e.g., companies with dual share class structures and / or where strategic investors have more than 50% voting control).

Overall Voting Results

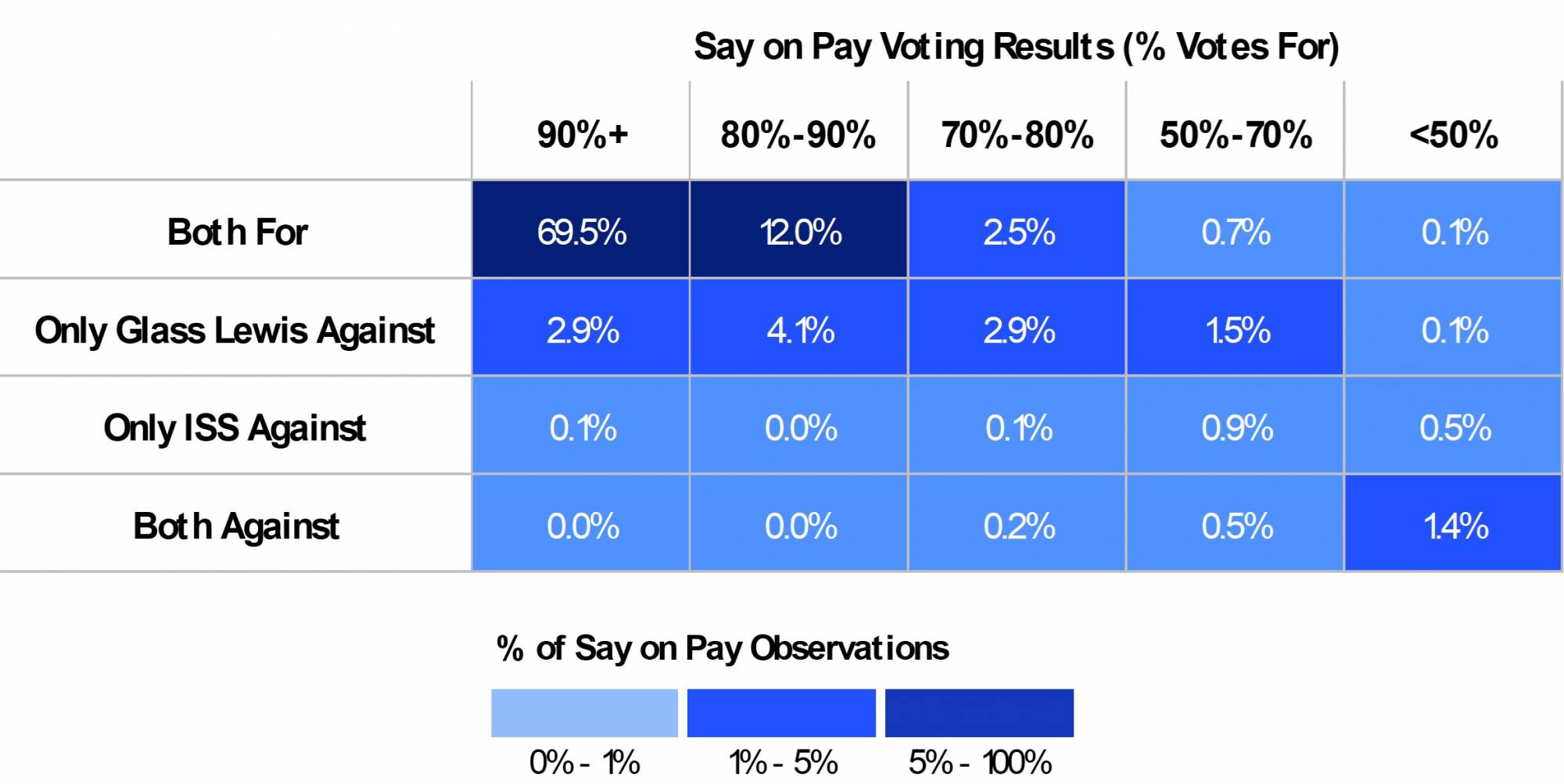

ISS and Glass Lewis generally recommended voting “For” on a majority of Say on Pay recommendations, which typically resulted in a Say on Pay outcome of 90%+ (see Figure 1). However, we note there were situations where shareholders voted contrary to ISS and Glass Lewis recommendations. This suggested that (i) a company’s executive compensation program may not have aligned with the respective shareholder’s voting guidelines (e.g., will not support companies that have “excessive executive pay” ) and / or (ii) there may be additional factors under consideration beyond pay and performance (e.g., Aimia failed their Say on Pay vote in 2023, but this result was likely influenced by the proxy contest during this time).

Figure 1: Distribution of Say on Pay Voting Results from 2019-2023

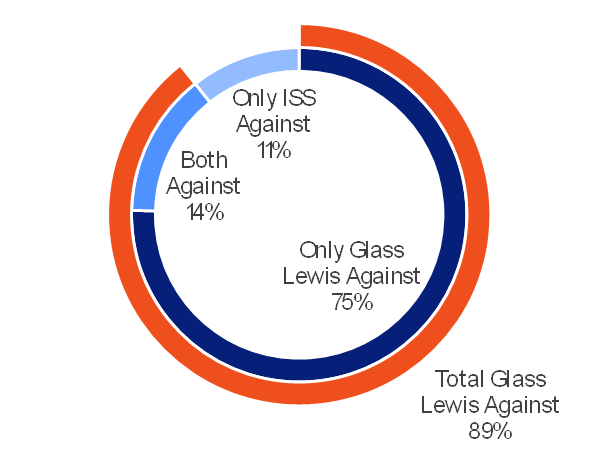

Between the two proxy advisors, ISS less frequently issued “Against” recommendations as compared to Glass Lewis (see Figure 2). For example, if Glass Lewis recommended voting against a company’s Say on Pay resolution, ISS will only recommend against the company in approximately 16% of those situations. However, an ISS “Against” recommendation is typically more impactful (see below for more details).

When both firms recommended voting against companies, there were some instances where companies still received a result above 50% (e.g., Cineplex, Obsidian, Tilray, Blackberry, Aurora). However, these are still poor outcomes (given that the standard is typically 90%+), and except for Aurora Cannabis’ vote in 2023, these observations only occurred during meetings in 2021 (i.e., reviewing pay and performance in 2020) suggesting shareholders may have been more lenient given the significant impacts of COVID-19. We also note that within this group there are a number of companies that received consecutive years of “Against” recommendations from ISS and Glass Lewis (e.g., Agnico Eagle, BlackBerry, CI Financial).

Figure 2: Breakdown of Proxy Advisor Against Recommendations

When ISS and Glass Lewis both provided a favourable recommendation, the average result was 93.3% in favour of the resolution (see Figure 3). If there was a split vote recommendation where one proxy advisor recommended in favour while the other recommended against, ISS tended to have a more meaningful impact to voting results than Glass Lewis (decrease of 33.4% and 11.7%, respectively). When both recommended voting against the resolution, the average result was a decrease of almost 50% (i.e., decrease from an average result of 93.3% to 44.6% in favour of the resolution), resulting in the average company failing their Say on Pay vote (i.e., <50% voting in favour).

Figure 3: Average Say on Pay Results Segmented by Proxy Advisor Recommendations

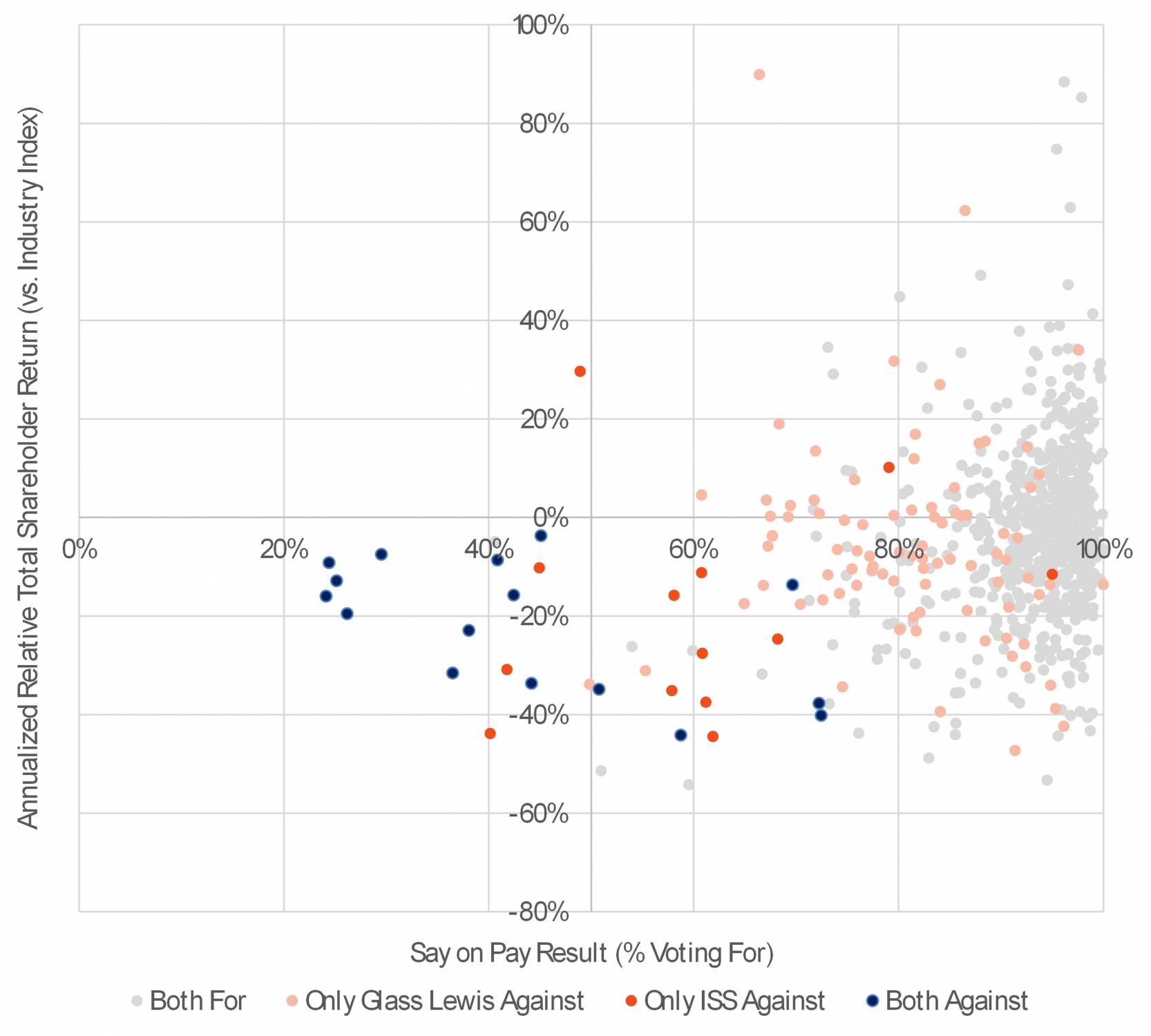

Impact of Shareholder Returns

In Figure 4 below, we compare relative total shareholder returns against actual Say on Pay results, with the colours indicating proxy advisor recommendations. We found that companies with weaker relative total shareholder returns more often received "Against" recommendations from both proxy advisors, and in turn are more likely to fail their Say on Pay vote (see bottom left quadrant).

Figure 4: Voting Results vs. Relative Shareholder Returns, including Proxy Advisor Voting Recommendations

Based on our observations of situations where only ISS recommended “Against”, it suggests that ISS puts a greater weighting on relative total shareholder return performance. A majority of the data points where ISS gave an unfavourable voting result consisted of companies that underperformed the industry.

Among the situations where only Glass Lewis recommended voting against, 37% had a positive relative total shareholder return (i.e., outperformed industry), suggesting that the recommendation was driven by other financial / operational factors that underperformed versus peers and / or problematic pay practices.

However, when looking at the broader dataset, only 17% of companies that underperformed their industry on total shareholder return received an “Against” Say on Pay recommendation from either proxy advisor.

This suggests that while total shareholder return is an important factor, it will not be the sole determinant of a company’s Say on Pay success. In our experience, the combination of underperformance with unaligned pay decisions / practices will typically result in an “Against” recommendation from proxy advisors.

Considerations for Companies

While our analysis was focused primarily on proxy advisor voting recommendations, voting results, and relative returns, there are a number of other factors companies should consider when navigating their annual Say on Pay vote:

- Compensation Program Review3 – Companies with a Say on Pay vote should review their programs to determine whether they are aligned with industry best practices and if not, describe in public disclosures (e.g., management information circulars) why they might differ given company specific circumstances. Disclosure is especially important to allow shareholders and proxy advisors to make an informed decision on whether or not a company’s pay programs are appropriately structured.

- Pay-for-Performance Alignment – Each proxy advisor has their proprietary methods of assessing if compensation outcomes are aligned with company performance, along with a broader assessment of a company’s pay programs. If there is a strong / direct link between compensation paid to named executive officers and company performance, ISS and Glass Lewis may provide a favourable recommendation even if a company has underperformed peers.

- Conducting Simulations – Companies can conduct simulations to emulate proxy advisor pay for performance tests and estimate the potential outcomes. This will allow firms to anticipate and proactively address shareholder concerns on executive compensation.

- Only a Recommendation – Proxy advisors will influence voting outcomes for companies, but institutional shareholders will ultimately vote based on their own policies. There may be situations where shareholders have policies that are more stringent than ISS and Glass Lewis, and thus it is important to understand a company’s shareholder base, highlighting the need for shareholder outreach to better communicate the specific company circumstances.

- Shareholder Outreach – Having both proxy advisors recommend against a company’s Say on Pay vote will likely result in a poor outcome or a failing result. While not much can be done after receiving dual unfavourable voting recommendations, companies can quickly pivot following a failed Say on Pay vote to prepare for the following year’s vote. This includes early communication with the companies’ largest shareholders on early considerations of changes to the executive compensation program. Furthermore, firms may consider distributing a broader communication to all shareholders to signal expected changes – see RioCan’s press release following a failed Say on Pay vote in 2021 4.

References

1 Proxy Advisors And Market Power: A Review of Institutional Investor Robovoting (link)

2 Data sourced from Diligent’s Market Intelligence Voting Module, Hugessen’s internal databases, and public disclosures

3 For more information and on the most common reasons ISS and Glass Lewis will issue an against recommendation, see our previous article where we explore the most commonly cited issues (link)

4 RioCan Real Estate Investment Trust Announces Changes To Executive Compensation Program (link)