A Total Variable Compensation (“TVC”) incentive program offers a unique approach to incentive compensation, blending elements of traditional short- and long-term incentive structures (“STIP” and “LTIP”). In this briefing, we shed some light on what it is, how it works, and key considerations for its implementation.

What is a TVC Structure?

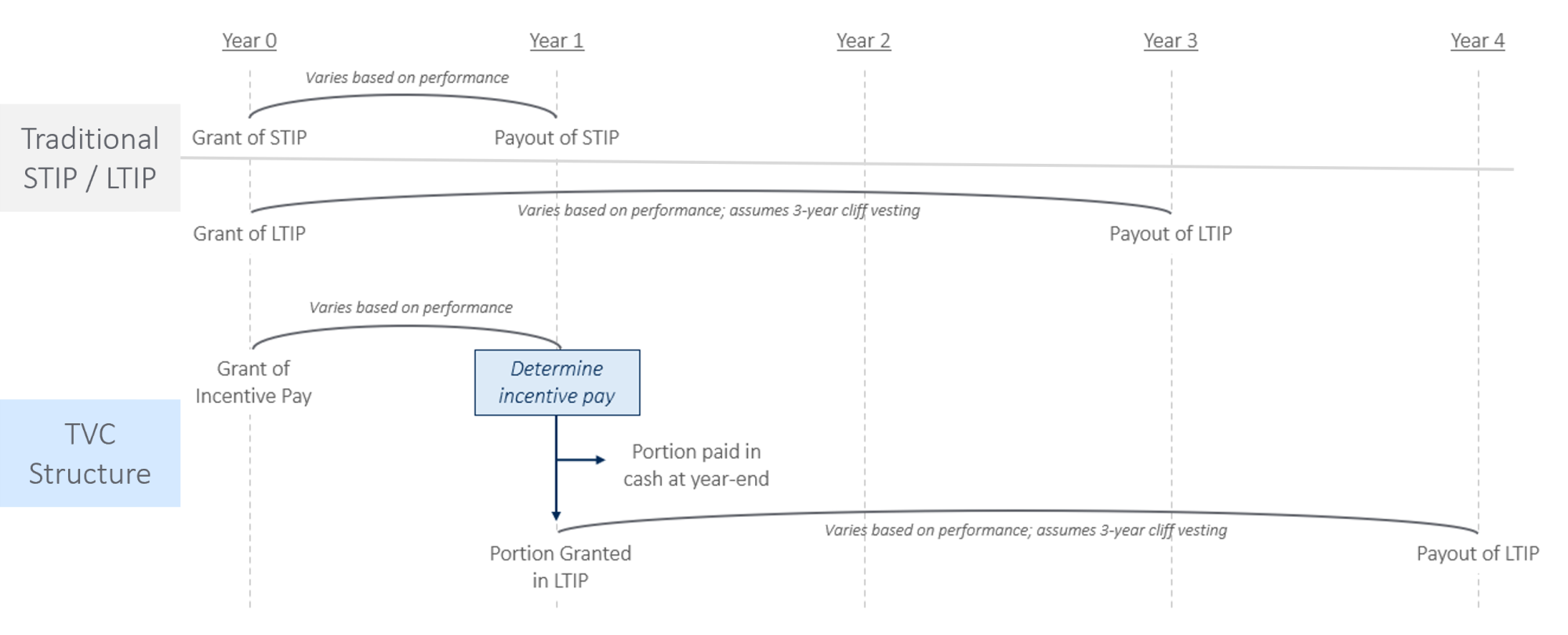

A TVC structure is an approach to incentive compensation whereby the total pool of variable pay is linked to an assessment of performance and then allocated between short-term and long-term incentives. In other words, at year-end, performance is assessed, with a portion of compensation paid out immediately and the remainder deferred over time, typically through long-term incentive vehicles such as Performance Share Units (PSUs), Restricted Share Units (RSUs), or Stock Options (see Illustration 1).

Simplified example, assuming 3-year vesting of LTIP instruments. For a more detailed example, see Appendix 1

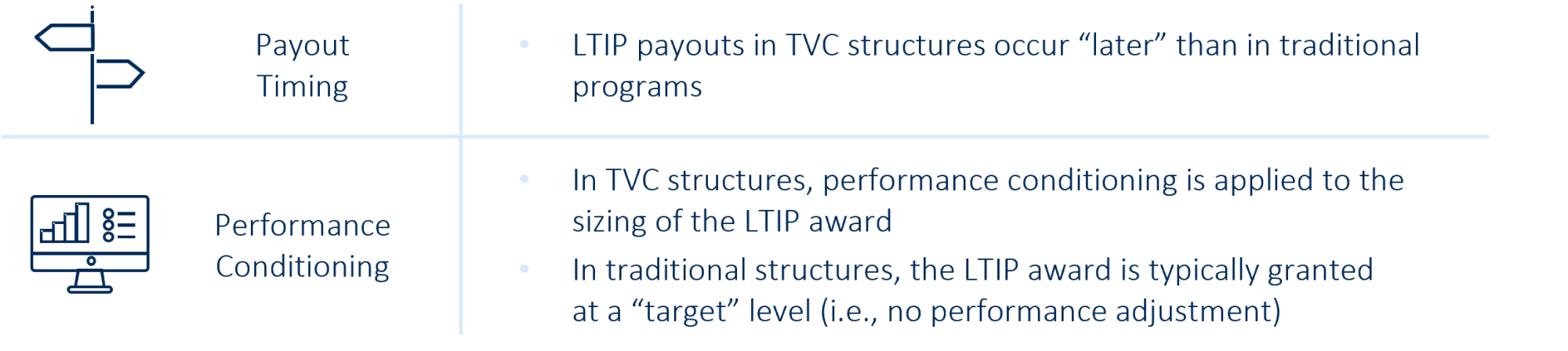

Mechanically, TVC structures are similar to traditional short-term incentive plans, except that both the annual cash bonus and the grant-date fair value (“GDFV”) of long-term incentives is driven by the same performance assessment, typically over a one-year period. This can have nuanced but distinct differences:

Key Advantages & Market Context

In Canada, TVC structures are most commonly used at financial institutions, pension funds, and asset management firms. These organizations adopt TVC structures for a variety or reasons, most often to facilitate “longer-term” incentive deferrals and reinforce pay-for-performance principles. Like traditional incentive structures, organizations use TVC programs to support cultural alignment and provide consistent messaging to all employees. The structure also enables greater flexibility in year-end decision-making and disclosure, allowing the determination of the total incentive award, not just the STIP payout as is typical in traditional frameworks.

“Longer-Term” Deferral & Formulaic Variable Pay

A key draw of TVC structures is to provide long-term deferral relative to traditional incentive models. In a TVC structure, incentive pay is determined at year-end based on some measure(s) of performance, with a portion paid out and a portion deferred into traditional LTI instruments. This contrasts to traditional models where LTI awards are typically granted at the beginning of a fiscal year. By delaying the grant of LTI to year-end, the overall deferral period is longer (e.g., PSUs cliff vest at the end of Year 4 rather than Year 3, see Illustration 1), supporting both retention and longer-term focus across the organization. This can be of particularly use for companies focused on risk, such as financial institutions, where material risk takers are subject to longer-term deferrals.

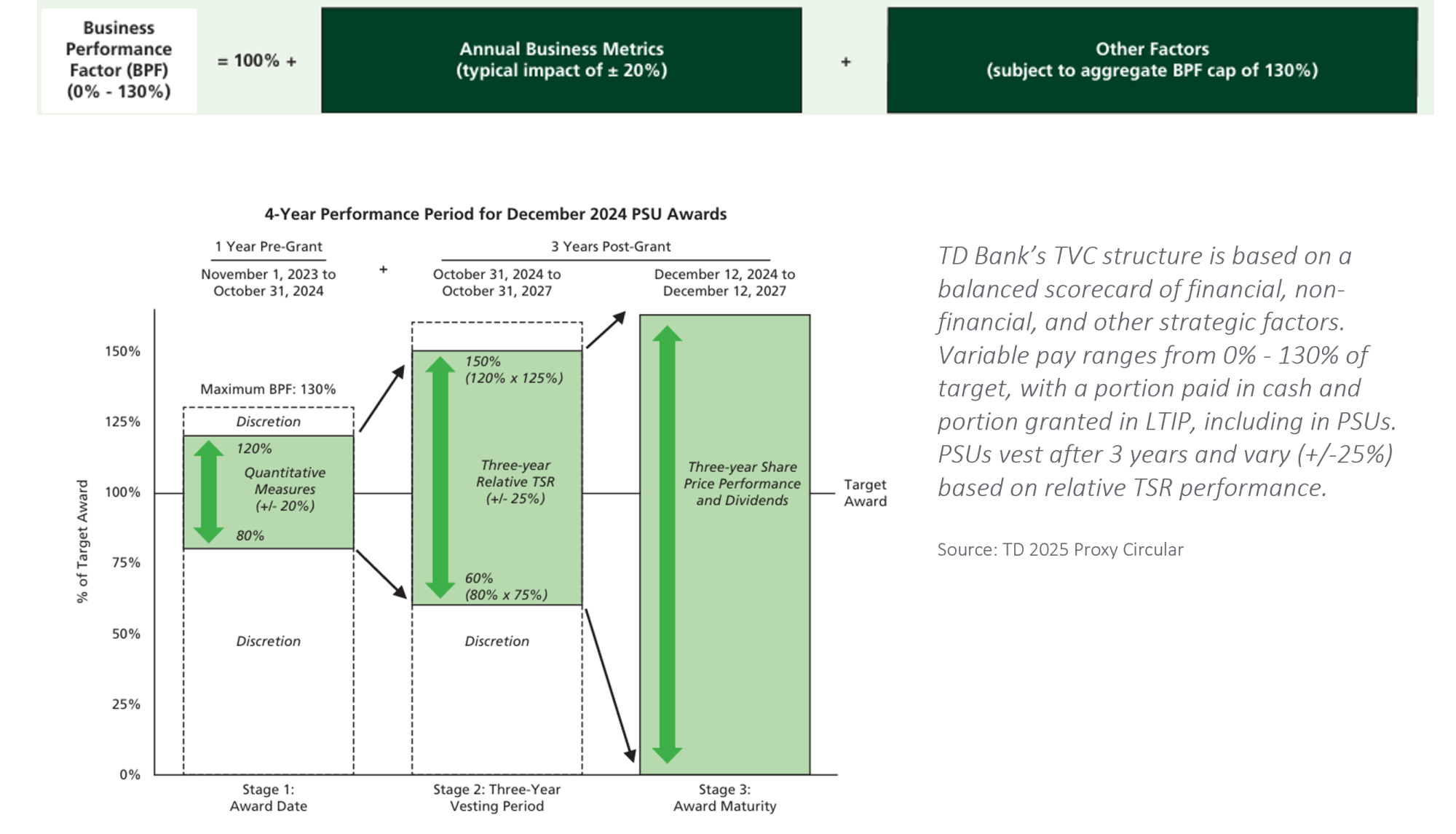

TVC structures also apply “front-end” performance conditioning to all LTI awards, including instruments typically linked solely to share price performance (e.g., stock options and RSUs). As a result, all components of variable pay are linked to specific measures of performance. By introducing variability in long-term incentive instruments and directly linking all elements of variable pay to performance measures, organizations can strengthen a pay-for-performance culture and enhance transparency in compensation decisions (see Case Study: TD Bank).

Case Study: TD Bank

Cultural Alignment / One Team Mindset

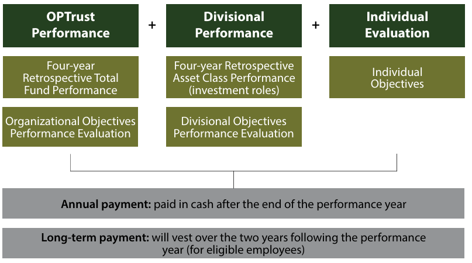

Like other incentive programs, TVC structures can be powerful and flexible communication and alignment tools. In Canada, this can be observed among major pension plans who often link total variable pay to a mix of measures, including overall organization, divisional / asset class, and individual goals. This dual approach rewards performance within individual asset classes while promoting shared accountability and cross-team collaboration (see Case Study: OPTrust).

Case Study: OPTrust

At OPTrust, a major Canadian pension plan, employees participate in a “One Plan” whereby all employees are assessed on shared corporate measures (Total Fund, Org. Objectives), divisional goals, and individual objectives. While the weightings and divisional/individual goals may differ by employee, the overall framework is applied consistently across the organization. All employees have a weighting on “total fund” performance, promoting a “one-team” mindset.

Source: OPTrust 2024 Funded Status Report

Flexibility to Determine Total Annual Incentive

With a TVC structure, decisions on both STIP payouts and LTIP grants are made at the same time, at year-end. For a given fiscal year, in traditional programs, these decisions are often split: LTIP grants are made at the beginning of the year, while STIP payouts are decided at year-end. Having a single decision point can make it easier for companies to see, and for publicly traded companies to disclose, the full picture of pay for the year. It also provides greater flexibility to align total annual compensation with actual performance, as both STIP and LTIP awards can be determined and adjusted accordingly.

Key Considerations

Implications of the One-Year Performance Period

Most TVC structures have a one-year performance period sizing both annual cash and the grant size of long-term incentives. While this provides performance conditioning on all components of pay, in some scenarios, this could potentially create pressure to focus on short (i.e., annual) performance compared to a traditional structure. To overcome this dynamic, many organizations place heavier weighting on long-term incentives within the pay mix. While the grant may still vary, significant exposure to longer-term performance goals helps maintain participant focus on the long-term success of the organization.

Defining and Managing Variability

By design, TVC structures can lead to greater variability and / or leverage in pay outcomes. In periods of sustained strong performance, this can result in high payouts, while in periods of underperformance this can lead to low payouts. The variability relative to traditional programs reinforces the importance of defining an appropriate pay philosophy which considers factors like business strategy, talent dynamics, performance culture, and industry norms. A key tension to navigate is the balance between incentive “stability” and performance sensitivity. For instance, some organizations may seek greater “leverage” (i.e., variability) to incentivize outperformance, while others may value more relative stability in payouts year-over-year.

To manage variability, organizations can adjust various design levers, including LTIP instruments used, payout ranges, metric selection, and target calibration. For instance, a company seeking to offer greater long-term incentive opportunity might grant PSUs within the TVC model to allow for a broader payout range than the traditional 0 - 2x PSU. In contrast, organizations favouring less variability may limit the use of levered instruments (e.g., PSUs or stock options), use a mix of diversified measures (to “smooth” aggregate impact), or calibrate measures with broad performance shoulders. In some cases, variability may be reduced by defining a narrow payout range relative to traditional structures (i.e., 90 – 110% vs. 0 – 200%). In either case, there are a range of levers available to organizations to tweak the program to best fit their philosophy and needs.

Impact of Sustained Under & Overperformance

In periods of sustained underperformance, the inherent variability of TVC structures can result in consistently low pay over a multi-year period (particularly within the LTIP). This can potentially raise retention issues. For example, several years of below target TVC payouts will result in significantly lower LTIP grants, limiting the upside leverage / earning potential compared to if awards were granted at target, as in a traditional program. This may demotivate employees who see limited opportunity to “earn back” pay over the LTIP’s performance period. In contrast, in periods of sustained outperformance the reverse is true. Participants can receive “higher” LTIP grants than traditional programs, resulting in (all else equal) higher earning potential.

For some companies, this variability is a desired and natural outcome of an intentional pay-for-performance philosophy. For others, greater stability is desired, and therefore calibrate their programs to mitigate against potentially extreme outcomes. This may include defining minimum and maximum levels of LTI grants (“floors” and “caps”) or adjusting the LTIP instrument mix (e.g., use of RSUs to limit additional variability). In any event, there are a variety of levers organizations can use to effectively calibrate the program to fit any unique circumstance or pressures.

Note on Complexity

Depending on its design, a TVC approach can combine multiple incentive vehicles, performance metrics, and multi-step calculations for pool funding and allocation, creating a framework that may not be immediately intuitive. This complexity can be effectively managed through clear communication and the use of visual aids that detail the structure. By illustrating how performance translates into tangible rewards, organizations can ensure that all parties understand program mechanics. Additionally, a well-defined pay philosophy can guide decisions regarding program complexity, ensuring that it effectively meets company objectives and serves the needs of the workforce.

Is a TVC structure the Right Fit?

Like any incentive program, choosing to implement a TVC structure is a strategic decision that should align with a company’s pay philosophy, priorities, and talent needs. A TVC model is particularly valuable for organizations that:

- Want to reinforce the direct connection between pay and performance.

- Can generally set robust performance goals.

- Want to promote a greater “one-team” mindset among its workforce.

- Seek to unify all participating employees on a singular, but adaptable incentive framework.

- Desire to add performance conditioning to long-term incentives, but are not yet ready for PSUs.

Conclusion

When thoughtfully designed and implemented, a TVC structure can be a powerful tool for aligning pay with performance, fostering collaboration, and providing organizations with the flexibility to tailor incentives to their strategic objectives. While TVC structures require careful calibration to balance variability, complexity, and performance measurement, they offer a compelling alternative to traditional incentive programs, one that can reinforce accountability, drive engagement, and support long-term value creation.