For companies considering an initial public offering (IPO), an important factor to carefully consider is the design of the long-term incentive plan (LTIP). The size of the share reserve and its allocation can play a pivotal role in ensuring a compelling and responsible compensation opportunity for the management team. To gain insights into prevailing LTIP practices, Hugessen conducted extensive research focusing on 45 IPOs listed on the Toronto Stock Exchange. These IPOs had market capitalizations ranging from approximately $100 million to $10 billion, spanning the period from 2015 to 2021.

Key Definitions

-

Common Shares Outstanding (CSO): Total number of common shares that a publicly traded company has issued and that are currently available for trading by investors.

-

Share Reserve: Pool of authorized but unissued common stock that is set aside for future grants as part of the equity- based compensation plan, typically denoted as a number of shares or percentage of CSO.

-

Rolling Plans: Equity-based compensation plans where the share reserve is stated as a percentage of the CSO and is automatically replenished as securities are issued from the plan.

-

Fixed Plans: In contrast to rolling plans, fixed plans allocate a set number of shares as the share reserve for the company's equity-based compensation plan. The number of shares remains fixed and does not change automatically based on the CSO.

-

Dilution: Dilution occurs when new shares are issued as a result of outstanding awards being settled under the equity plan. This results in a decrease in ownership percentage for existing shareholders.

-

Burn Rate: Rate at which the share reserve is utilized or reduced each year, usually expressed as a percentage of the CSO. It indicates the rate at which the value of investors' holdings in the company is expected to be diluted due to the granting of equity awards.

-

Named Executive Officers (NEOs): NEOs refer to the CEO, CFO, and the next three highest-paid executive officers within a company, as disclosed in the company's annual Management Information Circular.

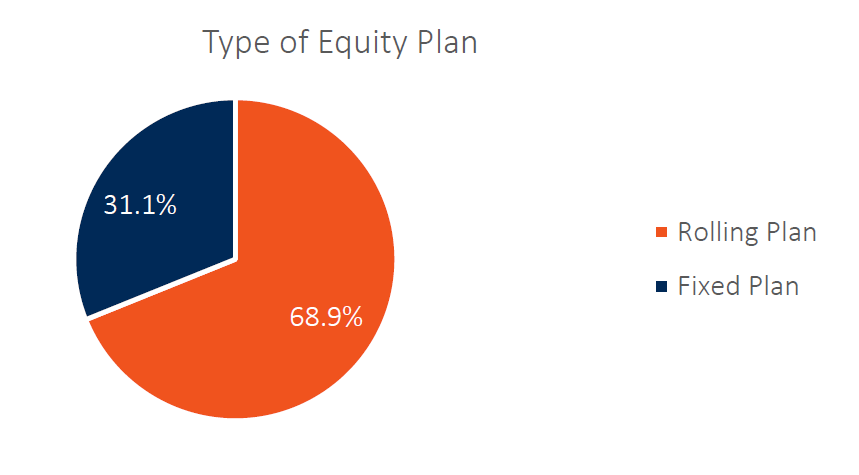

Rolling vs. Fixed Plans

Of the 45 companies examined, 69% (n=31) implemented a rolling plan at the time of their IPO, while the remaining 31% (n=14) opted for a fixed plan. Rolling plans automatically replenish, hence, the total number of shares available for issuance grows over time. The TSX requires rolling plans to be re-approved by shareholders every three years.

Size of Share Reserve

Among the companies analyzed, a majority of 27 out of 45 (60%) chose to set aside a 10% share reserve for their equity-based compensation plans. Historically, institutional shareholders have generally viewed equity plans with up to 10% dilution to be reasonable. In some cases, higher levels of dilution may be deemed acceptable for emerging growth or recent IPOs.

Dilution and Share Reserve Remaining After IPO Year

We observe a wide range in dilution levels and the size of share reserve remaining after the first year post-IPO.

Burn Rate

The burn rate in the first year post-IPO varied significantly across the observed companies. Anecdotally, burn rates tend to be higher in the initial years following an IPO compared to more established and stable companies. It is also worth noting that some companies opt to grant substantial equity awards shortly before their IPO, followed by a decrease or absence of equity awards for a period afterward.

LTIP Instrument Prevalence

During the first year post-IPO, the granting of stock options, restricted share units (RSUs), and performance share units (PSUs) differed among the companies analyzed. Among companies that granted LTIP, approximately 57% used a single LTIP instrument, often stock options, while 35% used two instruments, and 8% employed all three. Notably, the granting of PSUs was relatively less common in the first year post-IPO compared to the usual practices among larger and more mature companies. Stock options and RSUs are linked to share price performance and represent simple approaches to equity-based compensation.

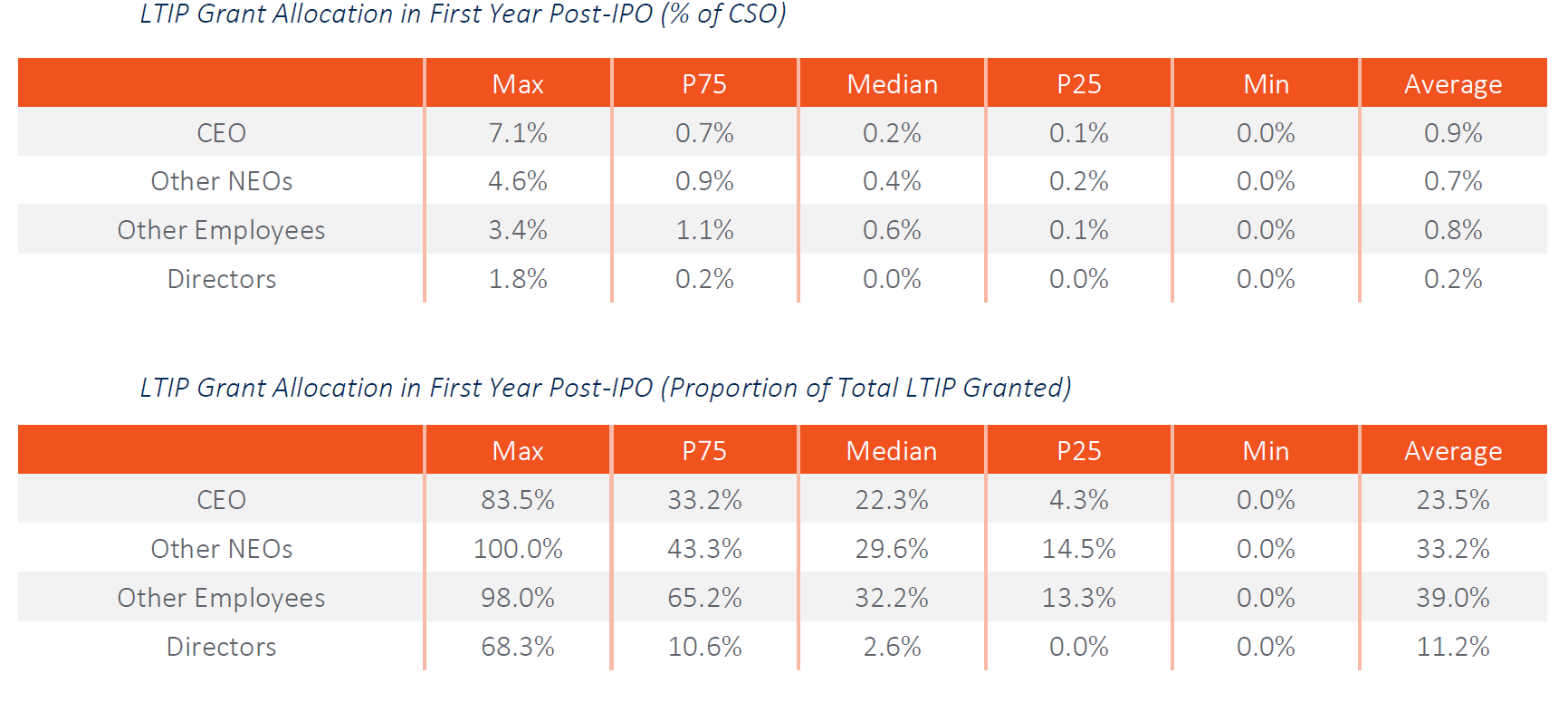

LTIP Grant Allocation

Analysis of LTIP awards granted during the first year post-IPO indicated that CEOs typically received a notable proportion of the total LTIP granted. Allocation to non-NEO employees exhibited wide variation. Generally, the board of directors received a smaller proportion or no LTIP grants, with some exceptions. Anecdotally, over time as the company becomes more mature the distribution of LTIP grants tends to balance out between the CEO and other NEOs, reducing the concentration on the CEO.

Conclusion

Since achieving record-breaking levels in 2021, the IPO market has encountered a notable deceleration. Challenges have emerged due to factors such as rising interest rates and declining valuations within the technology sector. Nevertheless, there are reasons for optimism. The peaking of inflation and the softening of energy prices contribute to a more favourable market outlook. As market stability returns and investor confidence strengthens, companies that previously delayed their IPO plans are expected to regain traction and resume the listing process. In light of this, it is crucial for companies pursuing IPOs to consider the range of practices and strategies related to executive compensation that can effectively support their objectives.