This article is the final part of our six-part ESG series and focuses on key considerations for calibrating and setting targets when incorporating ESG metrics into incentive plans. After identifying the most relevant ESG metrics for inclusion into compensation plans, ensure metrics are set and calibrated appropriately so that they strike the right balance between “achievable” and “stretch.”

The prior instalment in our series outlined considerations for the determination of weights for ESG metrics. The following article will address the next step when incorporating ESG metrics into compensation plans – setting targets and calibrating performance curves.

The following factors should be considered when determining ESG targets within a company’s STIP and/or LTIP:

- How to align long-term nature of ESG goals (e.g., 2030 and 2050 targets for GHG emissions) with interim timelines (i.e., typical incentive plan metrics – 1 to 3-years)

- Ability for the metric to be scalable (i.e., can perform at, above, or below target)

- The confidence in forecasting targets, and shoulders, to reduce the need to apply discretion

See below for more details on these considerations, including detailed examples and illustrations.

1) Aligning Long-Term Nature of Goals with Interim Timelines

Many ESG measures may be aligned with longer-term goals (i.e., 5+ years), which can pose difficulties for target setting (i.e., shorter timeframe for compensation plans) – incorporating interim targets may be appropriate in these cases.

When setting interim targets, companies should have a detailed understanding of how these targets will progress them towards their longer-term, publicly disclosed, goals. Furthermore, it is important and helpful for external parties and stakeholders if the communication surrounding longer, and interim targets is transparent (i.e., provides stakeholders greater confidence that the Company is on track to achieve long-term goals).

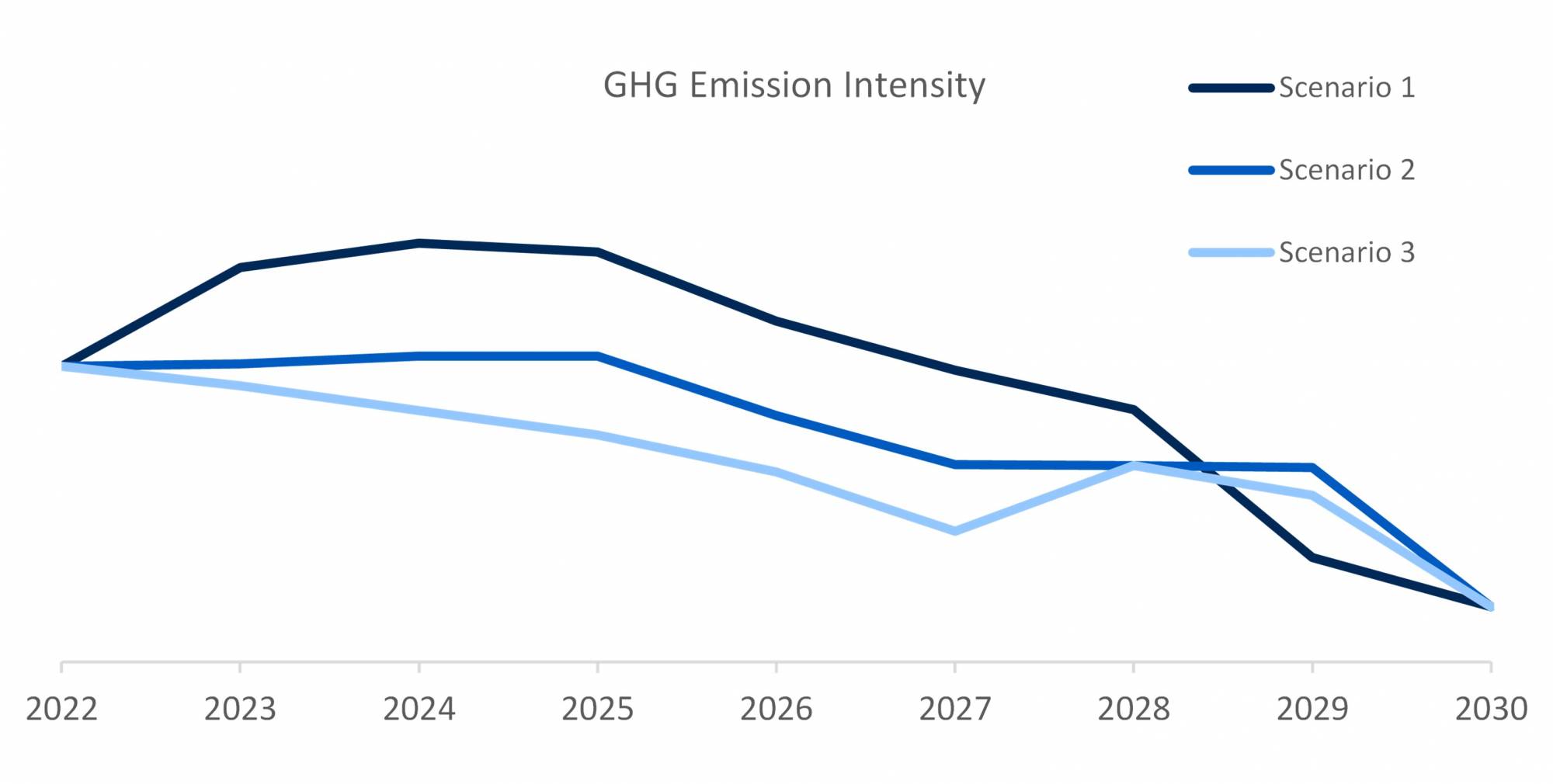

However, interim targets may not always be linear and may appear negatively impacted in early years before clear progress is presented (see below for an example outlining a number of illustrative scenarios).

- There are different paths to reduction; consider implications to 1 – 3-year incentive plan targets

- There are many external factors that can influence metrics – consider stress-testing under different scenarios prior to inclusion to understand the influence external variables can have

- It is important to continuously monitor the achievability of the targets that have been set

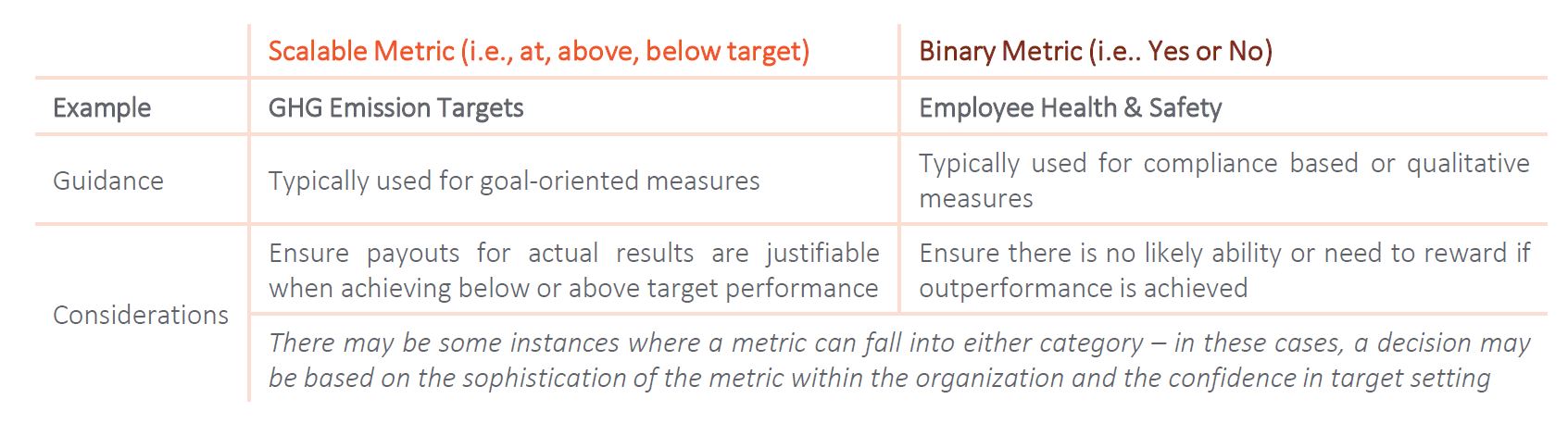

2) Choosing Between Scalable and Binary Targets

The messaging around scoring and payouts of ESG metrics need to be well considered and defensible both for internal and external stakeholders to incentivize the desired behaviours. Furthermore, deciding if the performance multiplier attached to the ESG metric can exceed target performance may differ depending on the metric – see below for more details:

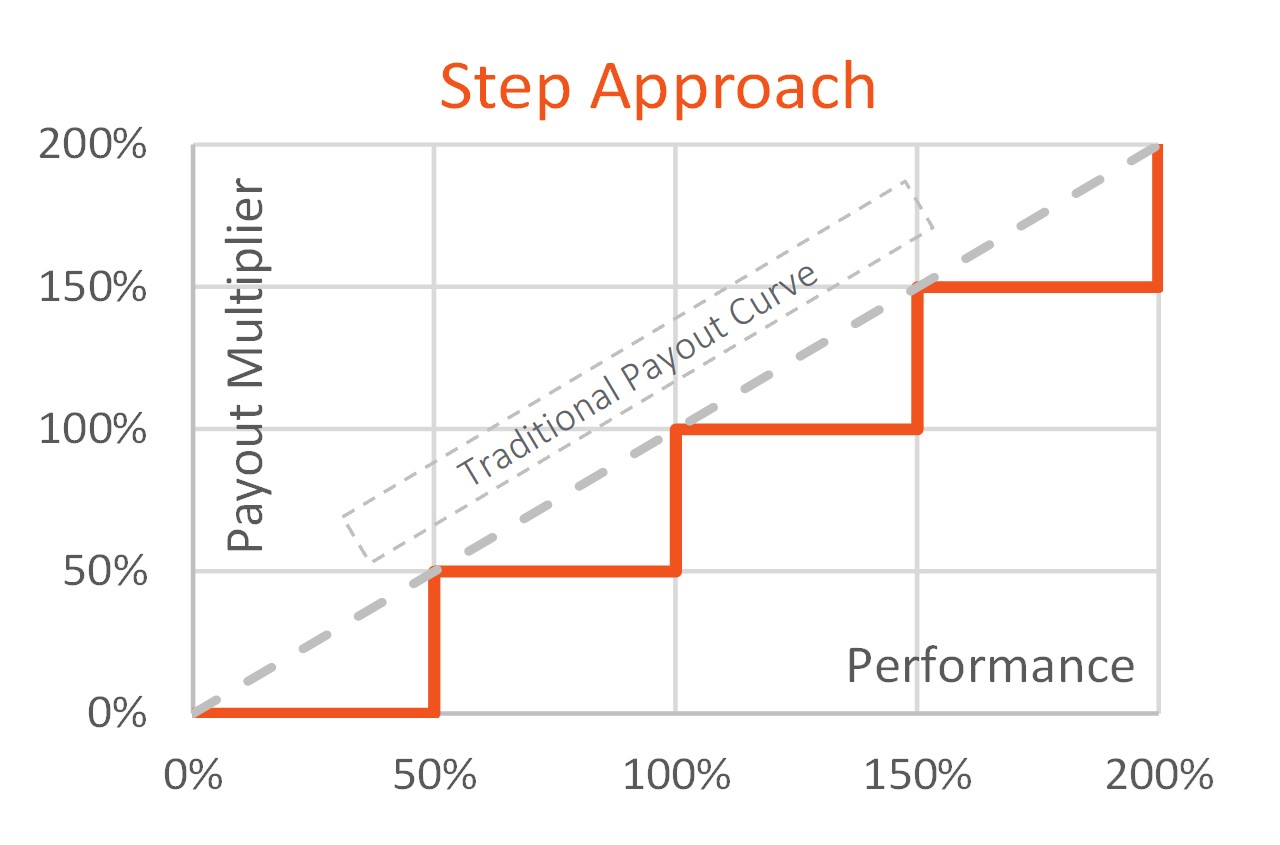

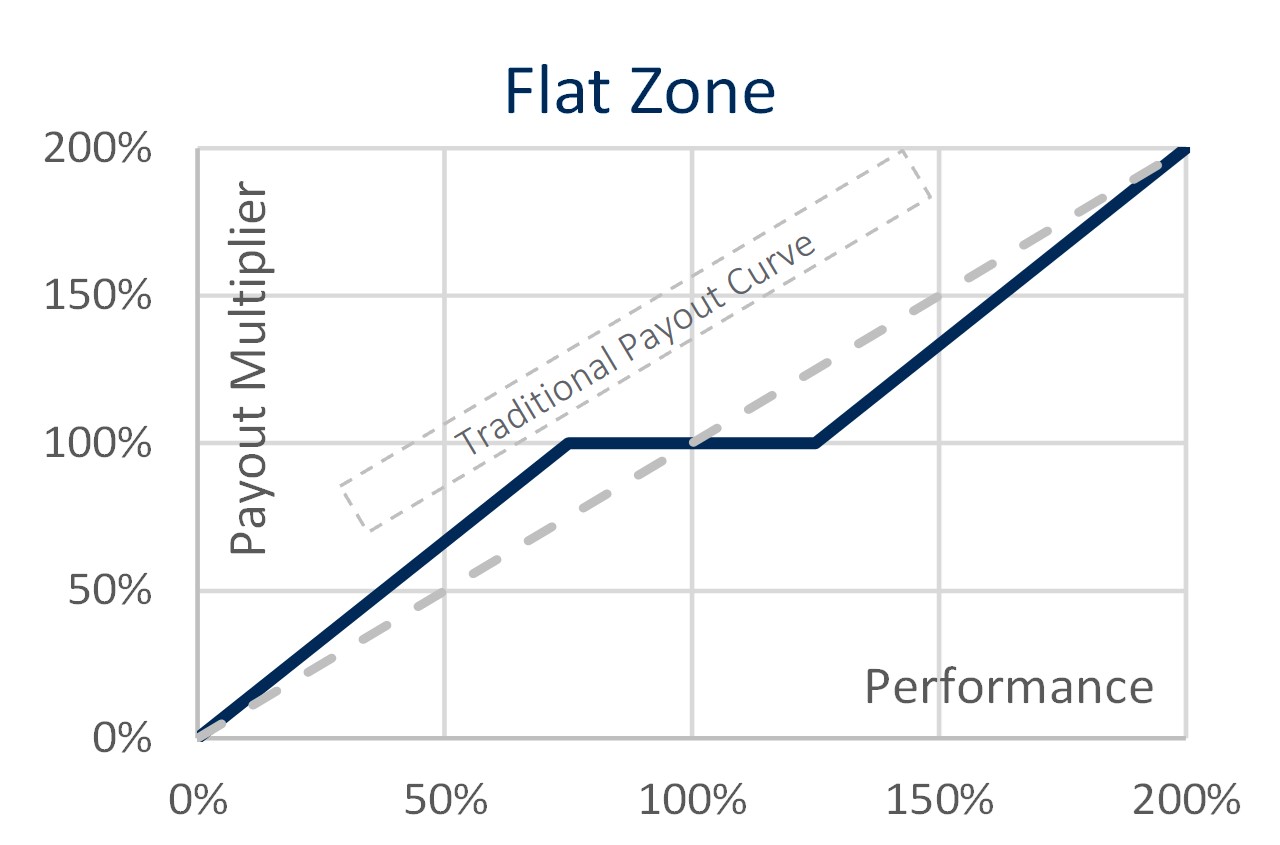

3) Calibration & Performance Shoulders (below relates to scalable measures)

When incorporating new metrics into incentive plans that are still in early stages or have limited history of performance, wider performance shoulders can help mitigate unpredictability of actual results. Alternatively, a step or flat zone approach can be taken (outlined below) which may address unpredictability and offer a “safer” landing zone near desired target performance. Under a traditional curve, each incremental unit of performance produces a uniform increase in payout. Many metrics that relate to ESG do not lend themselves to a linear curve (shown below).

In all cases, the Board should retain discretion over the plan to ensure the ability to modify awards.

Considerations

- May be applicable for qualitative measures

- Careful thought placed on applicable scores (i.e., required milestone achievements for each level of payout)

- A caution with this approach is that any slight miss may result in a substantially lower payout

Example: Reportable Injuries

Considerations

- Suitable for quantitative or scalable measures

- The flat zone alleviates pressure in having a “perfect” calibration, where slight misses may trump the overall payout

- Setting the flat zone requires judgement and will be based on specific circumstances (i.e., a wider zone will be less punitive for performance below target, but will also reduce the upside potential)

- Incremental performance in the flat zone would not produce incremental increases in reward

Example: GHG Emission Intensity

Summary

Incorporating ESG metrics in compensation is similar to traditional metrics and has some unique considerations given the dimension of time, scalability, and maturity of measurement. The longer-term nature of many ESG goals presents challenges in setting targets which can be mitigated through the use of interim targets, ensuring these targets remain focused on the long-term goal and transparent for stakeholders to understand the pathway to long-term goals. Consistently monitoring achievement of results and maintaining flexibility to evolve the set targets will be helpful in achieving well defined incentive plan targets.