Every year, Hugessen Consulting conducts a review of the proxy circulars filed by the constituents of the S&P / TSX60 Index to report on trends in executive compensation and related governance practices among Canada’s largest and most influential companies. This article is the first in a three-part series summarizing our findings related to environmental, social, and governance (“ESG”) metrics in executive compensation programs among these companies.

Part 1 of our series will focus on the prevalence of ESG metrics being incorporated into incentive plans. Part 2 will provide a deeper dive on how ESG metrics are incorporated into incentive programs (i.e., short term versus long term plans, weighted measure versus modifier). Part 3 will address the types of ESG metrics being used and measured.

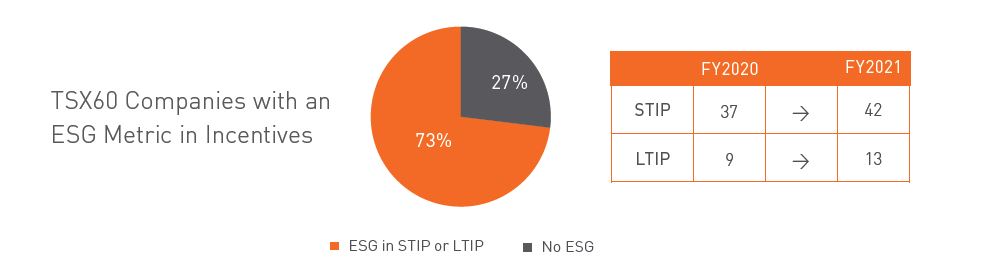

How many TSX60 companies incorporate ESG metrics in their incentive plans?

The prevalence of including ESG metrics in incentive plans has gained momentum over the past 5 years, with a notable increase throughout 2020 and 2021 as many companies became more thoughtful about their role in society and duties to all stakeholders. This remains true for the 2022 proxy season: our key takeaway is that there has been continued momentum and an intensification of the ESG-related compensation trends we saw in 2020 and 2021.

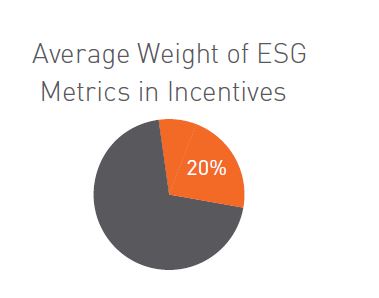

As of the 2022 proxy season, 75% of TSX60 companies have formally incorporated ESG into their compensation plans in some capacity, or have disclosed their intention to do so in 2022. Several companies also increased the relative weight of ESG metrics within their incentive plans year-over-year (17%). For the companies that have defined the weight of ESG metrics within their STIP or LTIP programs, these metrics are weighted at approximately 20%, on average, which is similar to the past few years1.

Of the 16 (27%) TSX60 companies that have not yet incorporated ESG into their incentive plans in any capacity, most appear to be in the relatively earlier stages of developing their broader ESG strategies; as such, it is likely premature in those instances to incorporate ESG into their incentive programs.

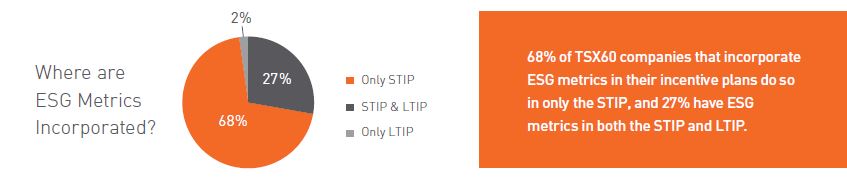

ESG in Incentive Plans: STIP vs. LTIP?

Short term incentive plans (“STIPs”) remain the most common incentive instrument used among the 73% of TSX60 companies that incorporate ESG metrics in executive compensation programs, typically as an element within the balanced scorecard. By doing so, ESG metrics are included among the other important financial and operational metrics used to evaluate performance in a given year, while also maintaining flexibility to adjust the metrics and measurement approaches year-over-year.

A significant minority of TSX60 companies also incorporate ESG metrics into their long term incentive plans (“LTIPs”). This is most often accomplished through the use of performance share units, or PSUs2. An alternative approach is to use front-end performance conditioning, where performance metrics determine the number of units provided to participants at the date of grant (as opposed to at the end of the vesting period, as with PSUs). Given the longer-term nature of many ESG objectives, the LTIP can be seen as a natural mechanism for linking ESG to compensation – though, the design of these instruments does not allow for as much flexibility to change the measurement approach as the STIP would (e.g., once a PSU is issued, there is limited ability to adjust the performance measures within its 3-year term).

Looking Forward

Companies and Boards are continuing to build their competence and comfort level with understanding the material ESG metrics for their organizations, and the complexities and tradeoffs that come with incorporating these metrics into incentive plans. Looking forward, we expect the momentum seen this proxy season to continue, with companies continuing to incorporate ESG metrics more frequently in their incentive plans.

1 Methodology is based on weighting as a % of STIP or LTIP (i.e., both corporate and individual components), for only those companies that include ESG metrics in their plans.

2 PSUs function like restricted share units (“RSUs”), where a participant receives a notional share. At the end of a performance period (typically 3 years), the number of units awarded is modified based on the achievement of pre-determined performance criteria.