Introduction

Entering 2024, company directors maintain an optimistic outlook for the upcoming fiscal year. Despite continuing challenges related to talent management and succession planning, companies are remaining agile and continue to adapt to the evolving business landscape. While inflationary concerns and fears of recession have diminished relative to last year, directors and organizations continue see new disruptions, notably the emergence of artificial intelligence technologies. The 2023 edition of our Director Pulse Survey captures prevailing sentiment on corporate performance, board priorities, expected 2023 incentive payouts and action, ESG in compensation, human capital challenges, and board effectiveness. These findings build on Hugessen’s Pulse Survey conducted last year. It is evident that the complexity of the issues faced by boards continues to increase, requiring an awareness of business trends, nuanced understanding on how they intersect, and proactive engagement with traditional and emerging governance issues. Overall, this report draws together a moderately positive outlook, and boards appear ready to respond to the challenges arising in the new fiscal year.

Methodology

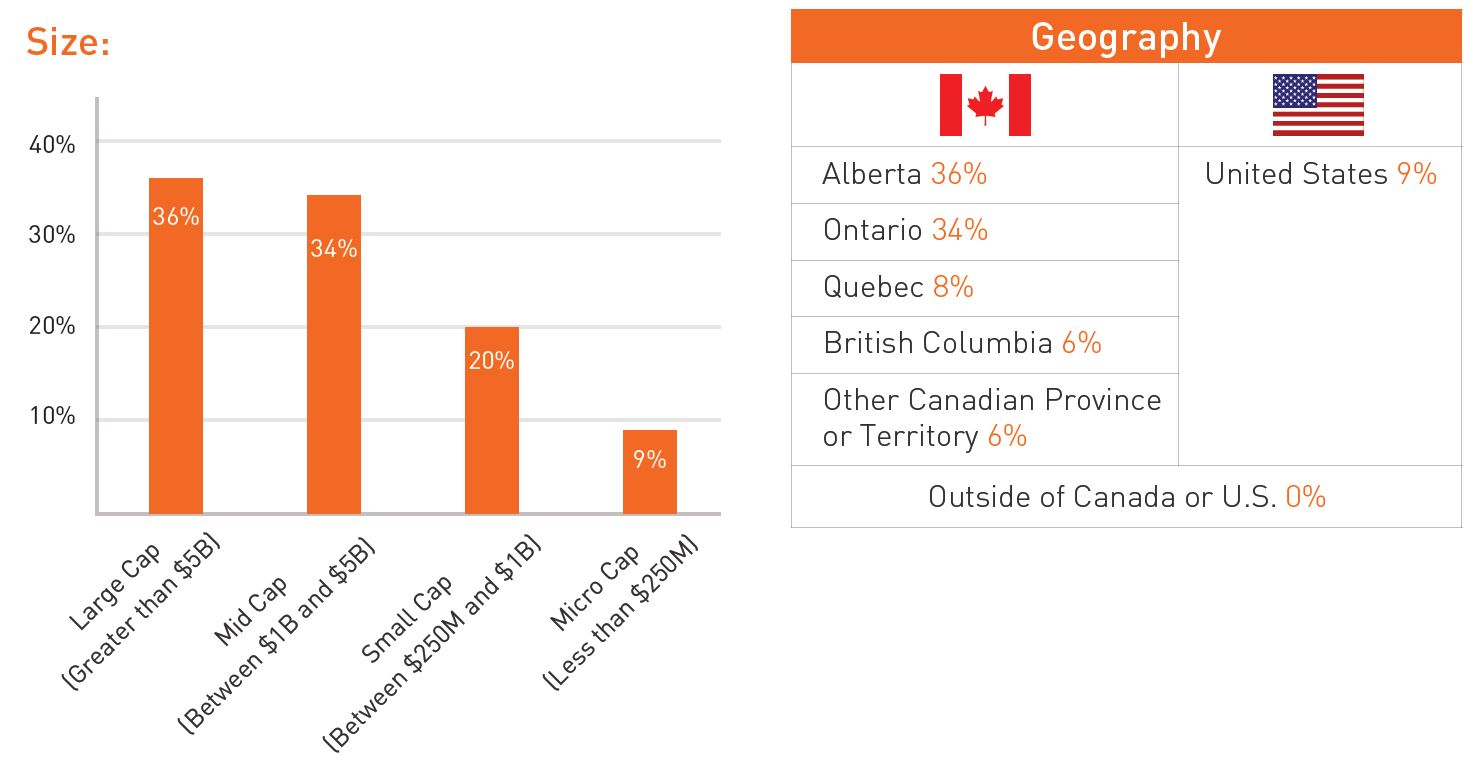

This briefing summarizes the responses of 64 director participants collected in the final two weeks of November 2023, representing directors who serve on a wide range of for-profit Canadian company boards from an ownership, industry, geography, and company size perspective. We note summary statistics may not add to 100% due to rounding.

Key Takeaways

- Financial performance expectations / estimates for 2023 were generally at or above target (75% of respondents), translating to expected incentive payouts being at or above target as well (70% of respondents)

- The application of discretion for short-term incentives remained stable year-over-year at ≈30% of respondents expecting to use discretion (75% of which is upward discretion)

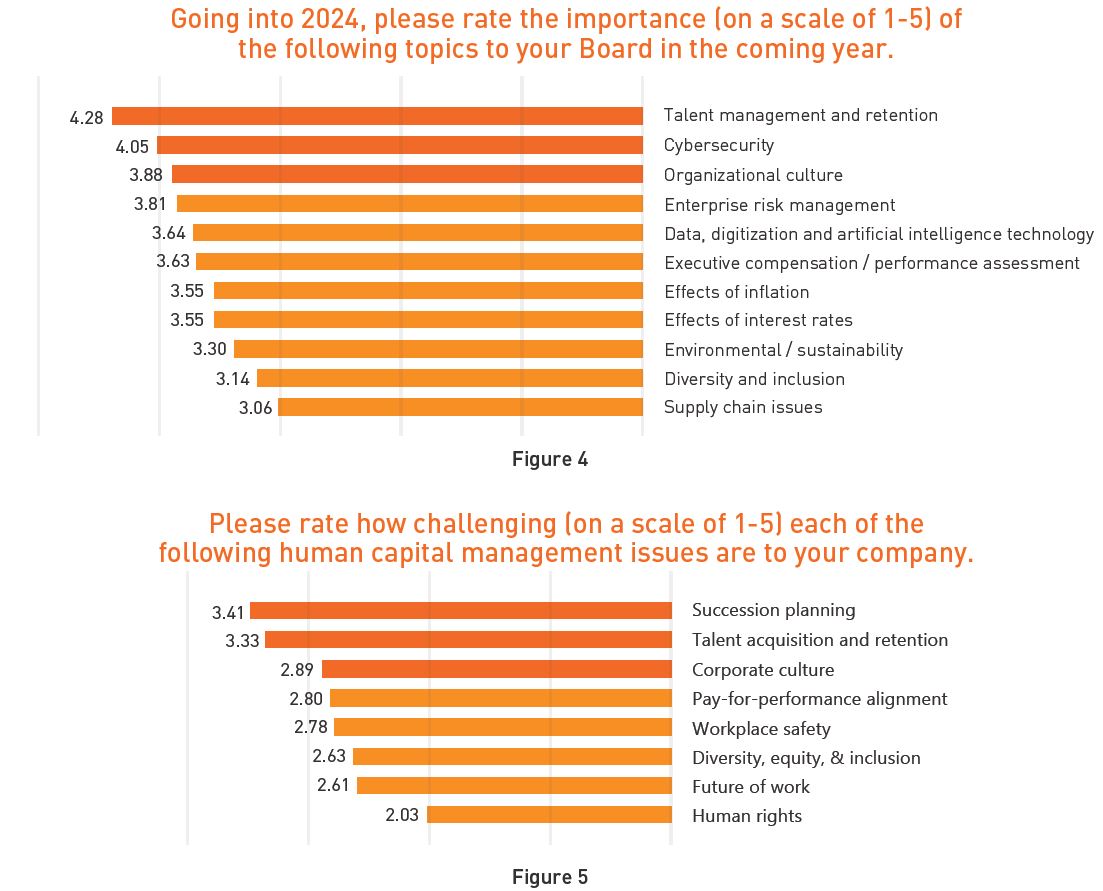

- Consistent with last year’s survey, directors identified talent management and retention as the highest Board priority going into 2024, while addressing the effects of inflation decreased from 2nd to 7th place

- Succession planning overtook talent acquisition and retention as the most challenging human capital management issue facing organizations

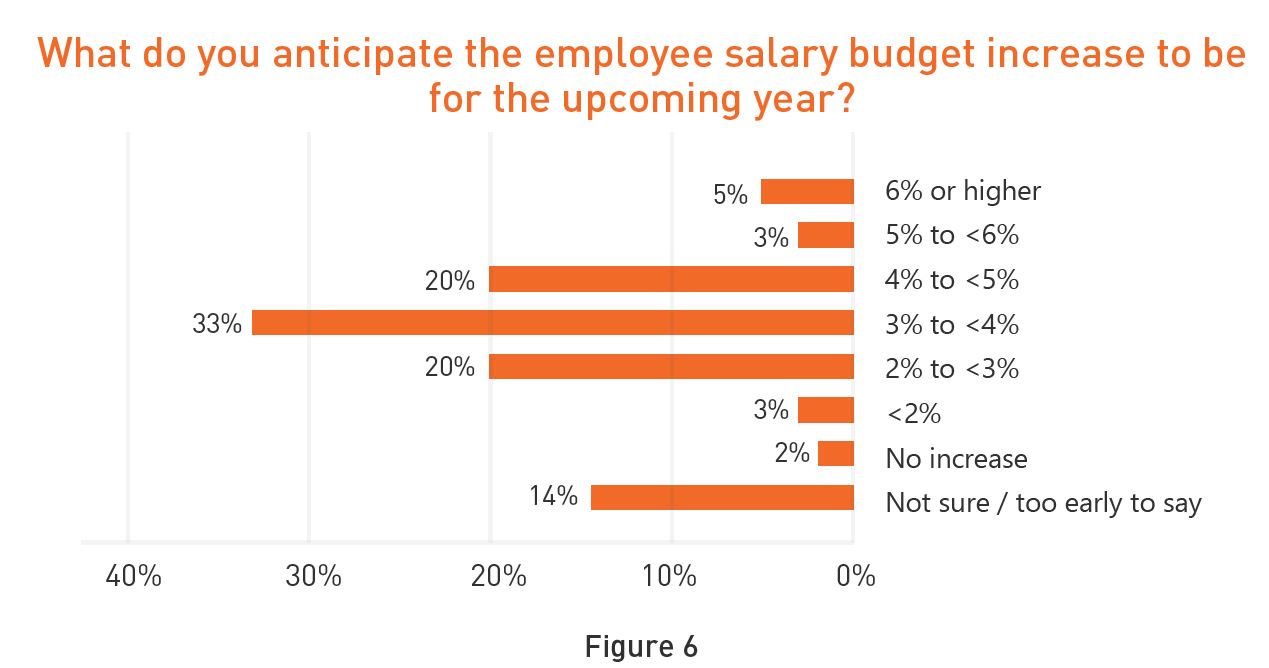

- Employee salary budgets have been generally stable year-over-year, with 73% of respondents expecting a budget between 2% and 5%. Only 2% of respondents are expecting no increase, which is down from 11% in last year’s survey

- Most respondents (84%) have some / moderate understanding of artificial technologies and their potential implications on their organizations, but few (2%) have a very high understanding

- Changes to LTIP design remain moderated, with 30% of respondents at companies granting stock options expecting to make an adjustment to their weighting in the LTIP mix (6% of which are removing stock options altogether); meanwhile, 25% of respondents at companies granting performance share units (PSUs) are modifying their metrics

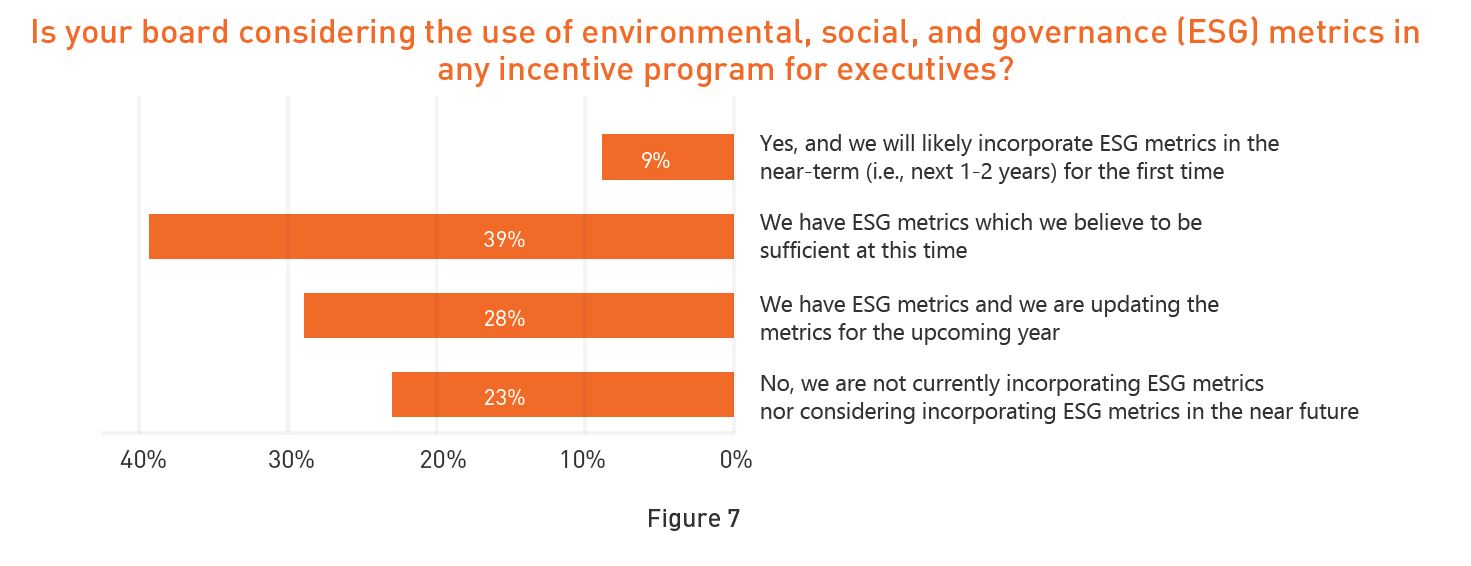

- The pace of ESG metrics adoption continues to slow, reflecting the swift proliferation of these metrics in executive compensation plans over recent years (9% of respondents expect to add ESG metrics for the first time, while 67% already have ESG metrics); ESG metrics continue to primarily be within short-term incentive programs rather than in long-term incentive programs

2023 Performance & Incentive Discretion

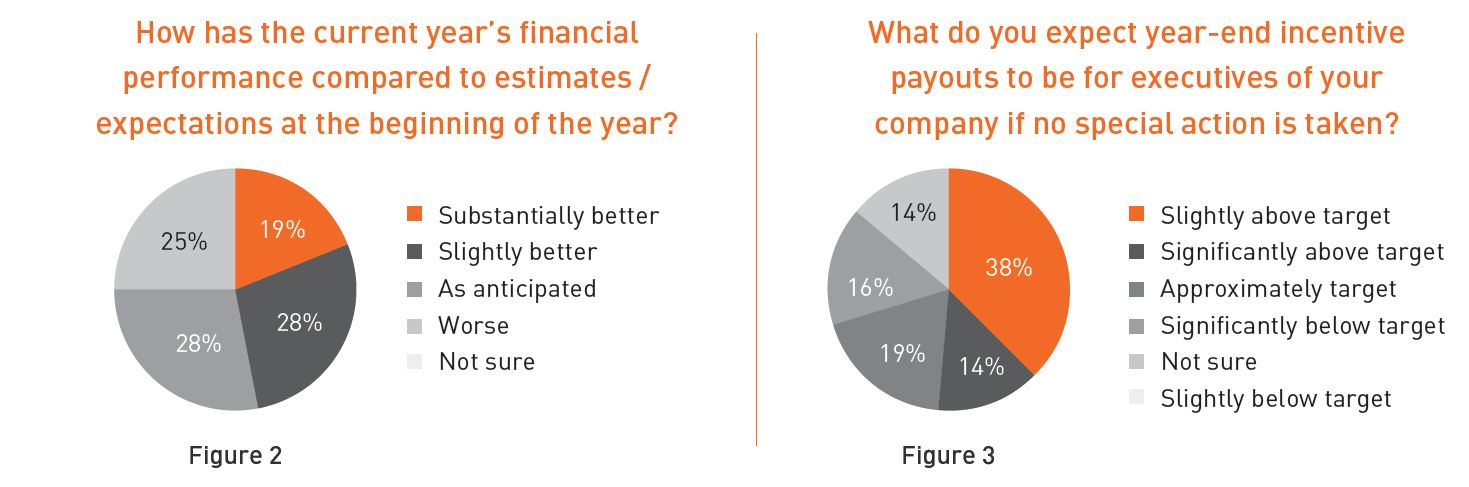

Overall sentiment regarding 2023 corporate performance is generally positive (Figure 2), although we note fewer respondents expecting ‘substantially better’ financial performance (19% in 2023 vs 30% in 2022). Accordingly, incentive payouts are expected to be at or above target (Figure 3), despite observing a slight increase in the number of observations of below target payouts YoY (30% in 2023 vs. 23% in 2022). Energy companies fared particularly well, with 82% expecting target or positive financial performance, translating to generally above target payouts (65% of energy respondents).

The anticipated need for discretionary STIP adjustments remained consistent with recent years at approximately 30%. For those organizations applying discretion, such discretion is expected to be modestly positive (75%). As noted in last year’s survey, we suspect that a combination of generally stable economic performance over the past few years (relative to the “shock and boom” of the COVID-19 pandemic), combined with more “flexible” incentive framework structures (e.g., wider performance ranges), have enabled performance assessment structures to operate as intended, reducing the need for year-end discretion.

Top Board Priorities for 2024

Consistent with last year’s survey, directors have identified talent management and retention as the top board priority, followed by cybersecurity and organizational culture (Figure 4). Interestingly, addressing the effects of inflation has fallen from the 2nd highest ranked priority to the 7th ranked priority, reflecting the stabilization and reduction of inflation rates over the past 12 months. Directors also identified regulatory and government actions / compliance as being top of mind going into 2024.

Succession planning was noted as the most difficult human capital challenge facing Boards, followed by talent acquisition & retention and corporate culture (Figure 5). This result is understandable, as 2023 saw record CEO departures in the U.S.[1]. Significant shareholder and media attention on numerous CEO successions has highlighted the importance and challenges in getting the CEO succession process right.

Salary Budgets & One-time Awards

Employee salary budgets expectations are stable year-over-year, with 73% of respondents expecting a budget increase between 2% and 5% (Figure 6). We do note, however, that more respondents (33%) expect a budget of between 3% and 4% than last year (23%). We also observed fewer instances (2%) of no increase relative to last year (11%), likely reflecting continued easing from COVID-19 related freezes.

Roughly 40% of respondents granted one-time awards in 2023, evenly split between retention-based awards and on-hire awards. While the frequency of one-time awards has remained stable year-over-year, we observe fewer retention awards than last year (16% this year vs. 21% last year). This suggests that as the labour market has softened, organizations may be feeling less pressure to provide supplemental awards beyond the incentive program and / or any past (or expected) pay increases are viewed as sufficient to retain employees. The reduction of these types of one-time awards may be viewed positively by shareholders and proxy advisors, who are generally wary of such awards as it may signal an ineffective compensation framework.

Environmental Social & Governance (“ESG”) in Compensation

The number of respondents who have ESG metrics in incentive plans or are planning to add them in the near-term is stable year-over-year at 76% (Figure 7), while the rate of adoption is slowing (9% of respondents expect to implement ESG metrics in the next 1-2 years, down from 20% last year). As ESG metrics have been added to most organizations’ incentive plans, the rate of new adoption will inevitably slow, with some minority of organizations continuing to choose not to adopt them (23% of respondents do not have ESG metrics nor are considering their adoption, stable year-over-year). Consistent with last year, the vast majority of ESG metrics reside in the STIP, suggesting that while ESG metrics have undergone wide adoption, companies are still cautious of setting and/or calibrating longer-term ESG objectives. This notion is reinforced by the fact that 63% of respondents report having no plans to implement ESG metrics in their LTIP plans in the near future. Of respondent companies with ESG metrics, the most common metrics remain climate/environment and human capital (82% and 73%, respectively).

Board Effectiveness

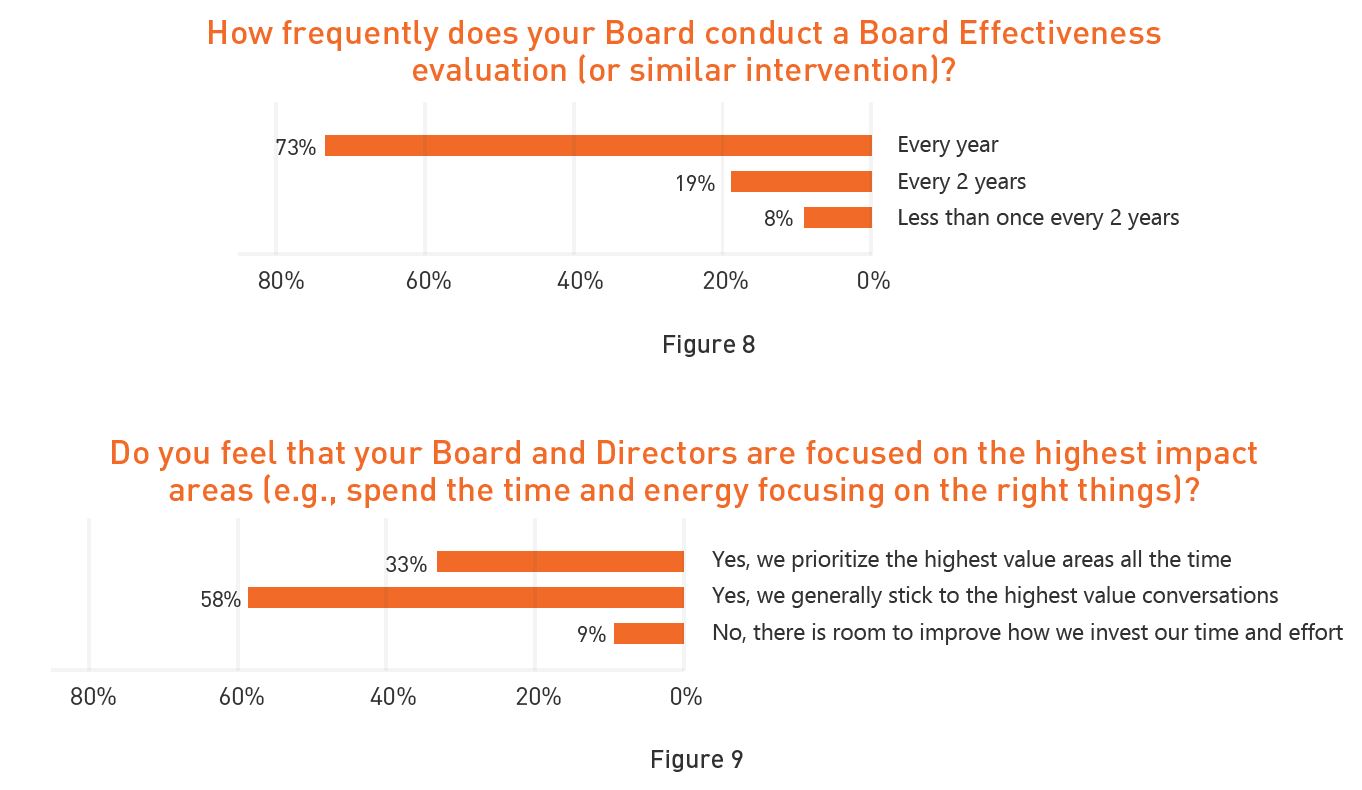

Directors continue to see board evaluations as a useful tool, as 73% of respondents reported using an annual board evaluation, or similar intervention, on the boards they serve (Figure 8). Among survey respondents, only 33% believe their Boards prioritize the highest value areas all the time, indicating opportunities to refine Board processes and stay agile on evolving priorities to drive greater value for the organization (Figure 9). Nonetheless, most (58%) believe that their Boards are generally sticking to the highest priority areas.

Conclusion:

The 2023 edition of our Director Pulse survey indicates a continued positive outlook as challenges such as elevated inflation rates begin to subside. Talent management remains a top concern for Boards even as the we observe a softening of the labour market in the U.S. and Canada. As Boards grapple with continuing challenges, emerging trends, such as the proliferation of AI, will necessitate nuanced understanding and prudent actions from directors. ESG metrics in incentive structures have maintained their momentum, with similar usage and adoption rates as in prior years, demonstrating a commitment by Canadian Boards in these areas. As Boards look to 2024, it will be important to ensure attention is focused on the issues that matter most to their organization, and that they continue to effectively navigate the numerous challenges facing them. While several challenges have subsided, new challenges are emerging, further increasing the importance of directors “leaning in” to add value to their organizations.

[1] https://www.challengergray.com/blog/november-2023-ceo-exits-highest-on-record-the-penultimate-month-of-2023-sees-most-ceo-exits-since-the-summer/