Introduction

Privately-owned companies enjoy many advantages compared to their publicly traded counterparts in the current economic and regulatory environment. Their detachment from the public markets allows them to operate under less scrutiny and governance bureaucracy. Furthermore, the taxation of stock options for individuals at Canadian controlled private companies (“CCPCs”) remains favorable compared to other LTIP instruments. That said, the degree of benefit has been dampened in some cases due to recent changes to the capital gains inclusion rate effective June 25, 2024. Larger non-CCPCs with annual gross revenues over $500M have also been affected by these changes, compounding the modifications to Canadian stock option taxation implemented on July 1, 2021.

The absence of a public market, and the easily accessible company valuation that comes with it, can make it more difficult, however, for privately-owned companies to structure, administer, adjudicate, and effectively communicate equity compensation to participants. That said, publicly traded companies continue to deliver a large portion of total compensation in the form of long-term equity-based awards setting the competitive standard.

We have collaborated with Mintz LLP to provide an update to our previously published article Long-Term Incentive Alternatives at Private Companies: A Brief Overview, expanding on key considerations for Canadian private companies when considering long-term incentive plan (“LTIP”) design and implementation. Selecting appropriate instruments will require careful consideration of several factors, including company valuation and liquidity – these factors are discussed later in this article.

Many Canadian public and privately-owned companies have operations, employees, directors and other service providers in the United States (and vice versa) and more often than not, these companies want to offer equivalent LTIP entitlements both north and south of the border. Consequently, we see many of the same LTIP vehicles described below being implemented via cross-border LTIPs. Critically, companies must ensure that the design of their cross-border LTIPs comply with applicable laws in both Canada and the United States, including tax, employment and securities laws, so to avoid any unintended outcomes and potentially costly lawsuits and liability. Hugessen and Mintz have expertise that can assist you in designing and implementing your cross-border LTIPs.

LTIP Objectives

The overall objectives of the long-term incentive plan will influence which design features are most relevant. For example, private companies have several alternatives for LTIPs that can mimic share-based compensation and allow participants to share in the longer-term growth in company value that is enjoyed by shareholders in cases where real equity ownership is not desired.

Common objectives include:

Attraction of Talent: attracting the right employees and other service providers, companies will want to consider what is competitive in their industry — considering both publicly-traded and private company incentive structures

Incentivization of Performance: striking a balance between reflecting key measures of company success, while incorporating what participants have ‘line-of-sight’ to influence. For many organizations, LTIPs can effectively support the objective of coalescing management teams around one or more common goals

Alignment with Shareholders: ensuring participants have sufficient “skin-in-the-game” and reinforce a culture of ownership and sharing in the company's long-term value growth

Retention of Key Personnel: ensuring sufficient retention mechanisms are in place (e.g., through deferral of compensation and vesting / forfeiture conditions)

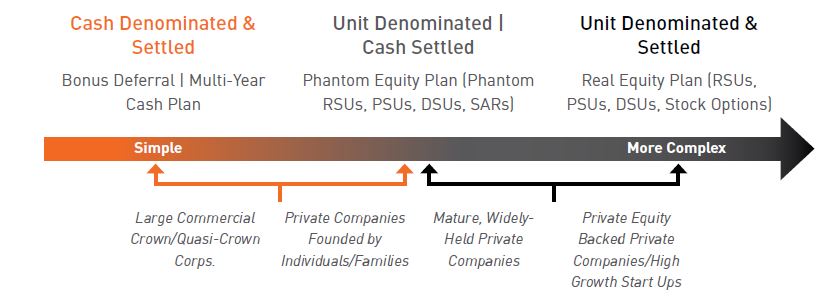

Spectrum of LTIP Vehicles

LTIP Vehicles: What is it and when to use it?

Annual Bonus Deferral

What is it?

A portion of a participant’s annual cash incentive award is deferred for a multi-year period (e.g., 3 years).

When to use it?

Seeking the simplest mechanism to incorporate a retention element into the incentive framework. No desire to incorporate forward-looking performance conditions or tie the award to the value (or theoretical value) of the company.

Multi-Year Cash Plan

What is it?

A target award is granted to a participant and is subject to a multi-year performance modifier based on predetermined performance criteria.

When to use it?

Desire to link payouts to the achievement of key long-term performance objectives.

Restricted Share Units (“RSUs”)

What is it?

RSUs are units that track the value of the underlying shares or notional value of the company (e.g., based on an EBITDA multiple) and vest based purely on the passage of time. At the end of the vesting period, the recipient receives the underlying number of shares (real equity) or a cash payment of equivalent size to the notional full share value at the time of settlement (phantom equity). The RSU award size can be informed by annual performance (similar to an annual bonus deferral, but into RSUs) or other desirable criteria.

When to use it?

Desire to align recipients with shareholders and provide reward for increasing longer-term company value. Retention incentive that generally retains its value over the vesting period.

Performance Share Units (“PSUs”)

What is it?

Similar to RSUs, but the number of units that vest is subject to the achievement of forward-looking performance conditions. This instrument provides the recipient with additional ‘leverage’ by allowing for more (or fewer) units to vest depending on the actual level of performance achieved relative to the pre-determined criteria.

When to use it?

Desire to link payouts to company value as well as the achievement of key long-term performance objectives.

Deferred Share Units (“DSUs”)

What is it?

Similar to RSUs, but are paid out only upon departure from the company subject to the achievement of any applicable vesting criteria.

When to use it?

Best if used in a focused manner, such as a long-term ownership vehicle for top executives or board directors.

Stock Options and Stock Appreciation Rights (“SARs”)

What is it?

Right to buy a share once vested at a pre-determined price (strike price) and derives value only from an increase in share price (above the strike price) from the date of grant. Either settled in real equity (stock options) or in cash (SARs).

When to use it?

Desire to provide additional upside ‘leverage’ (with potential preferred individual tax treatment).

LTIP Vehicles: Types of private companies that use them?

Large Commercial Crown / Quasi-Crown Corps: almost always use cash denominated and settled plans, as real or phantom equity is not available or appropriate. Multi-Year Cash Plans are most commonly used.

Private Companies Closely Held by Individuals / Families: typically use cash-settled plans as shareholders are usually not inclined to share real equity. Multi-Year Cash Plans or Phantom Equity Plans are most commonly used.

Mature, Widely Held Private Companies: often provide real equity or at least track company value for phantom equity purposes as in RSUs. These companies often have many shareholders, most of which tend to be employees or partners in the organization. Real or Phantom Equity Plans are most commonly used.

Start-Ups & Private Equity Backed Private Companies: typically provide real equity through the granting of “founder shares” or other more leveraged instruments. Real Equity Plans are most commonly used, especially stock options, sometimes with performance hurdles.

Key Considerations for LTIP Awards

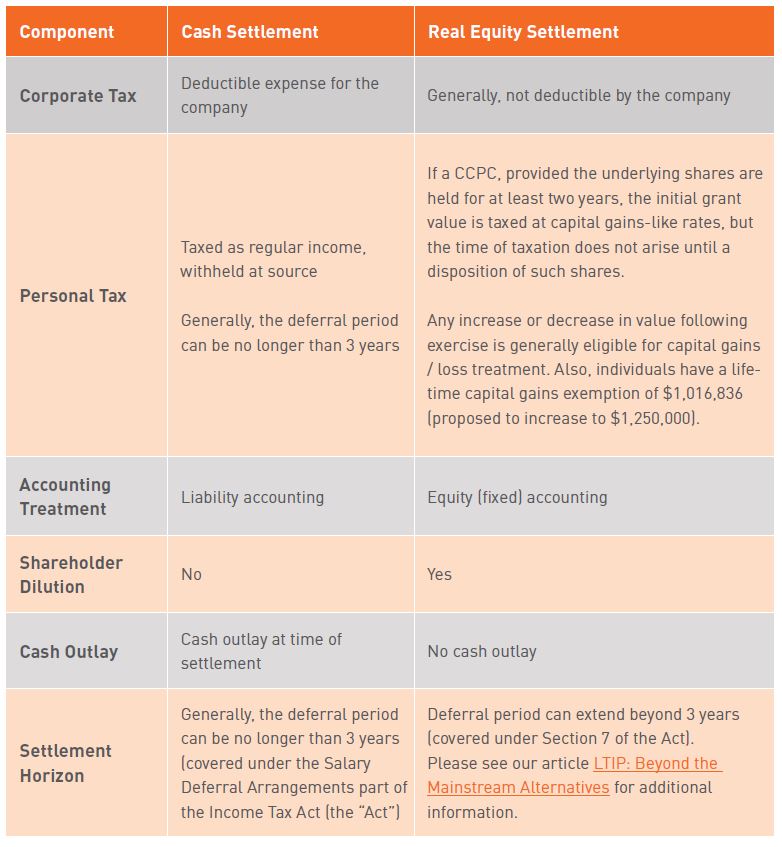

Like publicly traded organizations, private companies will need to weigh the pros and cons of settling equity awards in either cash or real equity (or a combination thereof). One major factor is the favourable personal tax treatment for CCPCs, which offers added tax benefits when using real equity. These structures grant stock options with a nominal exercise price, effectively delivering the value of a full share, while receiving preferential capital-gains-like tax treatment.

Company Valuation

Determining a share price to unitize value is often a challenging aspect of developing a private company LTIP. The key objectives should be to develop an easily administered, defensible and consistent approach which accurately measures the change in company value over time. There are two primary valuation methodologies a company can use:

Third-Party Valuation: A third-party valuation often provides the most accurate appraisal of the company, at the expense of line-of-sight to value drivers and cost. This method is also readily accepted by the Canada Revenue Agency if questioned.

Formulaic Valuation: A simple fixed financial metric multiple (e.g., EBITDA) offers clear line-of-sight to value drivers and is cheaper to implement, but may be more difficult to apply and defend to the Canadian Revenue Agency over time as the business evolves.

Tax Considerations. For CCPC stock options, the fair market value of the shares issued at exercise determines the tax payable later on a future sale. To determine if a non-CCPC stock option is eligible for capital gains like rates, the strike price must be set to be at least equal to fair market value at the date of grant.

Corporate Governance Considerations. Regardless of which valuation methodology the company uses, the board of directors of the company should ultimately approve whichever share price is chosen, whether by way of a board meeting or a written resolution. If the company is attempting to set the share price at fair market value in order to, for example, grant eligible optionees capital gains like rates on their taxable employment income inclusion from the options (as mentioned above), the board should be extra careful to ensure that the valuation is, indeed, defensible. Directors generally owe a duty of care to the corporation and must exercise the care, diligence and skill that a reasonably prudent person would exercise in comparable circumstances, or they may otherwise expose themselves to potential liability.

Share Liquidity

With no public marketplace to facilitate the purchase and sale of shares, private companies are typically responsible for providing liquidity to plan participants. Liquidity requirements can be managed through careful planning and budgeting, scenario-testing, and the implementation of certain “safeguards” (e.g., cap on trading to ensure fundability, prohibiting trading between employees, limiting liquidity commitment under extraordinary circumstances, etc.).

Employment Agreements, Shareholders Agreements and Equity Plans

In addition to the considerations above, when designing and drafting LTIPs companies must be mindful of other applicable laws (e.g., employment and securities laws), ensure that their LTIPs are drafted clearly and provide adequate protections and administrative flexibility (e.g., permit appropriate capital adjustments) and, if of interest, ensure that their LTIPs do not discourage potential buyers (e.g., include off-market change of control and vesting provisions).

Termination provisions in an LTIP are an essential component aimed to provide certainty with respect to vesting and participation (including post-service exercise or settlement periods) at the end of a participant’s tenure with the company. It is critical, particularly for employees, that the termination provisions be drafted clearly and meet the minimum requirements of applicable employment standards legislation to avoid unintended and often costly consequences, such as continued vesting and participation during an employee’s common law reasonable notice period (which can be as much as 24 months or more following the last day of employment). It is also imperative that companies review these provisions periodically and update them to reflect the current state of the law, which remains fluid throughout Canada.

Not only should the plan itself include clear language, but so should the accompanying award agreements, enrollment forms and any other participant communications (including employment, agreements), which should be drafted consistently with plan terms and, where appropriate, expressly reference the termination and other material provisions of the plan in order to enhance the probability that they will be enforced as intended.

LTIPs should also include a number of boiler-plate provisions aimed to protect the company covering subjects such as restrictive covenants (e.g., confidentiality, intellectual property, non-solicitation, and to the extent appropriate, non-competition), privacy, and voluntary participation.

Further, if an award recipient pursuant to an LTIP will, at some point, become a shareholder of the company, the company should ensure that the LTIP contemplates the standard protections against shareholders disputes as well. Generally, if the company already has a shareholders’ agreement in place, the LTIP can simply provide that any award recipient must enter into the company’s shareholders agreement prior to the receipt of any shares. However, if a company does not have a shareholders’ agreement in place, then it is recommended that the company include their desired shareholder protections directly in the LTIP. These can include, but are not limited to, provisions related to the restrictions on transfer, right of first refusal, drag-along, lock-up, voting restrictions and repurchase of an award recipient’s shares (once issued to them pursuant to the LTIP).

Concluding Thoughts

As evidenced by the high usage levels among both publicly traded and private companies, LTIPs are viewed as effective tools to incentivize employees and other service providers to focus on goals that extend beyond the short-term, and participate in long-term growth in company value. Two final thoughts:

- When considering adopting an LTIP at a private company, it will be important to weigh the tax and alignment benefits against the practical and legal complexities and risks of implementing such a framework.

- There is significant flexibility afforded to private companies when designing an LTIP – gaining an understanding all of the alternatives available, and their associated benefits and drawback, is a critical first step.