The changes to stock option taxation mark an opportune time for companies to reassess and, if necessary, revise their long-term incentive plan (LTIP) strategy and design. In March, Hugessen provided an overview of the tax changes – please see Part One for a detailed overview of the upcoming changes. This was followed by a briefing outlining approaches to reassessing long-term incentive design – please see Part Two of our series. This “Part Three” briefing looks beyond the mainstream LTIP alternatives and focuses on real long-term equity and ownership approaches. Much of the material in this briefing was covered in a paper produced for a conference hosted by Caisse de dépôt et placement du Québec in October 2015 – please see Rethinking Long Term Incentives and Ownership Guidelines.

Beyond the Mainstream LTIP Alternatives

In general, long-term incentives are used by companies to motivate and reward management to achieve mid- and long-term performance for investors. The most common LTIP instruments include stock options, restricted share units (RSU), and performance share units (PSU).

Globally, the use of stock options has decreased significantly over the last 20 years. The first shift away from stock options happened post-Enron and the bursting of the dot-com bubble, leading to a remix or balanced approach of stock options, share units (PSUs and/or RSUs), and share ownership requirements. The second major shift happened post-2008 financial crisis which led to greater regulatory and shareholder pressures. These included, among other things, say-on-pay, increased disclosure requirements on risk, and a more assertive shareholder community. The result was a further increase in the pressure to reduce, if not eliminate, the use of stock options. Throughout this period, stock option usage has declined in Canada, albeit at a slower rate than in the United States. We expect the change in taxation of stock options in Canada to be the next inflection point.

As stock options decrease in either prevalence or in proportion of the LTIP mix, 3-year share units (RSUs and PSUs) have increasingly become the go-to alternative. Provided that at least half of the LTIP is composed of PSUs, companies can find themselves in a safe position vis-à-vis proxy advisors and institutional shareholder say-on-pay votes. However, these mostly cash settled vehicles lack both the long-term and/or ownership characteristics that may be desired. With pressures to ensure risk alignment, long-termism, and sustainability in compensation programs, looking beyond the mainstream alternatives to longer-term equity should be considered as part of the redesign process. To this end, this briefing examines three approaches:

- Long-Term Share Units

- Total Return Rights (i.e., stock options with dividend equivalents)

- Long-Term After-Tax Shares

This briefing also discusses share ownership requirements in the context of the shifting LTIP landscape.

1. Long-Term Share Units

It is often said that share unit deferrals cannot be longer than 3 years. It is true that certain types of cash-settled share unit structures do have such limits. However, if structured properly, long-term incentives can go beyond 3 years. In most cases, this requires use of treasury settled awards, thereby moving from the Salary Deferral Arrangements part of the Income Tax Act to Section 7 of the Act that deals with stock options and treasury settled compensation.

These long-term share units can be structured as long-term RSUs or PSUs with either fixed or flexible settlement dates.

The images below illustrate a fixed versus flexible settlement. Both settlement approaches provide additional retention extending past the typical 3-year window for cash-settled LTIP. The flexible settlement approach allows the recipient to retain their ownership for as long as desired providing additional benefit to the recipient through potential share appreciation and/or dividend accruals and additional benefit to the company through risk alignment and long-termism.

Important Note: The approaches provided in this section have a number of tax, accounting, and security issues. For more detailed information on many of these approaches please refer to the CPA document Equity-Based Alternatives to Stock Options. Ultimately, it is important that tax, accounting, and legal advice specific to each issuer’s situation be fully understood.

The Fixed Settlement example has half of the units settling at the end of year 5 and half at the end year 7.

In the Flexible Settlement example, the share units continue beyond five years and there is a redemption feature whereby the employee can request to have the treasury shares issued. This flexibility is akin to a stock option exercisable period between vesting and expiry.

In both examples, awards are fully vested as of the 3rd anniversary of the date of grant.

There are several ways to overlay performance on such awards, including:

- Sizing the initial award based on performance

- Using the typical three-year PSU performance period (e.g., adjust the number of units after three years, with the term of the awards extending thereafter)

- Using longer term performance measures and standards, in line with the term of the awards

Finally, it is possible to incorporate a cash settlement alternative. To stay within Section 7 of the Income Tax Act, the participant would need to maintain the right to receive settlement in treasury shares, but can be given a cash settlement alternative. This is akin to stock options with a tandem cash SAR. One of the reasons companies may want to include a cash settlement alternative is to gain access to a corresponding corporate tax deduction (RSUs and PSUs that settle in treasury settled shares do not result in a corporate tax deduction in Canada).

2. Total Return Rights

Many dividend paying Canadian companies offer stock options as part of their LTIP mix. Stock options by nature are leveraged vehicles. The leverage increases as the value of the underlying options decrease, as more options need to be granted to provide the same grant date compensation value. For issuers with high dividend yields, the stock option leverage can be very significant (due to the typical option valuation mechanisms such as Black Scholes or Binomial models). In these circumstances, this leverage is often managed by limiting the overall weight of stock options within the LTIP, and by ensuring the option values used to calibrate the grants are not too low. Another approach could be to consider including dividends in the appreciation structure (e.g., Total Return Rights) – whereby the payout would effectively equal the total return on a starting share price (and not just the share price appreciation, as is the case in typical stock options).

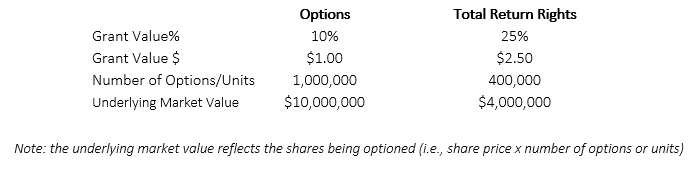

The table below shows how such an approach would shift the grant size. The primary assumptions are a 4% dividend yield, a $10 starting price, and a $1 million grant date compensation value. Using option pricing models (e.g., Black-Scholes, Binomial) we arrive at an option value of about 10% of the grant price for the options and 25% of the grant price for the Total Return rights. The higher the option grant value, the fewer the number of options or rights need to be granted to achieve the grant date compensation value, thus reducing the leverage embedded in the award.

In this example, the lower option value generates a very large grant, with $1 million of compensation resulting in 1 million options being granted - said another way, options on $10 million of share value. This means, for each 10% increase in the share price, the options become $1 million more in-the-money. Conversely, the Total Return Rights are less leveraged and would require a 25% total shareholder return (share price and dividend return) to achieve the same incremental $1 million in-the-money value.

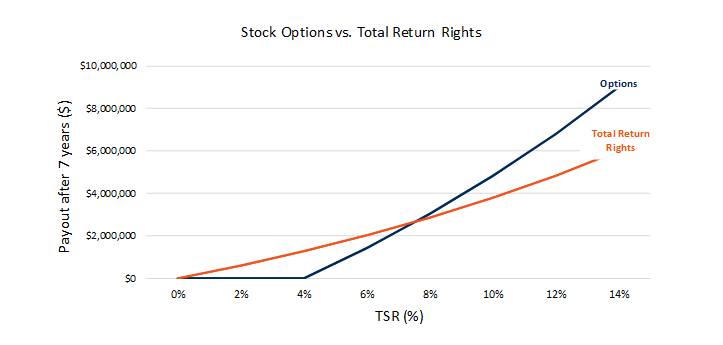

In the end, Boards should be comfortable that the risk/return characteristics of the long-term incentive plans support the risk/return characteristics for investors and key stakeholders. Stock options may have an appropriate place in the LTIP mix, but in some situations Total Return rights may provide a more suitable alternative.

The chart below shows the payout curve of Stock Options vs. Total Return Rights under several 7-year annual TSR scenarios using the assumptions provided above:

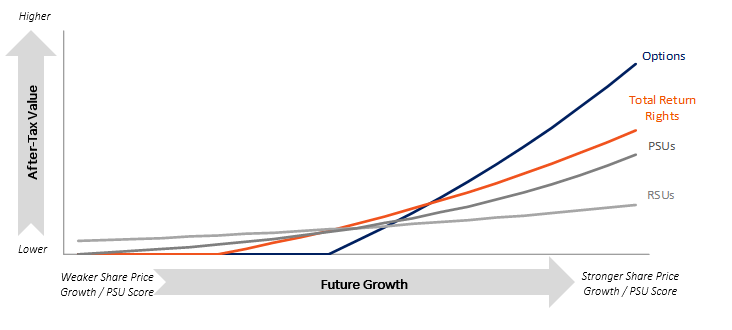

Sensitivity Analysis: Options versus 7-year RSUs, PSUs and Total Return Units

The chart below shows the payout curve of several equity instruments. It is important to consider the leverage required and fit of each instrument for your organization.

Generally speaking, instruments with the least amount of leverage (e.g. RSUs) perform best relative to high leveraged instruments under low growth scenarios. Conversely, more highly leveraged instruments (e.g. PSUs and stock options) perform best under high growth scenarios. It is useful to understand how the pay-for-performance leverage operates for each instrument and how they operate when combined in an LTI program. Dependent on the characteristics of the business in question, one or multiple instruments can be used to maximize the usefulness of the compensation program.

3. Long-Term After-Tax Shares

Under conventional LTIP designs, pre-tax share units are granted through the LTIP, whereby recipients are not required to pay taxes until the shares have vested (i.e., after 3 years for typical RSUs and PSUs). This is commonly viewed as a favourable approach as the recipient can take advantage of shareholder return on a larger pre-tax amount. An alternative approach considers the potential advantages of structuring the vehicle to have taxes paid up front in a manner that is acceptable to participants and the issuer. Such advantages may include:

- Taxable fair value is less than market value

- Long-term real ownership

- No forced liquidation (ownership can continue indefinitely without forced monetization, unlike RSUs with a 3-year vesting schedule)

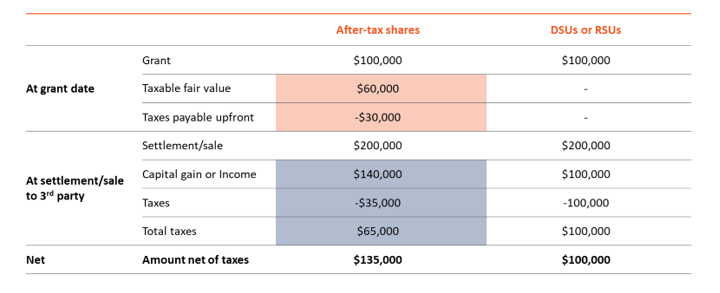

After-tax shares can be structured in a favourable manner by incorporating selling restrictions and reducing the taxable fair value. For example, if $100,000 of shares are awarded with selling restrictions, a valuator may determine that the taxable fair value of the award is only $60,000 – hence the recipient would need to pay roughly $30,000 in taxes upfront (assuming a 50% income tax rate). Recipients may find it appealing to pay lower tax upfront and then have capital gains and dividend tax treatment thereafter.

The table below provides an example of how such an award might work, comparing after-tax shares (left side) to RSUs or Deferred Share Units (“DSUs”). DSUs settle at retirement while RSUs settle at end of 3 years.

The result is long-term ownership that does not have to be monetized. This compares to RSUs and DSUs with taxable (and often monetizing) events on specific dates or short settlement windows.

Reconsidering Ownership Guidelines

Reviewing share ownership guidelines (“SOGs”) naturally fits into an LTIP review. SOGs started to become popular during the post-Enron era. The intent was to ensure management had “skin in the game.” Today, we are finding that SOGs are often not meeting their intended purpose. This is for two reasons:

- The portion of the LTIP mix in PSUs and RSUs has increased, with the RSUs typically included in the definition of share ownership

- The significant increase in the LTIP levels being granted since these programs were initially put in place

Put together, the portion of an executive’s ownership guideline covered through normal-course compensation received through RSUs has increased significantly. In fact, many companies find themselves in situations where ownership guidelines can be entirely fulfilled through annual LTIP grants, with no need for the executives to buy shares or defer their incentive into DSUs. (That said, we do note that many executives hold significant ownership in their companies – albeit independent of the ownership guidelines.)

Canadian issuers may wish to consider reviewing their approach to share ownership guidelines. In redesigning the share ownership guidelines, a number of factors should be taken into account, including:

- Alignment to wealth creation. The more wealth generated from the executive pay package, the higher the expected ownership levels should be. Conversely, the less wealth, the less ownership should be required.

- The LTIP structure. The structure, goals, and nature of the long-term incentives should be considered – i.e., ownership in 3-year RSUs should be given less weighting than (say) ownership with 5-year RSUs or real shares.

-

Characteristics of underlying shares. An assessment of the desired executive share ownership alignment in the context of the underlying share investment characteristics is important. All other things being equal, an executive of a highly volatile business should not be expected to have the same ownership guideline as an executive of a very stable and low risk business.

Too often, ownership guidelines are structured as an absolute level (e.g., 2 times salary). Moreover, many LTIP payouts are, for various reasons, ultimately paid out as cash and not “real” share ownership. Having multiple guideline levels could be a more appropriate approach for some companies. For instance, multiple SOG levels could be structured as follows:

- An amount that must be met with real ownership (e.g., 2x salary for a CEO)

- An amount that must be met with real ownership, DSUs, long-term equity and/or RSUs (e.g., 5x salary for CEO)

- An amount that is directly linked to the wealth created from LTIP payouts, with declining ratios as the level increases (e.g., 25% of LTIP payouts until 10x salary is met for the CEO; 10% of LTIP payouts until 15x salary is met)

There are numerous ways SOGs can be structured to achieve a real ownership component and an expectation that is aligned to how much wealth the executive is accumulating from the Company. Moreover, it can be naturally incorporated into the LTIP, such as having part of payouts delivered in real or deferred share vehicles.

Concluding Thoughts

For most companies, LTIPs are narrowly structured with the 3-year RSU, PSU, and stock option vehicle alternatives. As the Canadian shareholder and taxation landscape continues to evolve, consideration of true long-term incentives and ownership structures can serve as viable alternatives to stock options.