Introduction

Since the financial crises of 2008, there has been a lot of media and academic attention on mitigating against excessive risk-taking and addressing the problem of “short-termism” – pressure to produce short-term results. As it relates to equity compensation and short-termism, there is an argument that we have actually taken a step backwards – albeit unintentionally.

This document is an abbreviated version of “Rethinking Long-Term Incentives and Ownership Guidelines” by David Crawford. It considers the need to both revamp share ownership guidelines and to incorporate longer term features in equity compensation, all with the view of aligning compensation to the long-term shareholder experience.

While we believe it is important for Boards and management to consider possible equity compensation design improvements set out in this document; we also realize that moving significantly away from competitive practice should be carefully thought through. In the end, a pay program that does not engage a high performing management team will not be effective, regardless of the merits it is based on.

It is Time to Rethink Long-Term Incentives and Ownership Guidelines

The use of stock options has decreased dramatically over the last 15 years. The first shift away from stock options happened post-Enron and the dot.com bubble, leading to a remix or balanced approach of stock options, share units (PSUs or RSUs) and share ownership guidelines often supported by DSUs. The second major shift happened after the market meltdown – further increasing the pressure to reduce, if not eliminate the use of stock options.

RSUs, DSUs, and PSUs

Vehicles linked to the full value of a company’s shares that are either cash-settled or equity-settled at the end of the vesting period.

RSUs - Vest solely based on time

DSUs - Vest based on time, but are not settled until retirement, termination, or change of control

PSUs - Vest based on time and the achievement of future performance, which will determine the number of units settled (relative to a target number of units granted)

While shareholders generally view these changes favourably, there are two unintended, but important consequences

- Ownership guidelines were no longer meeting their intended purpose and were becoming a slam dunk in many companies. This is because RSUs, and to a lesser extent PSUs, counted as ownership for the purpose of meeting these guidelines. As awards of share units increased, ownership guidelines were being met without the need to buy shares and defer a bonus (in DSUs).

- There is no real long-term incentive. RSUs and PSUs, making up an increasing portion of the LTIP, normally have only a 3-year term. Moreover, those providing stock options still tend to have designs that are not truly long-term.

Building Share Ownership

Canadian issuers should consider reviewing their approach to ownership guidelines. In redesigning the share ownership guidelines, a number of areas should be taken into account, including:

- Alignment to wealth creation. The more wealth generated from the executive pay package, the higher the expected ownership levels should be. Conversely, the less wealth, the less ownership should be required.

- The LTIP Structure. The structure, goals and nature of the long-term incentives. Ownership in 3-year RSUs should be given less weighting than (say) ownership with 5-year RSUs or real shares.

- Characteristics of Underlying Shares. An assessment of the desired executive share ownership alignment in the context of the underlying share investment characteristics is important. Investment returns subject to greater external business risk should require less executive ownership than situations where external business risk was more moderate.

Too often, ownership guidelines are structured as absolute levels (e.g., 2 times salary) - independent of the areas described above.

Boards and issues should consider more appropriate ways. A rational approach going forward would be to break the ownership requirements into levels or steps. For instance:

Step 1: more moderate guideline (e.g., 2x salary for EVP) must be met with real ownership or DSUs. Until these guidelines are met, half of short and long-term incentives are settled in real shares or DSUs.

We note that in the US, retention ratios are quite common. There are effectively three types:

1. Holding period linked to stock options and share units (e.g., must hold half of after-tax gain or settlement for a period of 9 months);

2. Retention ratios until ownership guidelines are met (e.g., 50% after-tax settlement retained as ownership);

3. Retention ratios that continue beyond ownership guidelines (e.g., 25% of after-tax shares of equity compensation settlements).

Step 2: after step 1 is achieved, a more meaningful guideline (e.g., 4x to 6x salary for EVP) would be set and, until met, a smaller percentage of net proceeds from long-term incentives would be retained in shares (e.g., 25% scaling down to 15% as ownership levels increase).

Approaches to Real Long-Term Incentives

It is often said that share unit deferrals cannot be longer than 3 years. It is true that certain types of cash settled share unit structures do have limits. However, if structured properly, long-term incentives can go beyond 3 years, and we believe at least part of LTIP for most companies should go beyond 3 years in some manner.

Important note: The approaches provided in this section have a number of tax, accounting and securities issues. This section provides a high level review. For more detailed information on many of these approaches please note [CPA document: Equity-Based Alternatives to Stock Options]. Ultimately, it is important that tax, accounting and legal advice specific to each issuer’s situation be fully understood.

The remainder of this document outlines the five approaches or structures to achieve the goal of structuring real long-term incentives. Each of these approaches will have varying pros and cons in terms of organizational fit, performance measure structural challenges, as well as tax and accounting implications.

1. Deferred share units (cash-settled) take advantage of specific wording in the Tax Act that allows and, in turn, requires shares to be deferred until retirement or employment termination. To date, the most common application is as a voluntary deferral of cash bonuses. However, DSUs could be formally part of the LTIP with longer term vesting requirements.

2. Treasury-backed share unit structures. Where there is a treasury share reserve and the participant has the right to receive settlement in shares, the deferral/vesting period can be more than 3 years. In fact, there is significant flexibility in how these plans are structured, including:

- Fixed versus flexible settlement. Can have a fixed settlement date (e.g., 5 years after grant) or a flexible settlement date (e.g., any time between vesting and two years after participant leaves organization as a good leaver)

Cash-settlement alternative. It is possible to incorporate a cash settlement alternative for participants, whereby the participant has the right to receive settlement in cash in lieu of shares. For example, at both Imperial Oil and Bell Aliant, the recipients may elect to receive one common share per unit or an equivalent cash payment.

Cash-settlement alternative. It is possible to incorporate a cash settlement alternative for participants, whereby the participant has the right to receive settlement in cash in lieu of shares. For example, at both Imperial Oil and Bell Aliant, the recipients may elect to receive one common share per unit or an equivalent cash payment.

3. After-tax shares.

It is generally viewed unfavourably to have to pay taxes upfront when compared to utilizing pre-tax share units. That said, if the vehicle can be structured to have taxes paid up front in a manner that is acceptable to participants and the issuer, some interesting possibilities can emerge:

Supplement the funding level to consider the tax differences. As is provided in the example below, allocating 25% more to fund a plan with after-tax proceeds used to purchase shares can off-set the tax disadvantages. In fact, the participant has the added benefit of not being forced to monetize at a settlement date (which is the case with DSUs). From the issuers’ perspective, by allocating 25% more now, any ongoing liability associated with the grant is removed. In the example below, the cumulative corporate expense under DSUs is $200,000 in the future (or $100,000 plus the cumulative hedging costs) versus $125,000 at grant. Effectively there is a trade-off to moving to after-tax shares:

- On the negative side, taxes have to be subtracted upfront

- On the positive side, this can be offset by the combination of additional funding (e.g., 25%), lower tax rates when ultimately sold, and the flexibility to continue to deferral beyond what is available with DSUs

Incorporate selling restrictions and reducing the taxable fair value. If structured properly, long-term selling restrictions can reduce the taxable fair value. So instead of paying taxes on $100,000, the taxable fair value may be reduced to (say) $60,000. Senior executives may find this quite appealing to pay this smaller tax level upfront and have capital gains and dividend treatment thereafter.

For example, CREIT’s Restricted Unit Plan is designed as follows:

4. Long-term performance conditions. Cash settled plans can have a term greater than three years if there is a “substantial risk of forfeiture”. Some pension funds with greater than 3 year performance periods rely on this “substantial risk of forfeiture;” as do many phantom option plans (e.g., Sobeys)

5. Improved stock option design features. The most significant criticism of stock options is that the act of exercising is normally the act of selling and can be timed and done fairly early in the option term.

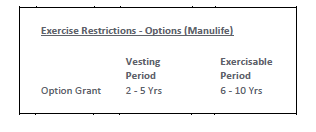

- Long-term share retention requirements. There are a number of ways that this can be structured depending on the goals and how options fits in the overall LTIP and share ownership program. We know from a number of US examples that executives with retention ratios will tend to continue to hang onto the shares even after restrictions lapse.

- Long-term vesting and/or exercise restrictions. Increasing the vesting period and / or restricting the ability to exercise until (say) the second half of the option term can make options truly long-term. Note: vesting for the purpose of determining the portion of options earned at employment termination can be structured to be closer to the competitive market. This approach is set out in the table below:

Conclusion

Boards and management should review and consider these approaches to providing longer term incentives and more effective ownership guidelines. The biggest challenge in terms of making changes is the pressure to do what everyone else is doing. However, an appropriate balance can be achieved in terms of staying close to competitive practice, yet moving in a better direction. Engagement with shareholders and their proxy advisors will also be important – as pay programs that are different may be exposed to greater attention.