This briefing is part two of our thought capital series on the changes to Canadian stock option taxation – please see Part One for a detailed overview of the upcoming changes. Our next article will focus on alternative equity compensation approaches and is expected to be published in Q2 2021.

In its 2021 federal budget released on April 19, 2021, the Canadian government affirmed its intention to proceed with the proposed changes to stock options taxation detailed in the November 2020 Economic Statement. Effective July 1, 2021 for covered companies (defined as non-Canadian Controlled Private Corporations with annual gross revenues greater than $500 million), the new stock option tax rules will eliminate the eligibility of employee stock options to receive preferential “capital gains-like” tax treatment, except for a $200,000 annual limit. The upcoming changes create an opportunity for companies to reassess and, if necessary, revise their LTIP strategy and design.

Purpose of LTIP and Overview of Common Instruments

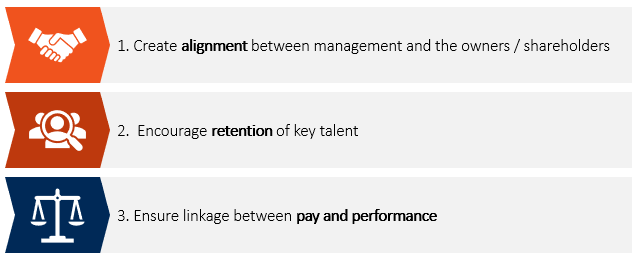

Long-term incentives are used by companies to motivate and reward management to achieve mid and long-term profitable growth, while fostering an ownership mindset among the management team. At its core, a long-term incentive plan (LTIP) should support three objectives:

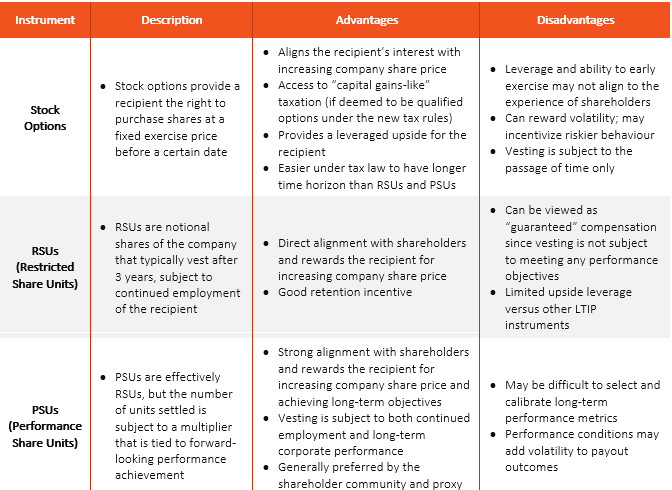

The most common LTIP instruments include stock options, restricted share units (RSU), and performance share units (PSU). Each of these instruments are equity-based in that their values are linked to the value of common shares of the business. Furthermore, a vesting period is typically attached to long-term incentives which conditions the payment to continued employment. As a result, the interests of LTIP recipients are aligned with growing the value of the business over the long-term. See Appendix for a summary of the key features of common LTIP instruments.

Right-Sizing Pay-for-Performance

When designing an LTIP and selecting the mix of instruments, an important factor is the desired degree of risk and reward, or “leverage”. A properly structured program should balance the stability and predictability of payouts with the overall compensation philosophy, company strategy, and purpose of the awards. Consider the follow questions when reassessing the long-term incentive program:

Q1: What is the company’s expected rate of growth, and how should it influence LTIP design?

To create the desired alignment between management and shareholders, the LTIP mix should be designed with the expectations on equity growth over the long-term, as well as the risk appetite of the company in mind. Since each LTIP instrument carries a unique pay-for-performance profile, the selection of the right instruments and mix is an important aspect of LTIP design. For instance, a company oriented more towards high growth may elect to use stock options and PSUs, both of which provide a greater degree of leverage. In contrast, a company seeking a more modest growth trajectory and a focus on retention may prefer RSUs and PSUs.

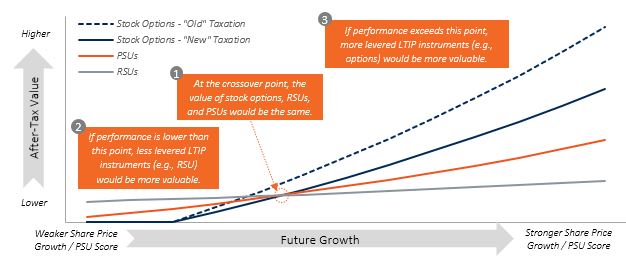

Q2: What is the leverage of LTIP instruments (stock options, RSUs, and PSUs), and how do they compare against one another?

RSUs provide a modest amount of leverage since its value is directly linked to the company’s common shares. PSUs provide a relatively greater degree of leverage due to a payout factor that is linked to performance on key objectives. Stock options often provide the highest degree of leverage due to the discounted valuation (typically determined using the Black-Scholes Model), which results in multiple options being granted for the equivalent value of an RSU. Exhibit A below illustrates the differences in leverage between stock options, RSUs, and PSUs on an after-tax basis.

Exhibit A: Example of Leverage in LTIP Instruments (After-Tax)[1]

Q3: How do the upcoming changes to stock option taxation impact the choice of LTIP instruments?

Under the new stock option taxation rules, only a limited number of stock options will be eligible for “capital gains-like” tax treatment and as a result, stock options will become less valuable on an after-tax basis to the recipient. However, stock options continue to have high leverage even after the changes and remain a viable LTIP instrument. As illustrated in Exhibit A, the value of stock options under the new rules can still exceed that of RSUs and PSUs in high share price growth scenarios. However, the changes in taxation, holding all other things equal, will require a higher degree of share price growth for stock options to deliver the same after-tax value as the current rules.

Q4: How should we assess the merits of various LTIP mix alternatives?

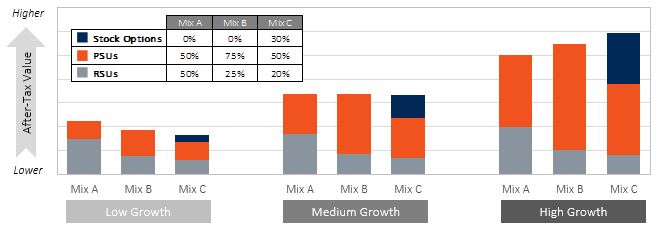

While testing different LTIP instruments in isolation is important, the company will ultimately need to determine an appropriate mix of LTIP instruments. This involves assessing the relative value of different LTIP mixes under various performance scenarios. Exhibit B below illustrates a comparison between three LTIP design alternatives. The comparison should be as close to “apples-to-apples” as possible (e.g., measuring the impact of the various instruments over the same time frame, which should include assumptions about reinvesting PSUs/RSUs to match the eventual crystallization with the exercise of stock options)

Exhibit B: After-Tax Value of Different LTIP Mixes

Under the Medium Growth scenario, the three LTIP mix alternatives produce similar after-tax values. When performance is stronger (High Growth scenario), the values of Mix B and Mix C increase at a faster pace due to the larger proportion of PSUs and stock options which provide greater leverage. When performance is weaker (Low Growth), the values of Mix B and Mix C see a more significant decrease for the same reason. The changes to stock option taxation will impact the after-tax value for the recipient, and thus necessitates a careful review of the expected outcomes under different performance scenarios.

Q5: Are there any unintended consequences due to the change in stock option taxation?

As illustrated above, the after-tax value of stock options will be materially less after July 1, 2021. If companies continue to include stock options after this date, they may consider the concept of a “gross up” such that executives continue to achieve the same level of after-tax benefits. This may come in the form of addition stock options granted to executives. Companies will need to review and address this philosophical consideration in the coming months and determine an appropriate course of action. Our experience to date is that companies are not contemplating any gross-ups or increases to stock option grants to match the after-tax value participants would receive prior to the taxation change.

Additional Considerations

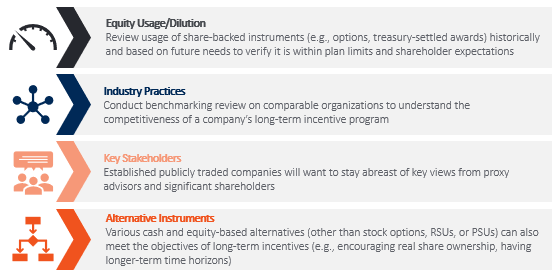

The evaluation of program and instrument leverage is one of many factors in designing an LTIP. Companies will want to assess other important priorities and considerations including the following:

Conclusion

The upcoming changes to Canadian stock option taxation will have a material impact for covered companies on the after-tax value of options for Canadian executives. As a result, the trade-offs between stock options and the mainstream alternatives of RSUs and PSUs will be impacted. Now is an opportune time for companies to reassess the LTIP design and consider the need for any changes to be implemented for 2022.

For further information, or for support with addressing the unique circumstances of your organization, we invite you to reach out to a Hugessen consultant.

Appendix: Key Features of Common LTIP Instruments

[1] This chart is intended for illustrative purposes only. Depending on factors such as the company’s future projected share price growth, structure of the PSU, valuation of stock options, and taxation, the after-tax values of the LTIP instruments may vary. Furthermore, the illustration assumes a perfect correlation between share price growth and PSU score.