The long-anticipated changes to Canadian stock option taxation are set to be effective July 1, 2021. The federal government, in the draft legislation released on November 30, 2020, provided details regarding the new limit on the eligibility of employee stock options to receive preferential “capital gains-like” treatment. For many companies, the impending changes mark an opportune time to review the LTIP design. This briefing is focused on the new stock option taxation rules; a follow-up briefing will cover revamping the LTIP strategy and design.

Highlights of the Changes in Option Taxation

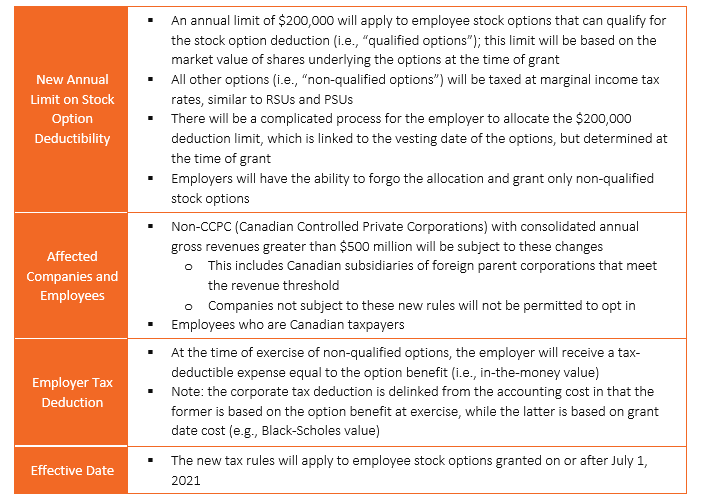

$200,000 Deduction Limit and Vesting

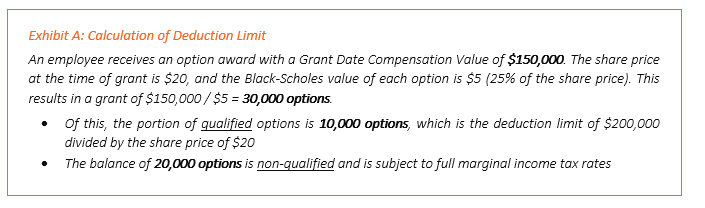

The $200,000 deduction limit on qualified stock options will be calculated on the underlying share price at the date of grant – note, this is different from the compensation value disclosed in the Summary Compensation Table. For example:

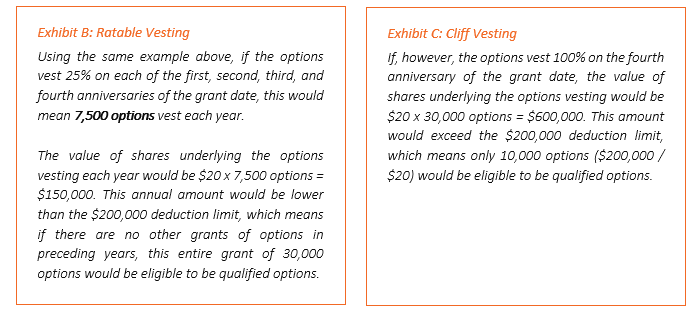

While the calculation of the $200,000 deduction limit is relatively straightforward, the process of determining qualified options will be more complicated depending on the vesting structure. The allocation of the deduction limit will be linked to the vesting date of the stock options, but determined at the time of grant. For example:

Companies that provide annual grants of stock options may find additional complexities in allocating the $200,000 deduction limit across different tranches of options. The allocation may be based on the calendar year the options first become exercisable, using effectively a First In, First Out (FIFO) approach – i.e., if more than one tranche of options vest at the same time, the tranche granted first would have the $200,000 annual limit applied before subsequent grants. In the end, the employer will need to determine what options to qualify (if any) up to the $200,000 deduction limit – and this must be done at the time of grant.

Key Issues and Questions

- Since most companies do not vest options until at least a year after grant, the $200,000 deduction limit for 2021 and 2022 will effectively be lost; for companies with cliff vesting of options, there will be additional years lost – Should the company consider if and how to qualify options and/or adjust vesting in a manner that accommodates individual tax situations?

- While non-qualified options are fully taxable to the recipient, the company will receive a tax-deductible expense equal to the option gain on exercise – How may this impact a company’s decision to qualify or not qualify stock options?

- For multi-national companies, how does the limit in Canadian stock option tax deductibility compare to other tax jurisdictions?

- How may societal factors impact the degree to which companies seek to minimize the increase in taxation for option recipients?

For many companies, now is a good time to review the LTIP design. Companies may wish to revisit the pay and performance philosophy and how the changes in option taxation may impact the role of options in their LTIP design going forward. Consider, for instance:

- What is the optimal place of stock options within the LTIP mix? On balance, do the advantages of stock options still hold notwithstanding the changes in taxation?

- What are the trade-offs between stock options and mainstream alternatives of RSUs and PSUs, and how will the new tax rules impact the risk-reward balance?

- Are there other long-term incentive alternatives that could be considered beyond the traditional 3-year RSU and PSU structures?

Conclusion

The upcoming changes to stock option taxation, though not yet enacted into law, are not expected to change substantially from the November 2020 draft legislation. While at a surface level the changes will harmonize the taxation of stock options with RSUs and PSUs, the $200,000 deduction limit provides a unique complexity for companies in their decision to qualify or not qualify option grants. In making their decision, it will be important for companies to consider the interests of shareholders, other stakeholders, and option recipients.

For further information, or for support with addressing the unique circumstances of your organization, we invite you to reach out to a Hugessen consultant.