As companies look to thrive in an ever more competitive environment, the role of management incentives (cash bonuses and equity compensation) and their effectiveness comes under scrutiny. Are these incentives rewarding improvements in performance, or are they contributing to less than competitive performance?

Many organisations calibrate their annual incentive plans to pay “target” awards for meeting internally developed budgets, usually including some testing of these budgets against the performance of best-in-class competitors to insure some “stretch” in the targets. However, sometimes budgets are repeatedly set at below best-in-class competitive performance, and as a result, incentive plan participants are rewarded with competitive (“target”) pay, but for uncompetitive performance. This practice effectively eliminates the incentive, or downside, to management for failing to close this performance gap, entrenching uncompetitive performance.

Companies facing this challenge will often have an underperforming stock price and can be targeted by activist or private equity (PE) firms. One of the main strategies for these firms is to acquire chronically underperforming companies, and then create value by closing performance gaps to deliver best-in-class performance and build shareholder value. Incentive programs are one of the tools used by these firms to motivate management teams to close any performance gap. While equity compensation is typically the cornerstone incentive used by activist or PE firms, changes to a company’s bonus programs can also influence company performance. Programs can be structured to not pay bonuses unless moving towards best-in-class performance, while offering significant upside bonus potential, but only for outstanding performance.

Incumbent boards and management of an underperforming company can consider taking the same approach as activist or PE firms to close any identified performance gaps. This can be achieved through implementing more demanding performance targets in management incentives plans. The process involves (i) assessing the competitiveness of the company’s performance, then (ii) determining changes to a company’s operations and strategy once shortfalls are identified, and finally (iii) calibrating cash incentives to reward successful execution of the performance improvement plan.

One of the most difficult changes companies will need to make is taking the “leap of faith” to adopt a true commitment to a performance-driven culture. Management and the board need to reflect on their organization’s culture to ensure it is enabling and motivating their employees to achieve superior performance. Getting the full support of management and the board on the need for change, along with a wholistic plan/strategy on delivering market-leading performance, will be essential to a successful turnaround.

4 Steps to Drive Towards Competitive Performance with Incentive Programs

The starting point is to focus on the competitiveness of the company’s underlying performance. Instead of focusing on historically achievable targets, set a revised business plan and strategy that aims to raise performance to world class levels.

STEP 1: Select 2 or 3 “Best-in-Class” competitors, and financial metrics for comparison

- Select best-in-class competitors – e.g. market leaders, market influencers and/or market disruptors

- Select key financial metrics where comparator data is readily available (typically from publicly traded companies) and metrics that can be compared across companies with minimal adjustments – industry agnostic measures (e.g. Revenue, EBITDA, Net Income, TSR) and/or industry specific measures (e.g. REIT metrics would include NOI, FFO, NAV) are a good starting point

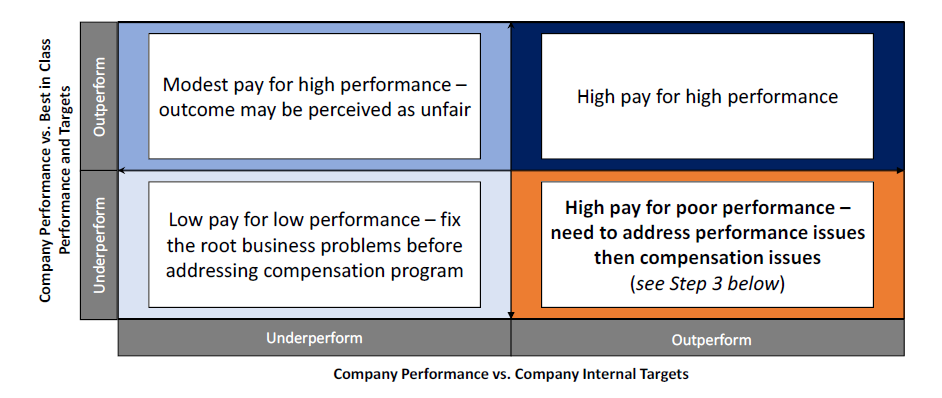

STEP 2: Compare the company’s actual/target performance to best-in-class performance targets

- The diagram below provides a framework to assess actual and target performance and the relationship between them

STEP 3: Once a performance gap is identified, develop an operating plan and/or strategy to close the gap

- Management, under the direction of the Board, first identifies the actions and changes required to meet the best-in-class standards, including strategic discussions, operational changes, transaction considerations, and reviewing expense levels/ budgeting process. For example, accelerating a move to e-commerce or adopting new technologies may be essential to achieve higher revenue targets.

- Approaches on how a company achieves higher performance goals are equally important as the goals themselves. Companies will need to consider factors such as discipline around capital allocation and appropriate risk management for each approach.

STEP 4: Set new incentive performance goals tied to achieving these performance enhancement initiatives

- Incentive performance goals should align with meaningful progress towards best-in-class awards to reward best-in-class performance

-

Ensure the plan does not reward mediocre, status quo performance (e.g. paying below market bonuses for sub-par performance

Case Study: Original Equipment Manufacturer

“Company A”, a Canadian-headquartered company with global operations conducted a thorough pay and performance benchmarking study. It was determined that their target total direct compensation was 20% higher than its peer group, while performance lagged best-in-class peers.

As outlined in the table below (Figure 1), Company A’s target setting process did not address any external reference points, but rather targeted relatively modest year-over-year improvements. Upon review, it was determined that EPS growth targets were set below the industry best-in-class “Group B”.

Based on the table below, the illustration (Figure 2) highlights the respective payout curves (solid lines) and probability of achieving each EPS growth rate (dashed lines).

After comparing Company A’s target to the best-in-class standard, the board established with management that the original budget was not closing the gap with best-in-class competitors, especially considering the higher target compensation. The board also determined that it was inappropriate to set the incentive target to the annual budget without consideration of any external reference points and that providing at or above market compensation for below competitive performance was not sustainable

The Board then guided management to develop a revised operating plan and strategy that would ensure the Company had a plan to meet the tougher performance standard. As part of these changes, the Company set its incentive target at the best-in-class standard to reflect achievement of this performance enhancement strategy – management and employees would only be rewarded for making measurable progress towards world class performance.

This new approach provided the motivation, direction, and resources for management to do things differently. The Company saw strong top-line growth through increased market distribution and a product enhancement strategy. Reflecting these enhanced goals and early wins, a significant amount of capital was invested to upgrade manufacturing facilities that increased efficiencies and lowered production costs. After three years, and the company saw an EPS increase of approximately 175% or an annual increase of over 40%.

The case study has been simplified to convey how firms can apply the approach described above on performance assessment. Each company requires significant business analysis and needs to address many other topics (e.g. calibration of performance shoulders). In essence, incumbent boards and management can consider the same tools used by activist or PE firms to enhance company performance – they simply need to have the will.

At Hugessen, we encounter situations where a considerable amount of time is spent making sure target bonuses are competitive while not enough time is spent making sure performance goals are competitive in a broader context. The framework above initiates a discussion on assessing incentive programs and their ability to drive competitive performance.