Part 4 of our series outlined different considerations for determining whether ESG metrics are more appropriate in a short-term or long-term incentive plan. This article focuses on the key considerations for incorporating metrics and determining the desired overall impact of ESG metrics on incentive plan outcomes.

Key Considerations – Incorporating ESG Metrics

Below are examples of a few considerations to help determine the preferred way of incorporating ESG metrics in the short or long-term incentive plans:

-

Consider if the metrics should be stand-alone discrete metrics or grouped together in a basket

-

Consider if the metrics should be a weighted component in a scorecard or a modifier

-

Consider the desired impact of the metrics on overall realized/realizable compensation (i.e., the appropriate weighting within the total compensation)

For illustrative purposes, we will be using “Employee Engagement” in a short-term incentive plan as the primary example. We note, the process is similar for a long-term incentive plan, however the dollar value/impact may be meaningfully more, depending on a company’s pay mix/philosophy.

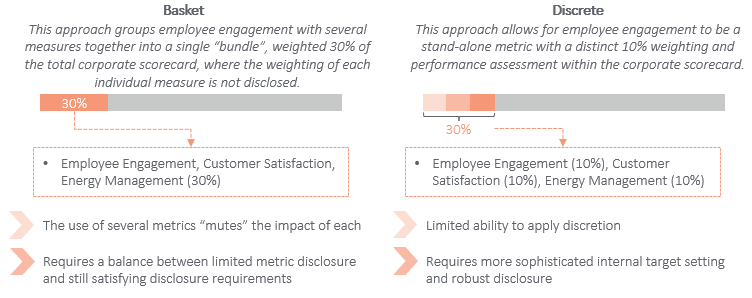

1) Basket vs. Discrete Approach

This illustration below details key considerations for whether the metrics should be discrete or basketed with other metrics. We note a basket approach can provide the company with additional flexibility on both the metric selection process and performance evaluation, providing more flexibility for companies integrating ESG metrics into their compensation plans for the first time.

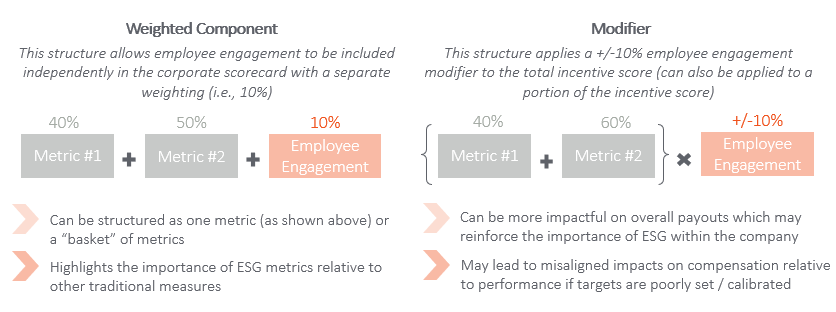

2) Weighted Component vs. Modifier Structure

After determining a basket or discrete approach, the next step is determining if the metric should be embedded in the scorecard, or applied as a modifier. As a guiding principle, modifiers have a more significant impact on payout than a modestly weighted component (i.e. 5%-10%) in the scorecard.

3) Impact of Metric on Total Plan

It is essential to ensure there is a balance between each metric having sufficient impact on the incentive plan while also ensuring the plan outcomes are aligned to overall corporate performance. Given this balance, companies should consider the impact of each metric and the impact of the total plan.

Summary and Next Steps

Ultimately, the company needs to consider the overall impact of an ESG metric on total compensation outcomes as it will help determine the appropriate structure / weighting of the desired metric. For example, if there is a high degree of comfort and confidence in target setting and measuring a metric, it may be logical to structure it as a stand-alone discrete metric with a higher weighting or as a significant modifier. The appropriate design may also be company size and industry dependent.

It is important to note incorporating ESG metrics will result in an inherent trade-off between the impact of traditional metrics (often financial and operational) and these new ESG metrics. Companies will need to ensure they are comfortable with these trade offs, and the potential impact to affordability, prior to implementation.

In the next article, we will look at how to determine the appropriate calibration for ESG metrics in the incentive programs.