Every year, Hugessen Consulting conducts a review of the proxy circulars filed by the constituents of the S&P / TSX60 Index to report on trends in executive compensation and related governance practices among Canada’s largest and most influential companies. This article is the third in a three-part series summarizing our findings related to environmental, social, and governance (“ESG”) metrics in executive compensation programs among these companies.

Part 1 of our series focused on the prevalence of ESG metrics being incorporated into incentive plans. Part 2 provided a deeper dive on how ESG metrics are incorporated into incentive programs (i.e., short term versus long term plans, weighted measure versus modifier). This article addresses the types of ESG metrics being used and measured.

A full recording of Hugessen’s webinar on Emerging Trends in Executive Compensation and ESG can be found here. Parts 1 and 2 of our 2022 TSX60 ESG series can be found here.

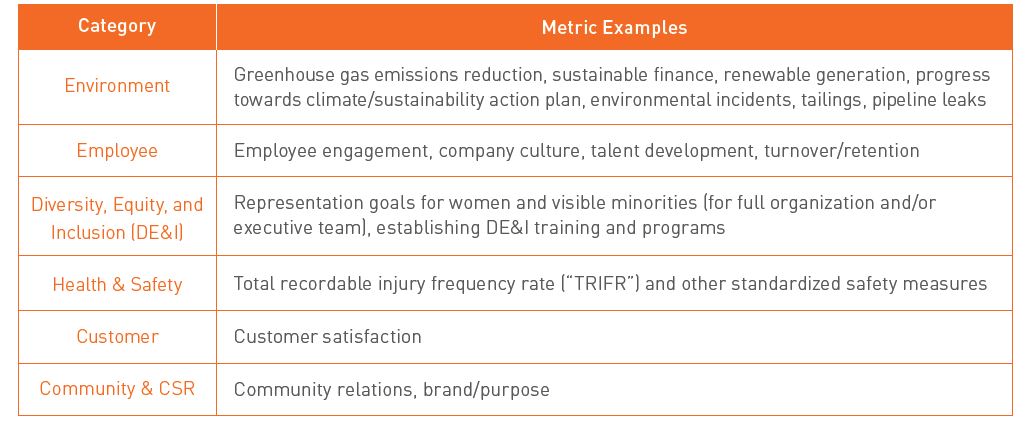

How do TSX60 Companies Measure ESG Achievements in Incentive Plans?

Below is a summary of the most common types of ESG measures we observed among TSX60 companies:

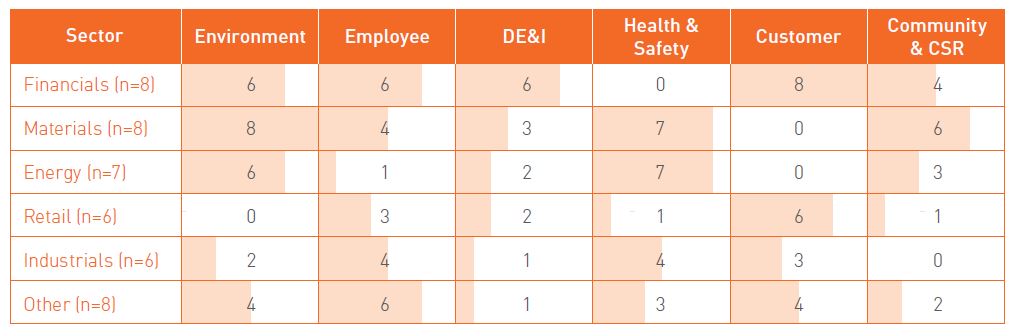

Use of ESG Metrics by Industry Sector

As a guiding principle, companies should only incorporate ESG metrics (or any metrics) into their compensation programs when they have a clear and well-understood link to the company’s strategy. As such, the types of ESG metrics we tend to see companies incorporate into their programs can often be generalized by industry sector. Traditionally, companies in the extractive sectors have tended to emphasize environmental metrics, while companies in the financial services and retail industries (among others) have tended to emphasize social metrics related to their customer base and employees. The table below illustrates the types of ESG metrics observed among the various industry sectors within the TSX60 this proxy season.

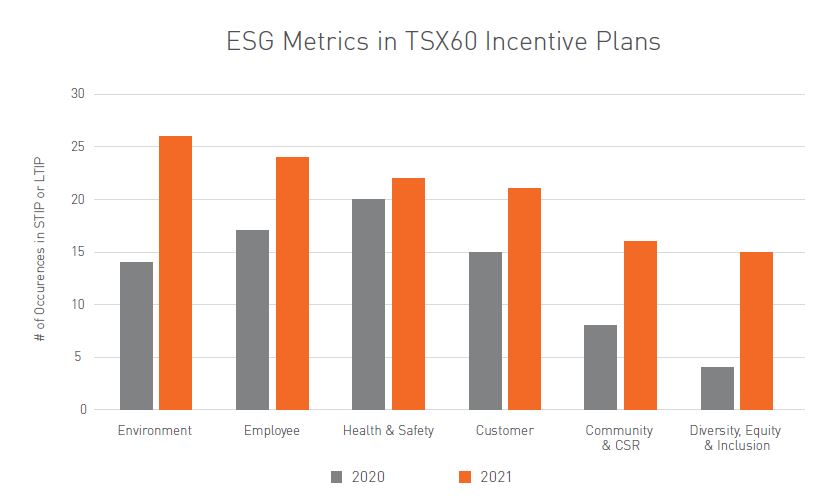

Key Theme for 2022: Emphasis on Environmental Metrics

This proxy season we have observed an increased emphasis on environmental, and particularly climate-related metrics among all industry sectors. 12 TSX60 companies added an environmental metric to their STIP or LTIP for the first time in 2021, 6 companies added an additional environmental metric or increased the weighting of an existing metric, and 5 companies disclosed an added metric or increased weighting for 2022.

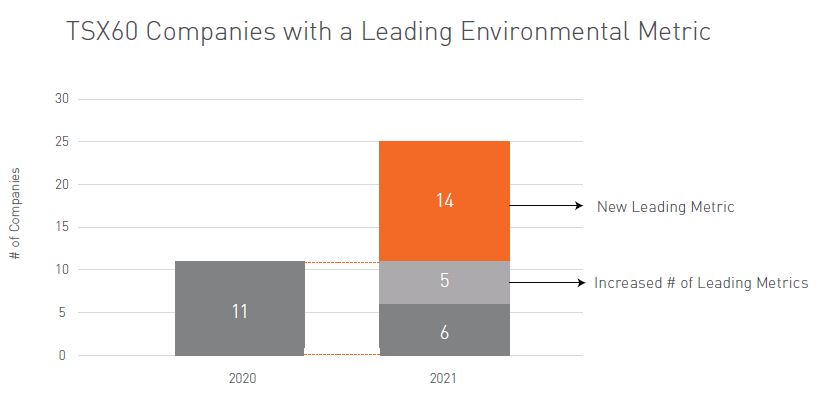

Climate Change: Use of “Leading” Environmental Metrics

One way to categorize ESG objectives is to group them as "leading" or "lagging" type metrics. Lagging (i.e., monitoring) metrics, such as backwards-looking safety and environmental incident measures, are well established in incentive plans; these often represent foundational operational metrics that are key to a company’s continued license to operate. While they still fall within the “ESG” category, they do not necessarily represent the more “transformational” or forward-looking metrics that are becoming an increasing focus for companies, shareholders, and society at large.

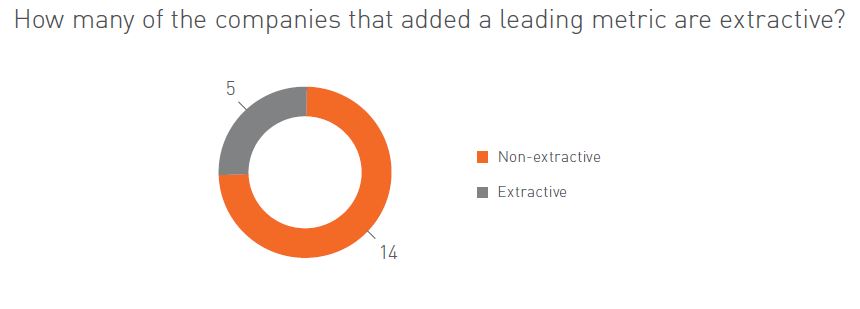

We observed a significant increase in leading metrics among TSX60 companies, particularly focused on the environment or climate change. This proxy season, we observed 25 companies with a leading type environmental metric in their compensation programs, 19 of which either added a leading environmental metric for the first time in 2021 or increased the number of these metrics in their programs.

Interestingly, the majority of companies that adopted new leading environmental metrics this year operate outside of the extractive sectors of the TSX60, indicating that climate change and other environmental metrics have become increasingly important for companies operating in all sectors. For example, several of the banks added progress towards climate action plans or longer-term sustainable financing goals as a measure within a broader group of ESG metrics.

Case Studies: “Leading” Type Environmental Metrics

Looking Forward

A likely next step will be increased scrutiny of the metrics and targets themselves. Similar to what we see for financial and operational metrics, we expect shareholders will look for additional clarity and disclosure as to why companies have selected particular metrics, how they link back to the company’s ESG strategy, and whether the targets that have been set represent meaningful progress against the company’s ESG strategy (e.g., are the targets tough enough?).

However, the underlying incentive design principles remain the same – thoughtfully designing programs that are meant to drive strong performance and positive outcomes for all stakeholders.