For the 3rd instalment in our COVID-19 Pulse Survey series, our Fall 2021 Director Pulse Survey provides insights into how Canadian directors are seeing 2021 pay and performance decision-making, 2022 priorities, and related compensation governance trends. Torys LLP has also provided their insightful perspective and commentary.

Key findings include:

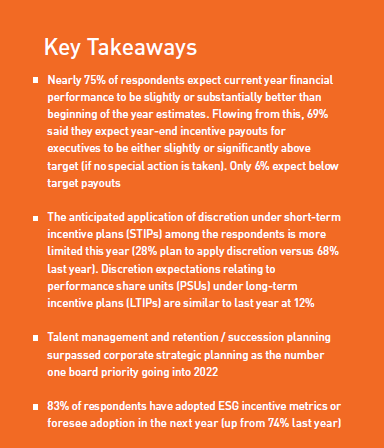

- Nearly 75% of respondents expect current year financial performance to be slightly or substantially better than beginning of the year estimates. Flowing from this, 69% said they expect year-end incentive payouts for executives to be either slightly or significantly above target (if no special action is taken). Only 6% expect below target payouts

- The anticipated application of discretion under short-term incentive plans (STIPs) among the respondents is more limited this year (28% plan to apply discretion versus 68% last year). Discretion expectations relating to performance share units (PSUs) under long-term incentive plans (LTIPs) are similar to last year at 12%

- Talent management and retention / succession planning surpassed corporate strategic planning as the number one board priority going into 2022

- 83% of respondents have adopted ESG incentive metrics or foresee adoption in the next year (up from 74% last year)

Introduction

For many companies across Canada, 2021 has been a year of recovery. That said, the year comes to a close in an operating and performance environment of brightening prospects, but continued uncertainty. The results of this year’s edition of our Director Pulse Survey represent a stark contrast from last year’s results, as corporate directors expressed a more optimistic tone. Financial performance expectations are generally strong, leading to at or above target anticipated incentive payouts and more limited use of incentive discretion compared to 2020. Other insights gathered relate to forward-looking base salary decisions, the incorporation of ESG (Environment, Social, and Governance) metrics into incentive structures, and board meeting practices. To help frame the insights from this year’s survey, we have also collaborated with the executive compensation and corporate governance teams at Torys LLP to provide their perspective and commentary.

Methodology

An Improving Pay and Performance Outlook

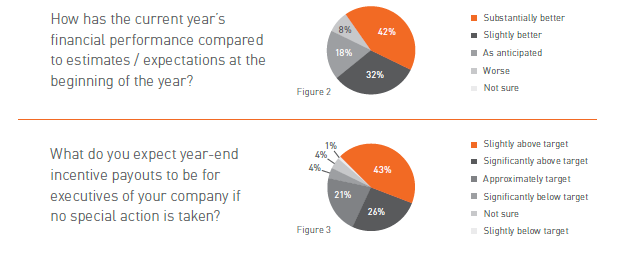

Both sentiment and actual results have had a much more positive tone in 2021 versus 2020. While 60% of respondents said their companies experienced a slight or substantial negative financial impact due to the COVID-19 pandemic last year, 74% now expect slightly or substantially better financial performance compared to expectations at the beginning of this year (Figure 2). These improved results are expected to have a direct impact on compensation, as 90% of respondents anticipate at or above target incentive payouts this year. (Figure 3).

Top Board Priorities

In this year’s survey, we asked directors about top board priorities going into 2022. The ongoing ‘war for talent’ has seen talent management and retention / succession planning eclipse corporate strategic planning as the top board priority in our 2018 Director Survey (Figure 4). Large-cap issuers are driving this result, with 72% responding that talent management and retention / succession planning is a very high priority. ESG-related priorities, such as environmental / sustainability, jumped three spots in the ranking (up to 3rd (tied) from 6th), while information technology / cybersecurity rose to be tied for the 3rd highest priority (up from 4th).

Going into 2022, on a scale of 1 to 5, please rate the importance of the following topics to your Board in the coming year. 1 signifies an issue of minimal importance, while 5 indicates an issue of very high priority. (Figure 4)

INSIGHT FROM TORYS

Having the right management team is crucial, especially in the face of disruption, so it’s not surprising that talent management, retention and succession topped the list of board priorities for 2022. Boards must ensure that they have the right team with the right expertise to address evolving risks and opportunities, which requires that key executives are properly attracted, incentivized and retained. Boards are taking a hard look at management competencies, compensation systems and performance metrics, diversity and workplace culture, and retention tools. In light of the dynamic work environment and the war for talent, Boards need to have confidence that management is developing a robust pipeline of potential successors and is creating and cultivating an inclusive workplace of choice.

To retain top-level talent, we are seeing companies implement increases in executive base compensation and providing senior management with enhanced incentive opportunities. These compensation increases may present opportunities for companies to amend their current contractual arrangements or enter into new contractual arrangements with their executives that provide greater protections for the company. For example, companies may consider implementing new or revised restrictive covenants, such as non-competition[1] or non-solicitation obligations, or improving the drafting of their executives’ current contractual termination provisions in order to increase the likelihood of enforcement. Public companies will also want to consider their public disclosure obligations and anticipated shareholder reaction before providing any increases in compensation.

2022 Executive Salary Expectations

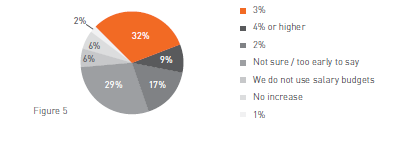

Whereas many companies implemented temporary base salary cuts and freezes last year in response to diminished business prospects and affordability constraints, going into 2022, 74% of directors participating in the survey anticipate an increase to executive salary budgets, the vast majority of which (86%) being equal to or above pre-COVID expectations. Of those that expected a specific % increase, 54% said +3%, while 16% said +4% or above (Figure 5).

Use of STIP & LTIP Discretion

Following a year of relatively liberal use of incentive discretion in 2020, we observe another year of historically above average—though more muted when compared to 2020—anticipated usage. As we observed with many of our clients, the setting of incentive targets early in the year was a challenging exercise, given the uncertainty around how the recovery might unfold.

Amid the strong incentive payout expectations noted earlier, 28% of respondents expect to apply STIP discretion, down from 68% last year. We note that of this 28%:

-

58% have already begun to discuss the process / considerations

-

58% anticipate applying upwards discretion, 16% negative and 26% not sure / too early to tell

Interestingly, this year, respondents do not anticipate that discretion will be applied in a manner that directly adjusts pre-set STIP target or actual results, a common approach utilized in 2020 to ‘adjust out’ the impact of COVID-19. Rather, the application of a formal discretionary plan component or overarching board discretion is the expected approach this year.

In terms of applying discretion to LTIP (PSU) programs, expectations were consistent with last year at 12%. As we noted last fall, we continue to attribute this modest application to a reluctance to modify multi-year performance objective measures, and the potential for increased shareholder and proxy advisor scrutiny as further discussed below.

INSIGHT FROM TORYS

Prior to exercising discretion to modify STIP or LTIP awards, companies will want to ensure they have a right to use such discretion, particularly if discretion is being used to negatively impact participant entitlements. Companies will also want to avoid the use of discretion in one year, which may be viewed as obligating the company to use similar discretion in subsequent years. These objectives can be achieved, in part, through clear and concise plan documentation and employee communications.

Public companies will also want to consider the views of institutional investors and proxy advisory firms regarding the use of discretion—for example, Institutional Shareholder Services (ISS) is generally not supportive of changes to outstanding LTIP awards and will evaluate any changes made on a case-by-case basis to determine if appropriate discretion was used and if adequate explanation was provided to shareholders of the rationale for the change.

Directors must act in the best interests of the company. Under Canadian law, the company’s interests are determined by reference to the interests of the various stakeholder groups that together comprise the corporate enterprise, and those interests may not always be aligned. While a decision to modify STIP or LTIP payouts could create conflict with the short-term interests of investors, boards need to think holistically and carefully balance the views of investors with the long-term best interests of the company and the need to incentivize and retain key members of management.

2022 STIP & LTIP Modifications

Nearly one quarter of directors participating in the survey said they anticipate making STIP design modifications in the upcoming year. Interestingly, while 47% responded that design changes were expected in last year’s survey, only 19% followed through based on this year’s results. The most common change both retrospectively and prospectively was / is adding or removing STIP metrics.

Similarly, only 18% said they anticipate modifications to the upcoming year’s LTIP, with the most common change being adding or removing PSU metrics.

INSIGHT FROM TORYS

Any amendments or modifications to STIP and LTIP designs, including applicable performance targets, must be clearly drafted and communicated in a timely manner to eligible participants in order to avoid any future conflicts or disputes. Additionally, any such amendments or modifications will generally trigger shareholder disclosure obligations in a public company’s next annual proxy circular, regardless of whether the amendments require shareholder approval. Accordingly, it will be important for public companies to provide a clear and compelling rationale for any such changes.

ESG & Incentives

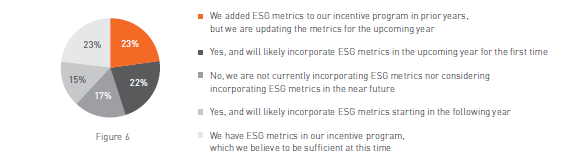

ESG-related issues remain a major boardroom topic across the country, a trend accelerated by the human capital impacts of the COVID-19 pandemic and recent social justice movements. As they pertain to incentive programs, 83% of respondents said their companies have already incorporated ESG metrics (46%) or are likely to incorporate them this year or next year (37%) (Figure 6). 100% of large-cap organizations are in this majority, as are 100% of Energy companies. This represents material progress since our 2018 survey, where 60% of respondents said their companies were not considering integrating ESG metrics into executive incentive programs.

Is your board considering the use of environmental, social, and governance (ESG) metrics in any incentive program for executives? ESG encompasses many topics, including environmental sustainability, diversity, etc. If your company incorporates standard safety metrics such as total recordable injury rate (TRIF), please note that we are excluding those from “ESG” metrics for the purposes of this survey.

INSIGHT FROM TORYS

ESG matters have quickly become an important strategic priority, and boards are being held accountable for their ESG commitments. Boards can differentiate themselves and create value through strong ESG performance, including by having clearly articulated, credible and broadly integrated short- term and long- term objectives and through demonstrable progress. It is crucial that management is properly incentivized to deliver on those objectives.

Approach to Board Meetings

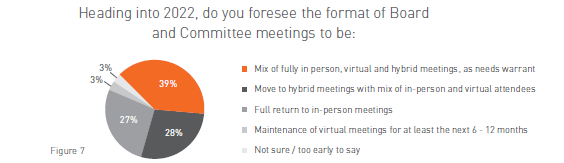

The COVID-19 pandemic required most organizations across the country to ‘go virtual’, a practice that largely persisted through 2021. For Canadian boards, what the ‘new normal’ will look like is mixed. Most directors foresee a flexible meeting approach in 2022, with a mix of fully in person, virtual and hybrid meetings, as needs warrant. Meanwhile, 27% expect in-person meeting to fully resume (Figure 7).

INSIGHT FROM TORYS

Boards should assess what is the best model for their particular organization. Regardless of the meeting format, it is critical that directors ensure that meetings are conducted with the same rigour that promotes robust discussion and allows all of the directors to actively participate, ask questions and effectively communicate any dissenting or divergent views and that directors are able to build rapport and trust.

Conclusion

Another year on from the onset of the COVID-19 pandemic, the pulse of Canadian directors is certainly more optimistic. While performance results have rebounded across many industries, new challenges have emerged, most notably talent retention pressures. Year-end incentive decision-making will likely continue to be rigorous as companies must adjudicate what may be strong calculated incentive results amid more modest overall performance outcomes. Meanwhile, Canadian directors’ shifting prioritization towards ESG topics will continue to evolve how incentives are used to influence and drive broader stakeholder considerations.

[1] In Ontario, non-competition obligations in employment agreements (non-compete agreements) are now prohibited (and, if applicable, voided) in employment contracts entered into with a non-“executive” employee after October 25, 2021. For additional details, please see Ontario passes Working for Workers Act, 2021 | Insights | Torys LLP