A short-term incentive plan (“STIP”), or sometimes referred to as an annual bonus program, is a common tool used to reward employees for their individual performance and to incentivize the achievement of annual business objectives. When properly structured, STIPs can support the alignment of pay with performance, and motivate the desired behaviours and outcomes in an organization. This article provides an overview of common principles and design choices for STIPs, with a focus on its application in executive compensation.

Principles and Objectives

The overarching philosophy and objectives of a company’s pay program play an important role in establishing the STIP design that is most appropriate. Common guiding principles for STIP design may include the following:

- Reward and incentivize employees for achieving annual business and individual objectives they have line-of-sight to.

-

Align pay with performance, ensuring the bonus outcomes reflect the success of the business and correspond with stakeholder expectations.

-

Design of the STIP should be clearly communicated and well-understood by participants to encourage the desired behaviours.

-

Incentive program should be market competitive and support the attraction and retention of key talent.

-

STIP should enable a robust performance management process for the management team, including the CEO.

Design Considerations

There are many design choices that a company has when structuring an STIP. Consideration could be given to market competitive practices such as the design used in peer companies, as well as organization-specific factors.

Size of Bonus Opportunity

The size of an STIP should be determined in context of the target total compensation for an employee to ensure pay is not excessive or diminutive. Market benchmarks can be used to inform the target levels of STIP that may be appropriate. The overall mix of fixed versus variable compensation should also be considered in light of the company’s pay philosophy. For executives, the mix of pay may need to be structured to avoid excessive short-term focus, and be appropriately balanced with long-term incentives.

Selection of Performance Metrics

An STIP is typically linked to performance on key annual business objectives of the company. This can be evaluated using quantitative and/or qualitative measures of performance. The employee should have line-of-sight and meaningful control over the performance metrics to support accountability and reward for the desired outcomes. As a company’s strategy evolves over time, the performance metrics can be reviewed and revised from time to time to ensure they remain relevant and continue to align with the company’s key strategic priorities.

Performance Target Setting

Targets for the performance metric(s) are often based on a company’s annual operating plan or budget. Performance targets should be set with a view to the likelihood of achievement. For example, they may be set at a level that is ‘rigorous yet achievable’. For companies with growth aspirations, the extent to which performance targets increase from year to year should be carefully considered. Additionally, target setting in cyclical industries or uncertain business environments may require more nuanced approaches to take into account a potentially greater variability of outcomes.

Degree of Stability vs. Variability

The balance of risk and reward is an important factor in structuring an STIP. A company will want to consider the performance sensitivity of the STIP (i.e., how much does it increase with stronger performance, and vice versa) and how stable or variable the payout should be from year to year. The use of informed judgment (sometimes referred to as discretion), either as a formal component of performance assessment or applied on an ad hoc basis, can help arrive at an outcome that is appropriate from a holistic lens. However, the misapplication of discretion could call into question the integrity of the STIP design and the associated performance targets.

Common Short-Term Incentive Structures

The following are three common STIP structures observed in the market: balanced scorecard, profit sharing program, and discretionary bonus program. While there are alternatives beyond the three listed below, a vast majority of annual bonus programs consists of some features that are reflected in the examples below or represent a hybrid approach.

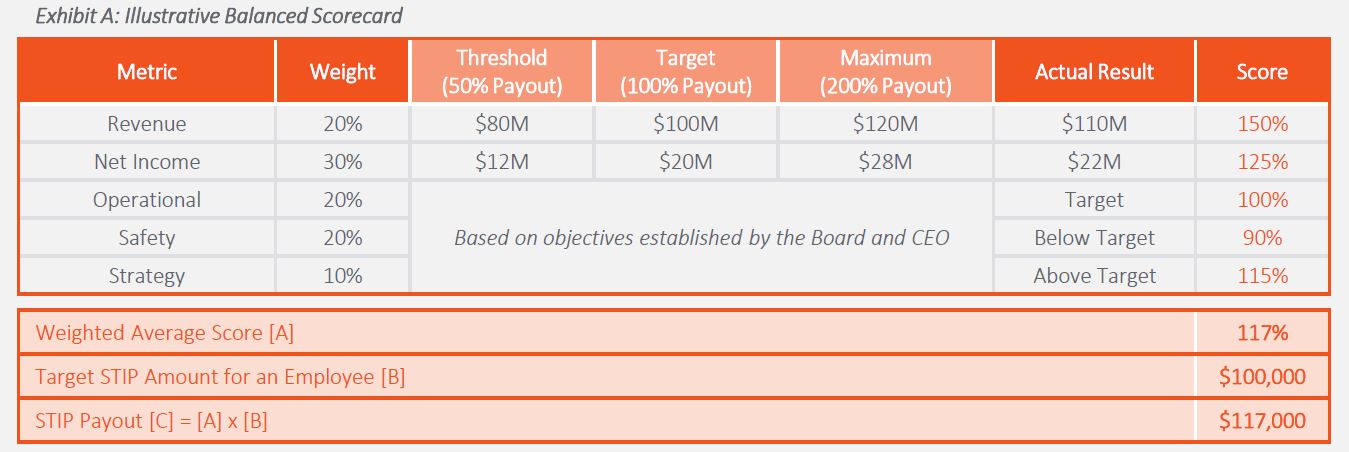

Balanced Scorecard

A balanced scorecard evaluates a set of pre-determined metrics, such as financial, operational, and individual objectives, that reflect the key indicators of success for a business. Each metric is assigned a specific weight that represents the degree of importance and emphasis on that metric. At the end of the period, a performance score is determined for each metric and a final weighted score is calculated to determine the STIP payout.

- A balanced scorecard provides an employee transparency and clarity into how the STIP is determined.

- The metrics and target in the scorecard can be set each year to reflect the annual business objectives.

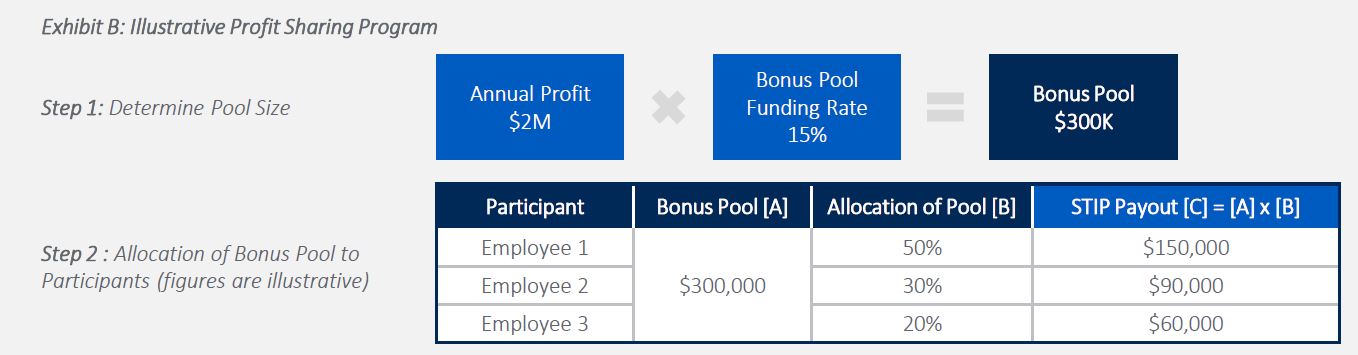

Profit Sharing Program

In a profit sharing program, an annual bonus pool is funded based on a pre-determined percentage of a measure of profit, cash flow, or value created by the business. Participants in the profit sharing program are then allocated a fixed portion of the pool.

- This approach provides a direct drive between incentive pay and business profitability, and can support the alignment of interests between employees and owners.

- A profit sharing program can be easier to administer since it does not require the establishment of annual performance targets. In very stable business environments, the payouts may be predictable and lack variability (i.e., akin to salary). Conversely, when business profitability is highly variable from year to year, profit sharing programs may produce volatile bonus outcomes.

- Safeguard features such as an overall cap on the size of the bonus pool, and a threshold level of profit required before any incremental profits are shared can be used to mitigate the risk of unintended outcomes.

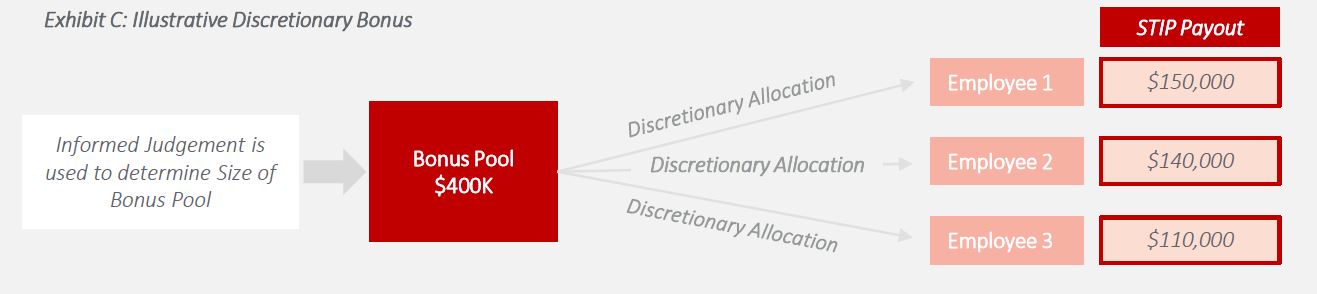

Discretionary Bonus

A discretionary bonus plan uses informed judgment to determine the size of the bonus pool which is then allocated to participants on a discretionary basis. While performance on key financial metrics are influential to the sizing of the bonus pool, this is not applied on a formulaic basis, but rather is evaluated in conjunction with other factors (e.g., a holistic assessment of company performance).

- This approach provides a greater degree of control for the owners/board to determine the STIP payouts. Since a discretionary bonus plan does not rely on direct drive metric(s), it may require greater effort to communicate and ensure an appropriate degree of transparency to employees regarding how compensation decisions are made.

Conclusion

A well-designed short-term incentive plan can be a strategic lever that drives performance and aligns employee actions with key business objectives. By carefully designing these plans, a company can unlock the potential of its human capital and ensure that every effort contributes to the strategic priorities of the company. The right incentive plan is not just about rewarding success, but about creating it.