Key Takeaways

Deferred share units “DSUs” are a widely used tool for Director compensation in Canada. While they offer several advantages, they also present limitations – most notably, the lack of flexibility at settlement. While DSUs allow Directors to accumulate equity throughout their tenure, they typically must be settled within a short window upon departure. This can limit a Director’s ability to hold shares for the long term and fully control the timing of monetization.

In today’s economic environment, attracting and retaining high-calibre Directors remains critical. Companies have an underutilized opportunity to provide greater flexibility, support long-term ownership, and eliminate corporate liabilities by offering Directors the option to receive real shares (i.e., direct taxable ownership) instead of DSUs.

If you answer “yes” to any of the following questions, there may be a compelling argument to explore this alternative:

Have any current Directors on your Board raised concerns about limited flexibility in when they can monetize their holdings after retirement?

This may be particularly relevant if:

- Your company settles DSU awards in cash and/or experiences a relatively high degree of share price volatility

- An increasing number of your board’s Directors are based in the US, where settlement flexibility is particularly restrictive

Does your company have a substantial buildup of outstanding DSUs?

- If treasury settled, this may create pressure on equity reserves.

- If cash-settled, this may result in a significant liability.

Each equity instrument has trade-offs, but for certain Directors, direct taxable ownership can be quite compelling. This may be particularly relevant for those who are in a financial position to pay taxes upfront, wish to hold shares indefinitely, are close to retirement and/or are based in the US.

Background: DSU Overview

Deferred share units “DSUs” are a form of equity-based compensation commonly used by Canadian companies for Director pay. They are similar to Restricted Share Units (“RSUs”) in that they offer participants the right to receive common shares (or cash equivalents) at the end of a specified period and are earned (i.e. “vested”) subject only to time-based criteria. The key distinction between DSUs and RSUs is that DSUs are only settled when the holder exits the company. Typically, a minimum portion of a Director’s retainer is delivered in DSUs, with the option to defer an additional amount of the cash retainer.

Similar to other forms of equity, DSUs can be settled in cash, shares purchased in the open market, or treasury shares. Most large Canadian companies elect to settle their DSUs in cash (though some settle via treasury).

DSUs are occasionally used for executives as well, though they are less common than RSUs & PSUs due to lack of performance-conditioning and liquidity. The most common use for executives is facilitated ownership through bonus deferral, though DSUs can serve as a long-term incentive vehicle or be granted for special purposes (e.g., on-hire awards).

Similar to other forms of equity, DSUs can be settled in cash, shares purchased in the open market, or treasury shares. Most large Canadian companies elect to settle their DSUs in cash (though some settle via treasury).

- Treasury-settled DSUs: These DSUs are settled in shares issued from the company’s treasury rather than in cash. By using this method, the company locks in the expense at the time of grant based on the fair market value of the shares, eliminating the need to track ongoing fluctuations in share price. Since the obligation is fulfilled with equity rather than cash, there is no liability recorded on the balance sheet.

- Cash-settled DSUs: These DSUs are settled in cash based on the company’s share price at the time of redemption. As a result, they are subject to mark-to-market accounting, meaning that the company’s financial statements must reflect changes in the liability as the share price fluctuates.

- Note: Cash-settled DSUs take advantage of specific wording (6801(d)) of the Income Tax Act that allows a long-term tax deferral, provided that they are based on a prescribed (i.e., common) share.

"The value of the DSUs must be based on the value of shares of a corporation. As a result, without adding considerable complexity, cash-settled DSUs cannot be structured to track the value of income trusts, partnerships or other noncorporate entities."

- Torys LLP

DSU Mechanics

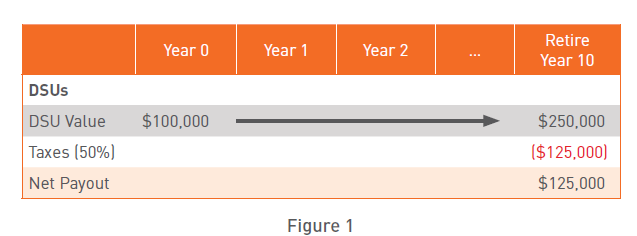

As DSUs accumulate, the tax liability for an individual fluctuates with the share value. At settlement (i.e., the taxable event), the recipient receives the share value in either cash or shares and is taxed at the full marginal rate.

DSUs are a leading form of Director equity as they…

√ Align Directors’ interests with the shareholders and ensure that Directors have a meaningful stake in the company until retirement

√ Offer the benefit of a full tax deferral, meaning that Directors have a larger amount of equity in play than RSUs, which are generally taxed after 3 years

√ Allow for efficient, pre-tax build up to share ownership guidelines (i.e., “SOGs”), and administrative ease for participants

√ Are accepted as an “ownership-like” vehicle by most institutional shareholders and the Canadian Coalition for Good Governance (“CCGG”)

√ Are exempt from the Salary Deferral Arrangement Rules (“SDA Rules”), regardless of whether they are cash or equity-settled in most cases (see note on income trusts on page 3)

However, DSUs present a number of limitations, including:

Lack of flexibility at settlement: DSUs may not meet the potentially desirable goal of facilitating long-term/indefinite ownership after retirement, as there is a relatively narrow window for monetization.

- Canadian Taxpayers: In Canada, awards must be settled by the end of the first full calendar year after departure. Although this provides some flexibility, in the context of an individual investment the settlement window can be punitive (as demonstrated below).

- US Taxpayers: US tax rules further limit settlement flexibility. Per Section 409A of the Internal Revenue Code, Directors must redeem DSUs within 90 days of departure unless a specific settlement date is pre-determined in the grant agreement. Torys LLP provides further insights in their video titled Year-end best practices: Cross-border compensation for dual taxpayers.

- DSUs may accumulate a significant liability (if cash-settled) or cause pressure on the equity reserve (if treasury-settled).

In some cases, there may be reliance on DSUs as a primary form of ownership (vs. common shares). While DSUs are accepted as ownership by most institutional investors and governance organizations, nothing beats real ownership.

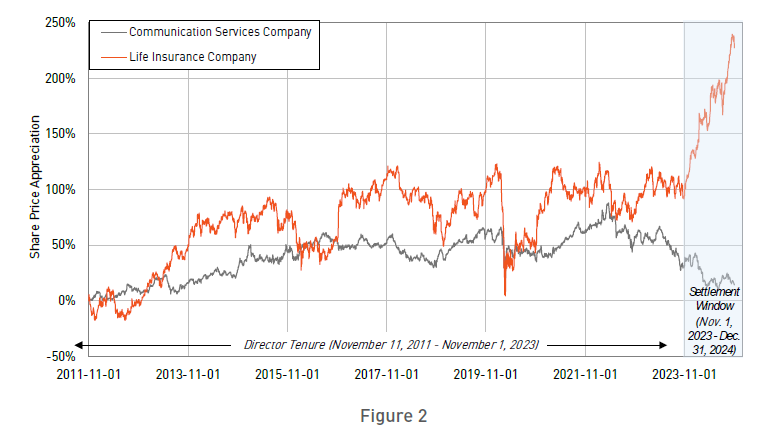

Impact of DSU Settlement Window on Director Payouts

This illustration highlights the potential impact of a relatively narrow fixed timeframe for DSU redemption post-retirement. A Canadian Director retiring in November 2023 after a 12 year tenure would have had until December 31, 2024 to redeem his or her DSUs. If this Director belonged to the communication services company (grey line) in the chart above, this limited window could have been relatively punitive.

A Compelling Alternative: Direct Taxable Ownership

To address the limitations of DSUs, companies have an opportunity to introduce an alternative: direct taxable ownership. This approach provides Directors with real shares upfront, offering greater flexibility while eliminating corporate liability. This could be facilitated in several ways – for example, through the Company arranging the purchase, to a Director agreeing to acquire a number of shares via a cash payment from the Company. To create long-term alignment with shareholders, this alternative may include a restriction limiting Directors from selling until departure.

"If the company is facilitating this program, it would need to ensure arrangements with a third party custodian are designed to ensure compliance with applicable corporate and securities laws and stock exchange rules."

- Torys LLP

This alternative may be particularly compelling for Directors who meet some/all of the following criteria:

√ In a financial position to pay taxes upfront

√ Close to retirement (the benefit of the DSU tax deferral lessens towards the end of a Director’s tenure) – see Figure 4)

√ Have a desire to hold the shares indefinitely

√ US taxpayer who may view ownership as preferential to deferred compensation

Comparison of Net Payouts

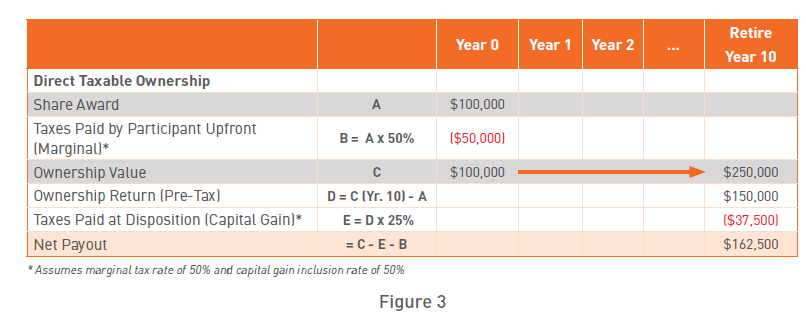

DSUs vs. Direct Taxable Ownership: In this illustrative example, the net payout to a participant would be marginally better from direct taxable ownership than DSUs.

Notes:

- For comparison purposes, this illustration assumes monetization at retirement. As previously noted, monetization at retirement is not required and a Director can continue to hold shares indefinitely.

- For US Directors, the tax rate on real ownership and capital gains should be very attractive relative to DSUs in most cases, assuming shares will generally appreciate in value over time and long-term capital gains rate will remain lower than ordinary income tax rate in the US.

- As in any ownership situation, a decrease in value would result in a capital loss, which cannot be directly deducted from income.

"For US Directors, if shares are granted subject to a vesting schedule, then the ordinary income tax that otherwise would have applied at grant can be delayed until the applicable vesting date(s). However, in such case, the requisite holding period for the preferential long-term capital gains rate will not start ticking until the vesting date(s) and the overall tax liability in respect of the shares could be greater if the shares appreciate in value between the grant date and the applicable vesting date"

- Torys LLP

Advantages of Direct Taxable Ownership

Direct taxable ownership addresses a number of the limitations of DSUs. Key benefits of this approach include the following:

- Offers participants maximum flexibility. After paying taxes upfront, any future growth is subject to capital gains and dividend tax. This structure allows participants to sell their shares (or never sell their shares) at any time after leaving the company, supporting long-term ownership. However, paying taxes at the outset creates an opportunity cost, which increases with tenure (see Figure 4 below).

- Facilitates ownership of common shares well beyond the Director tenure.

- Eliminates the corporate liability, which tends to grow over time, as the expense occurs at share grant with no subsequent growing liability (vs. a cash-settled DSU).

Diminishing Benefit of DSU Tax Deferral

As illustrated above, the value of the tax deferral offered by DSUs decreases as a Director nears retirement. Assuming a $100K share award and 50% marginal tax rate, receiving DSUs would enable a Director to defer $50K taxes rather than paying this amount upfront (albeit the value at settlement is then subject to the full marginal tax rate rather than capital gain and dividend tax treatment). If the $50K were instead invested at a 4% simple interest rate, its future value would grow to $80K after 12 years, yielding a $30K benefit. As the chart shows, this benefit steadily declines as the Director nears retirement, falling to just $2K in the year prior to retirement. This suggests that for Directors nearing retirement, the “opportunity cost” of immediate taxation may be a less material consideration.

Additional Considerations

- Providing Direct Taxable Ownership to Executives: If offering direct taxable ownership to Directors, there may be an argument to offer this alternative to executives as well.

- Accessing a Discounted Taxable Fair Value: We would be remiss not to note that some executive restricted ownership structures enable a discounted taxable fair value of awards due to holding requirements (e.g. if committed to not selling for 10 years, taxable value could be 50 cents on the dollar). That said, while this “discount” may be available for direct taxable ownership to Directors, some pause would be warranted as to the necessity to set Director pay to minimize taxes. For additional information on this concept, see Hugessen’s article titled LTIP: Beyond the Mainstream Alternatives.

Conclusion

In today’s evolving economic landscape, companies must take proactive steps to attract and retain high-calibre Directors. By integrating a direct taxable ownership vehicle into their compensation strategy as an optional alternative to DSUs, organizations can enhance flexibility and facilitate long-term ownership. Now is the time to evaluate this underutilized opportunity.