The fact that 2020 has been an unprecedented and challenging year is stating the obvious. Management teams have been working harder than ever to sustain their operations and support the well-being of employees, customers, and society at-large. However, there is no avoiding the reality that for many companies, financial and shareholder outcomes for this year will fall short of initial expectations, and in some cases quite significantly. For other companies, the pandemic has provided an economic windfall as demand for their products or services has surged.

So, what are Boards to do? As we approach year-end meetings, Boards and Compensation Committees are preparing for potentially challenging discussions related to corporate and individual performance for the year, and how this performance is valued in incentive plan outcomes.

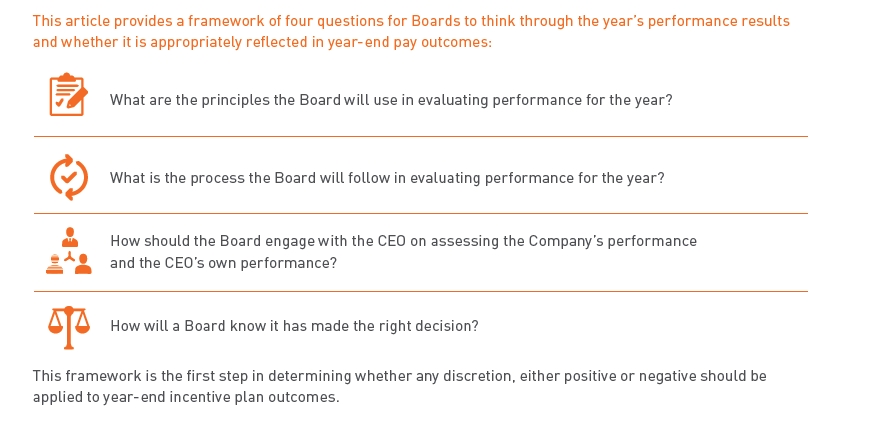

This article provides a framework of four questions for Boards to think through the year’s performance results and whether it is appropriately reflected in year-end pay outcomes:

This framework is the first step in determining whether any discretion, either positive or negative should be applied to year-end incentive plan outcomes.

What are the principles the Board will use in evaluating performance for the year?

In most cases, the Board’s typical performance evaluation approach will not be practical for 2020. For companies with well-defined performance evaluation frameworks and processes, the existing structures may not be flexible enough to capture the complex implications of the COVID crisis. The disconnect between the efforts of Management and the corporate results will have many Boards questioning how the evaluation of 2020 performance should be reflected in compensation outcomes for management teams.

To-date, most Boards and Compensation Committees have adopted a “wait and see” approach to 2020 incentive plan outcomes and have not applied discretion mid-cycle. That said, many Boards and Compensation Committees have expressed that they will consider applying discretion to compensation outcomes for the year closer to year-end.1 This discretion might be applied to the corporate scorecard for the annual bonus (or to specific measures therein) or to the assessment of executive performance as measured in the “individual” portions of incentive plans (typically annual bonuses). Discretion could be used to increase or decrease the calculated incentive plan outcomes, based on the Board’s overall assessment of performance and in some cases affordability.

In approaching these challenging performance evaluation and compensation decision-making meetings for 2020, we suggest Boards and Compensation Committees develop principles that reflect both the Board’s underlying compensation philosophy and the organization’s culture.

As a starting point, Boards may consider the following questions, which can help establish principles for decision-making, and should be tailored to the specific circumstances at each company:

In most cases, the Board’s typical performance evaluation approach will not be practical for 2020. For companies with well-defined performance evaluation frameworks and processes, the existing structures may not be flexible enough to capture the complex implications of the COVID crisis. The disconnect between the efforts of Management and the corporate results will have many Boards questioning how the evaluation of 2020 performance should be reflected in compensation outcomes for management teams.

To-date, most Boards and Compensation Committees have adopted a “wait and see” approach to 2020 incentive plan outcomes and have not applied discretion mid-cycle. That said, many Boards and Compensation Committees have expressed that they will consider applying discretion to compensation outcomes for the year closer to year-end.1 This discretion might be applied to the corporate scorecard for the annual bonus (or to specific measures therein) or to the assessment of executive performance as measured in the “individual” portions of incentive plans (typically annual bonuses). Discretion could be used to increase or decrease the calculated incentive plan outcomes, based on the Board’s overall assessment of performance and in some cases affordability.

In approaching these challenging performance evaluation and compensation decision-making meetings for 2020, we suggest Boards and Compensation Committees develop principles that reflect both the Board’s underlying compensation philosophy and the organization’s culture.

As a starting point, Boards may consider the following questions, which can help establish principles for decision-making, and should be tailored to the specific circumstances at each company:

What is the process the Board will follow in evaluating performance for the year?

Once the Board has had initial conversations and is aligned around the principles that will be used to evaluate performance and make compensation decisions, the next step will be to agree upon the process that will be used leading up to year end.

How should the Board engage with the CEO on assessing the Company’s performance, and the CEO’s performance?

Particularly for 2020, performance discussions should occur between the Board and the CEO early and often. Establishing the principles and processes referenced above should be done collaboratively with the CEO to agree on assessment approaches, and to provide the CEO with clarity as to the Board’s intended approach to evaluating performance. This will allow the CEO to align the broader team around this shared view of performance for the balance of the year. The amount of information shared with the CEO may be dependent on the relationship between the CEO and Board: where there is a strong relationship, the process to engage and collaborate with the CEO is much more effective.

Some practices to consider when engaging the CEO on evaluating performance include:

- “Front-end load” conversations related to evaluating performance and compensation decisions for the year; if the process and principles are agreed early in the cycle, it can help facilitate smoother discussions at year-end once results are known

- The Board should develop its own independent perspective on the CEO’s performance before it considers the CEO’s self-assessment

Some practices to consider in engaging the CEO on assessing incentive plan outcomes include:

- Self assessment for the CEO and assessments for the balance of the management team: the process should be similar to other years, but assessments may be more tied to ability to manage the organization through the crisis and ability to pivot in response to the pandemic

- Iterative discussions between the Board and the CEO to reconcile any differences in these assessments vs. the Board’s view of the CEO’s and other executives’ performance